The results are in, and it looks like cannabis company Aphria (APHA) hit another ball out of the park. Unlike other heavy hitters in the space, this name has consistently impressed Wall Street with its performance, and its most recent quarter was no exception.

According to its fiscal Q3 earnings report, which was released Tuesday, the company generated net revenue of CA$144.4 million, flying past the CA$131 million consensus estimate. Not to mention this number is up from CA$120.6 million in the previous quarter. Group adjusted EBITDA also didn’t disappoint. For the fourth consecutive quarter, the figure came in positive at CA$5.7 million. If that wasn’t enough, the average adult-use selling price got a boost on a quarter-over-quarter basis, growing from CA$5.22 per gram to CA$5.47 per gram.

However, APHA did deliver an unwanted piece of news. The company hasn’t been able to escape COVID-19’s grasp on the market, and as a result, management announced that it would suspend full year 2020 guidance.

Covering the cannabis stock for Jefferies, analyst Owen Bennett isn’t surprised by the guidance suspension, but instead tells clients to focus on everything APHA has going for it. “First, cash levels are very healthy with no material debt maturities in the next 12 months and new capex projects ceased, meaning little liquidity risk even if the situation worsens. Second, Aphria go into this period of uncertainty with clear sales and earnings momentum that they should be able to resume. Thirdly, and to this, the company intend to re-instate guidance though concede this may not be until FY21,” he commented.

Adding to the good news, Bennett believes that its strong execution, profitability, industry-best brand positioning and possible near-term positive newsflow make it a stand-out in a highly competitive industry. Expounding on this, the analyst stated, “The highlight for us has to be the demand that is evident for Aphria’s products. In an industry where peers are seeing top-line pressures from spending the first 12 months of legalization filling the shelves, Aphria is having to source third-party product to try and keep up. Pushback maybe that wholesale shipments have increased but this was a tactic to offload lower potency THC products.”

While bulk sales might not reach the same high level in the next quarter, Bennett argues that all of the above justifies his bullish stance. This prompted the analyst to not only reiterate his Buy rating but also call APHA his “top pick in the space.” In addition, his CA$10.00 (US$7.29) price target puts the upside potential at nearly 100%. (To watch Bennett’s track record, click here)

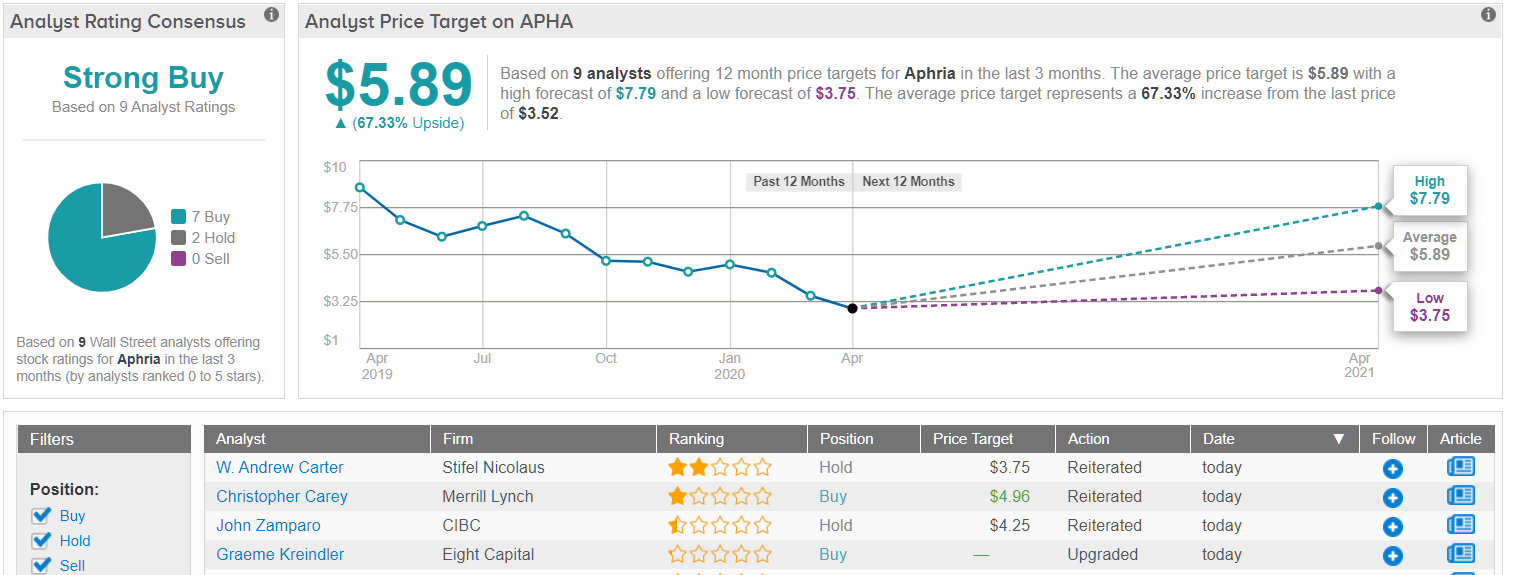

What does the rest of the Street think about APHA’s long-term growth prospects? Based on 6 Buys and 1 Hold assigned in the last three months, the word on the Street is that this cannabis stock is a Strong Buy. Despite being less aggressive than Bennett’s forecast, the US$5.89 average price target indicates 67% upside potential. (See Aphria stock analysis on TipRanks)

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.