As most of North America goes back to work following shutdowns due to the coronavirus outbreak, one sector that survived the economic weakness was the cannabis sector. The sector was generally seen as essential by various governments due to the medical cannabis aspect while other retailers were forced to close.

The Canadian cannabis sector continues to see sales grow as more retail stores are opened and Cannabis 2.0 products are rolled out. For January/February, sales were roughly C$150 million per month. The country is now on the pace to top C$2 billion in annual sales this year.

In April, the sector now has 1.5x the number of retail stores as recently as November with more stores on the way in the key province of Ontario. In addition, the Cannabis 2.0 rollout continues to provide another boost to sales.

The bigger question for the sector was liquidity as financial markets became less willing to lend to firms in a developing market such as cannabis with the onset of a recession. Yet, despite weak access to affordable capital, the strong sector sales set up the players with excess cash to survive and thrive in this period.

We’ve delved into these Canadian cannabis stocks with two stocks to consider here and one to avoid. Using TipRanks’ Stock Comparison tool, we lined up the three alongside each other to get the lowdown on what the near-term holds for these cannabis players.

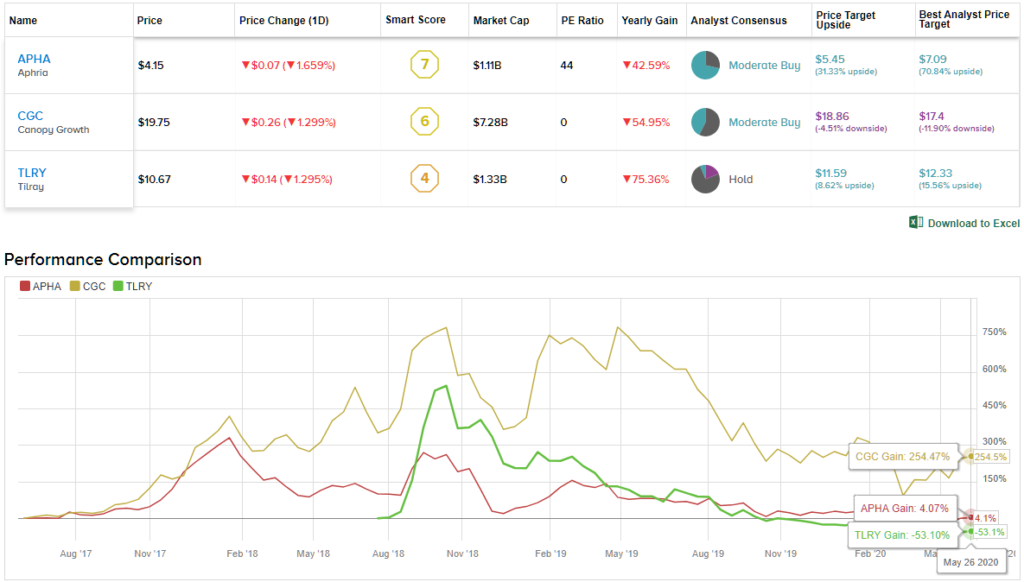

Aphria (APHA)

We will start with Aphria, a Canadian cannabis producer with a strong cash balance sheet and a solid operating business. The stock has started a solid rally off the $3 lows due to encouraging signs in the cannabis sector.

The company ended the last quarter with C$600 million in cash on the balance sheet. On the negative side, Aphria did have C$465 million in debt, but the key at this point in the cycle is the liquidity while smaller competitors lack access to reasonable funding.

The company made the recent deal in May to convert C$127.5 million worth of convertible debt by issuing 18.7 million shares for a conversion price of $4.84 per share. The deal saves C$6.7 million in annual interest costs.

Analysts are forecasting FY20 revenues reaching $390 million followed by nearly $500 million in FY21. The stock has a market cap below $1 billion so lots of value exists here.

The stock is one of the cheapest in the Canadian cannabis space and Aphria is one of only a few cannabis companies with a net cash position above C$150 million. The stock rally to $4 appears the start of extended gains as Aurora Cannabis changed the sentiment in the Canadian cannabis sector.

Overall, APHA holds a Moderate Buy rating from the analyst consensus, based on 5 “buy” ratings and 2 “holds.” Shares are selling for $4.19, and the average price target of $5.45 implies about 30% upside potential. (See APHA stock analysis on TipRanks)

Canopy Growth (CGC)

As with a lot of sectors, the rich only got richer during the downturn. In this case, Canopy Growth saw Constellation Brands cash in warrants providing more cash for financing growth.

The large Canadian cannabis company ended the December quarter with a cash hoard of C$2.26 billion and the C$245 million from the warrants will further boost the balance sheet. The biggest question for Canopy Growth is whether the new management team can drastically cut the cash burn from large EBITDA losses.

The news wasn’t really surprising with the strike price at only C$12.9783 per share for 18,876,901 warrants to purchase Canopy Growth when the stock was trading above C$21.

The warrants equated to 5.1% of the outstanding shares of Canopy Growth placing the Constellation Brands position up to 38.6%. The company owns warrants to purchase another 139,745,453 shares for a controlling position of 55.8%.

With the extra cash, Canopy Growth remains a solid stock to own here at $18. My recommendation has recently held to pick up the stock on weakness as the company looks to grow revenues while substantially cutting the EBITDA losses from the C$92 million in the last quarter. As the company gets closer to breakeven, the stock will regain a lot of the previous interest in the cannabis space that originally drove the stock above $50. (See Canopy stock analysis on TipRanks)

Tilray (TLRY)

The big-name Canadian cannabis company in the opposite position is Tilray The company has limited cash and a highly unprofitable business.

Tilray generated $52 million in Q1 revenues and analysts forecast Q2 revenues of ~$55 million. The big problem is the ongoing large losses. The company plans to get quarterly operating expenses down to $40 million, but Tilray only generates gross margins in the 29% range.

My biggest issue is that Tilray is plugged into a lot of different business with Canadian cannabis, U.S. hemp and international operations causing the large expense base. If the company had the balance sheet of Canopy Growth or Aphria, the spending levels wouldn’t be a problem.

Tilray ended March with $174 million in cash and had to raise $60 million in debt during February before completing an equity offering. Back in March, the company sold 7.25 million shares and warrants for net proceeds of $90.4 million.

Analysts have Tilray losing money for the next couple of years and the market isn’t going to find money-losing cannabis stocks very appealing in this environment. Investors should watch for the Canadian cannabis company to drastically reduce the quarterly EBITDA losses after losing another $21 million in Q1. Once Tilray gets to a position where additional funds aren’t needed, the stock can be removed from the ‘avoid’ list.

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclosure: No position.