With the volatility in the stock market and especially the cannabis sector these days, one way to invest for the long-term is to buy a basket of stocks. The sector has had so many pitfalls due to regulations and company missteps that buying multiple stocks helps reduce any company specific risk and increases the odds of picking a couple of long-term winners in the sector.

Investors should look at this as how a lot of the market participants invest in the biotech space. Picking winners in the sector can be difficult due to binary outcomes around drug testing and approvals. Investors buy baskets of biotech stocks since no investor wants to risk all of their capital to only one stock that could have a surprise negative outcome on a trial or FDA approval.

While the cannabis sector doesn’t have the same binary risk, the market does have a ton of regulatory risk and splitting up investments between Canadian and U.S. companies helps reduce the risk of any negative outcome in one country. In addition, the market has bounced around from a shift to high THC value brands from an expectation for premium cannabis strains with moderate THC levels.

The global cannabis market is still poised for substantial growth as the Canadian provinces allow additional retail stores and Cannabis 2.0 products expand and the U.S. continues to see state by state approvals of recreational cannabis. All while, international locations such as Mexico appear on the verge of approving cannabis use.

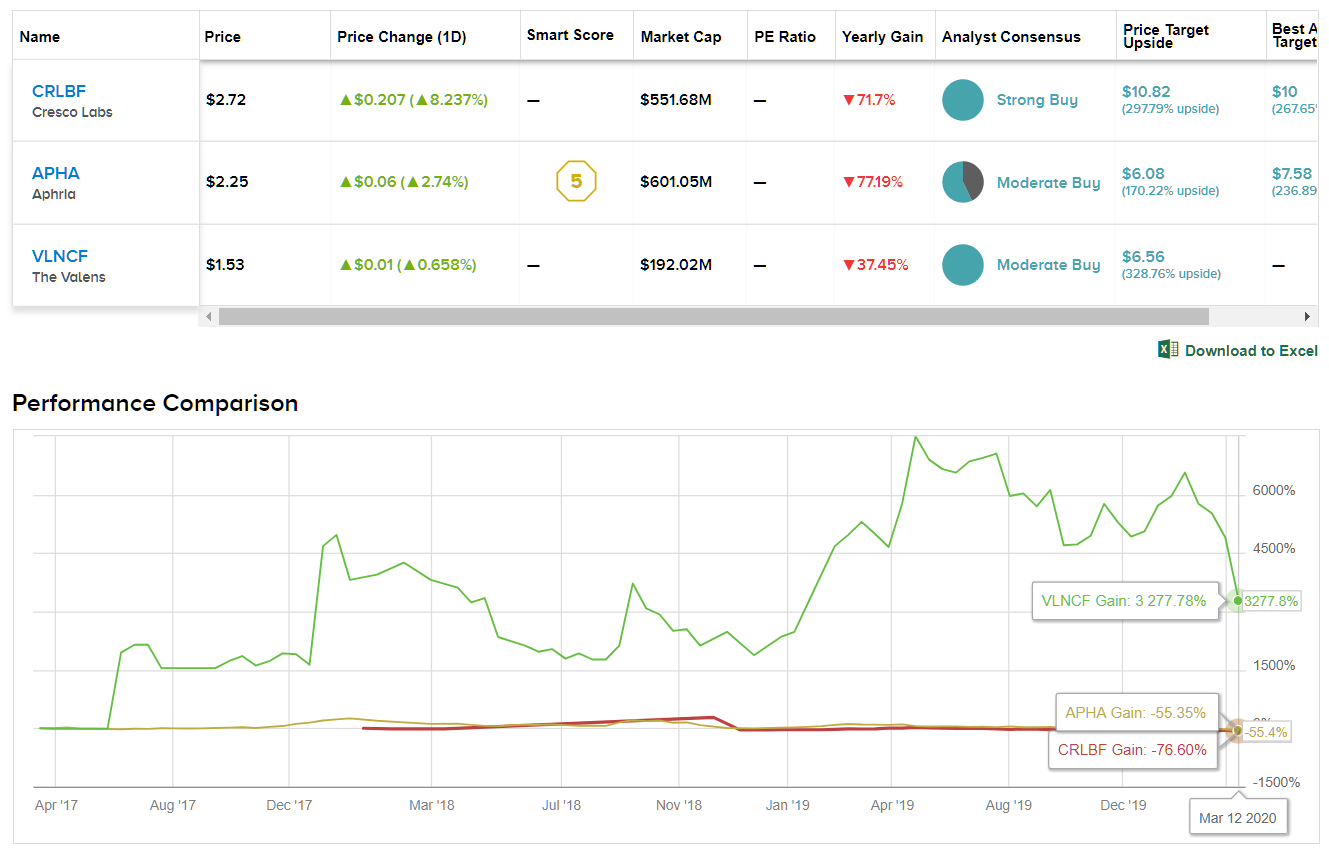

With that in mind, we’ve delved into three cannabis stocks with solid potential for rewarding shareholders, especially when purchased as a basket of stocks. Using TipRanks’ Stock Comparison tool, we lined the there side by side to get the lowdown:

