The market appears disappointed that Aphria (APHA) withdrew FY20 financial targets. Yet, the Canadian cannabis company continued to show market leadership with strong FQ3 results. The company provided a twist to the quarterly results showing the current large benefit from remaining in the farming business and a negative sign of where wholesale cannabis prices eventually will head. The stock remains in a strong position to rebound as the global economy reopens from the coronavirus shutdown.

Future Margin Boost

The news from Aphria’s FQ3 results wasn’t quarterly revenue growth, but rather the massive margin impact from buying wholesale weed. The company saw cannabis revenue surge to C$55.6 million, up 65% from only C$33.7 million in the prior quarter. Cannabis EBITDA nearly doubled to C$6.0 million in the quarter.

The real story was how much cannabis margins were hit by Aphria having to make a C$20.2 million wholesale purchase in the prior quarter. Some of the license approval delays for their new Aphria Diamond facility required the company to make a large temporary purchase before their own cannabis supplies came online.

The big news was the level of margin impact versus homegrown supplies expected to cost below C$1. The company forecast the wholesale supplies cost Aphria 1,360 basis points on cannabis gross margins in the quarter and a C$7.6 million hit to gross profit and adjusted EBTIDA.

Aphria expects gross margins to jump back above 56% going forward with the normalized adjusted EBITDA for the last quarter of C$13.6 million, or more than double the reported amount. While other large Canadian cannabis companies are closing operations to cut costs more in line with sales, Aphria is working to expand operations to grow actual EBITDA profits.

Industry Ramifications

Anybody in the wholesale cannabis space is going to have a hard time completing sales in the C$3+ per gram price point going forward. Not only is Aphria entering the market with the ability to dramatically increased their own production levels, but also the company is clearly exiting the wholesale market as a buyer.

The company is promoting gross margins for homegrown cannabis at double the 25% margin generated on the product sold during the March quarter. Not enough margin exists currently in buying supply in bulk considering Aphria made a massive purchase and still couldn’t make much of a profit.

Long term, the cannabis market is likely to shift into one where strong brands buy product in bulk, but currently the wholesale prices are generally at levels double or triple the costs to grow. Any company in the wholesale business is likely still facing a difficult 2020 while cannabis sales rise in Canada, but the prices should collapse.

Takeaway

The key investor takeaway is that Aphria remains the best positioned Canadian cannabis company. The current management team has the company already generating solid EBITDA margins on the cannabis business and has a cash balance in excess of C$500 million to survive and thrive as the economy reopens in the next weeks and months. As new retail stores open in Canada this year, Aphria is a buy on any weakness.

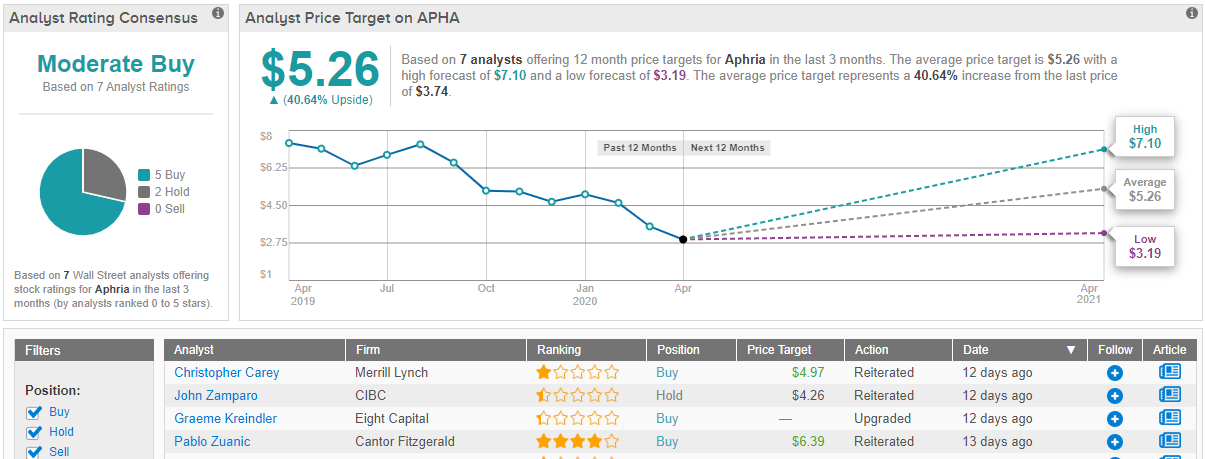

It’s worth pointing out that Aphria stock has been endorsed with 5 “buy” ratings over the past year, compared to only 2 “holds.” Meanwhile, the consensus estimate of analysts polled is that Aphria shares should rise a 40% (40.64% to be precise) to hit $5.26 within a year. (See Aphria stock analysis on TipRanks)

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.