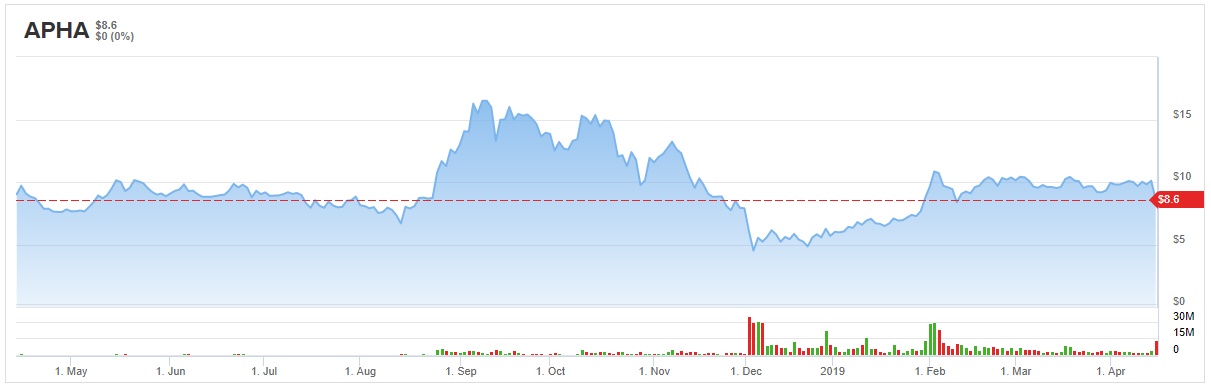

Medical marijuana stock Aphria (APHA) caught fire on Monday — in a bad way.

Reporting earnings early Monday morning, Leamington, Ontario-based Aphria closed the day down nearly 15% despite having grown its sale 240% sequentially in its fiscal third quarter 2019 — and 617% year over year!

How in heaven’s name could that be bad news?

Basically, the answer is that despite growing sales, Aphria failed abysmally at the primary purpose of all for-profit enterprises: Earning profit.

In Q3, Aphria reaped $73.6 million in sales, and kept $13.4 million of that as gross profit. The real problems appeared farther down the income statement, however.

As sales sextupled, “general and administrative” expenses octupled to $22.4 million. Share-based compensation expenses, marketing costs, R&D, amortization — all of these expense items rose rapidly in Q3, culminating in a massive $58 million charge to earnings for the “impairment” of assets that left Aphria with operating costs of $106.6 million, wiping out every last penny of the company’s gross profit, and saddling Aphria with an $89.3 million operating loss for the quarter. By the time Aphria reached its bottom line, net losses had ballooned further to $108.2 million — $0.43 per diluted share, and a reversal of last year’s $0.08 per share profit.

Now obviously, the worst line item of all in the above was the $58 million impairment. Aphria addressed this item specifically in its report, explaining that “the Ontario Securities Commission requested … that the Company perform an impairment test on its LATAM assets subsequent to the filing of the 2019 second quarter financial statements.” Aphria dutifully complied with this request, and after doing so, “determined that a $50 million non-cash impairment charge to the carrying value of” its assets in Colombia, Argentina, Jamaica, and Brazil was required, based on “new financial information received from” its financial advisors.

So what did these advisors discover?

Basically, these advisors told Aphria that its Latin America and the Caribbean assets — acquired in a July 2018 deal to purchase “LATAM Holdings” from Scythian Biosciences — were earning “lower gross margins and EBITDA margins” than had been earlier believed. As a result, these assets are less valuable than previously believed.

Aphria had paid “approximately $195 million” to acquire these assets, but as it turns out, it overpaid — then exacerbated the mistake by making a further $30 million in additional investments in these operations. Consequently, Aphria had to write down the value of what it bought.

Obviously, this is a disappointment, but before you dismiss this as a case of Aphria making “one bad call,” and basically being a good company despite its unforced error, consider: $58 million is a big number, but it was still barely half of Aphria’s total net loss for the quarter. Even had Aphria not overpaid for LATAM Holdings, the company would still have ended up losing a lot of money in Q3.

Now, Aphria management deserves credit for fessing up to this fact. In plain black and white, management admitted that even “excluding the aforementioned non-cash impairment charges” related to LATAM Holdings, its “adjusted net loss was $50.2 million , or $0.20 per share” for the quarter. That being said, a loss is still a loss — and Aphria’s post-earnings sell-off was the correct response to this loss.

Seaport analyst Brett Hundley commented, “In our view, Monday’s move in the stock is more a function of APHA’s $50MM impairment charge on its LATAM assets rather than anything else. To be sure, many industry participants are wrestling with near-term growing pains inside Canada, and Aphria is no different. But the write-down on LATAM is akin to reopening old wounds, even if such impairment is the result of recent company actions to set the Colombian business up better for the long-term. Management simply must move forward and clear all related corporate governance hurdles before this stock will likely achieve any type of multiple, in our view. Alongside the impairment charge, the company announced that it has entered into a series of transactions that will effectively lead to the expiration of Green Growth Brand’s (GGBXF) unsolicited bid for the company, coupled with Aphria ultimately realizing a relatively complicated payment of $89MM. The latter is obviously a net plus, but we think some shareholders may have been disappointed to see a takeout offer removed. We think that APHA is better off on its own, for now.”

“We think that a refreshed corporate governance profile together with its global asset base will set the company up well for the future. We think strategic partners will be part of the equation,” Hundley concluded.

Hundley reiterates a Buy rating on APHA stock, while lowering the price target to $16.00 (from $18.00), which implies nearly 86% upside from current levels.

To read more on the nitty gritty of what’s going on in the rising cannabis industry, click here.

More on APHA: Aphria: The Problem with the Cannabis Stock Market