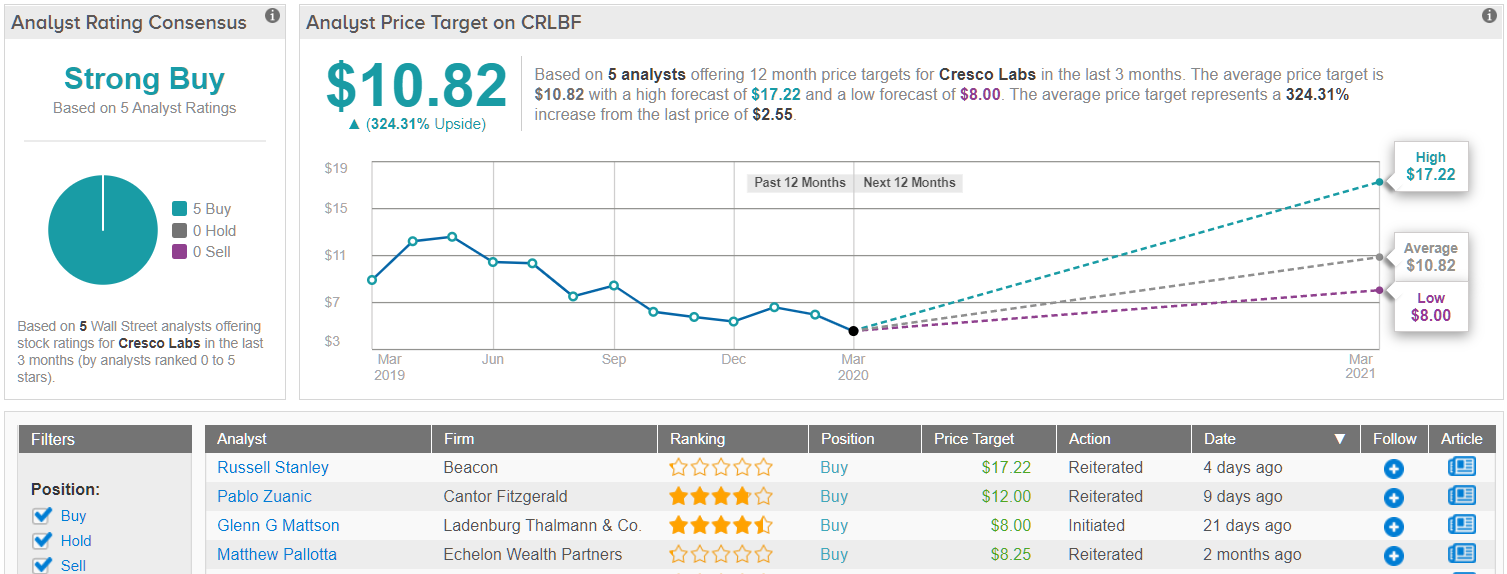

Cresco Labs (CRLBF)

The prime area to look first for an investment is within the U.S. multi-state operators (MSOs). Investors probably can’t go wrong with most of the stocks in the MSO space, but one favorite is Cresco Labs with legalization of recreational cannabis sales in Illinois.

The company just obtained approval for a dispensary in downtown Chicago bringing their total stores in the state to six. Cresco Labs has licenses to open an additional four dispensaries in Illinois. The market estimates are for sales topping $2 billion and possibly reaching $4 billion after the state reached sales of $74 million in only the first two months after legalization on January 1.

The MSO will soon have cultivation capacity of 243,000 square feet with the approval for three facilities to reach the largest capacity in the state at 630,000 square feet. Additionally, the company has operations in key markets like California, Arizona, New York, Ohio and Pennsylvania.

The stock has a listed market value of only $523 million following a Q3 in which the company reported pro-forma revenues of $73.6 million. The closing of the Origin House deal will boost 2020 sales to over $500 million with analysts predicting sales reaching $800 million in 2021.

In an upbeat report, analyst Glenn G Mattson of Ladenburg Thalmann explained why he is initiating coverage on Cresco Labs with a Buy rating and a $8 price target: “We believe that given Cresco’s attractive footprint, its sound long-term strategy and its record of profitability the company deserves a premium valuation. The introduction of adult recreational cannabis in Illinois, a state where Cresco maintains the top market share, is the key potential catalyst to propel revenue growth. This along with the prospect for other key states especially in the northeast to convert to adult recreational use later in 2021 should provide a significant catalyst for the company over the course of the year.” (To watch Mattson’s track record, click here)

What does the rest of the Street think? It turns out that they wholeheartedly agree with Mattson. With 5 Buy ratings and no Holds or Sells, the message is clear: Cresco Labs is a Strong Buy. If that wasn’t enough, the $10.82 average price target puts the upside potential at 324%. (See Cresco Labs stock analysis on TipRanks)

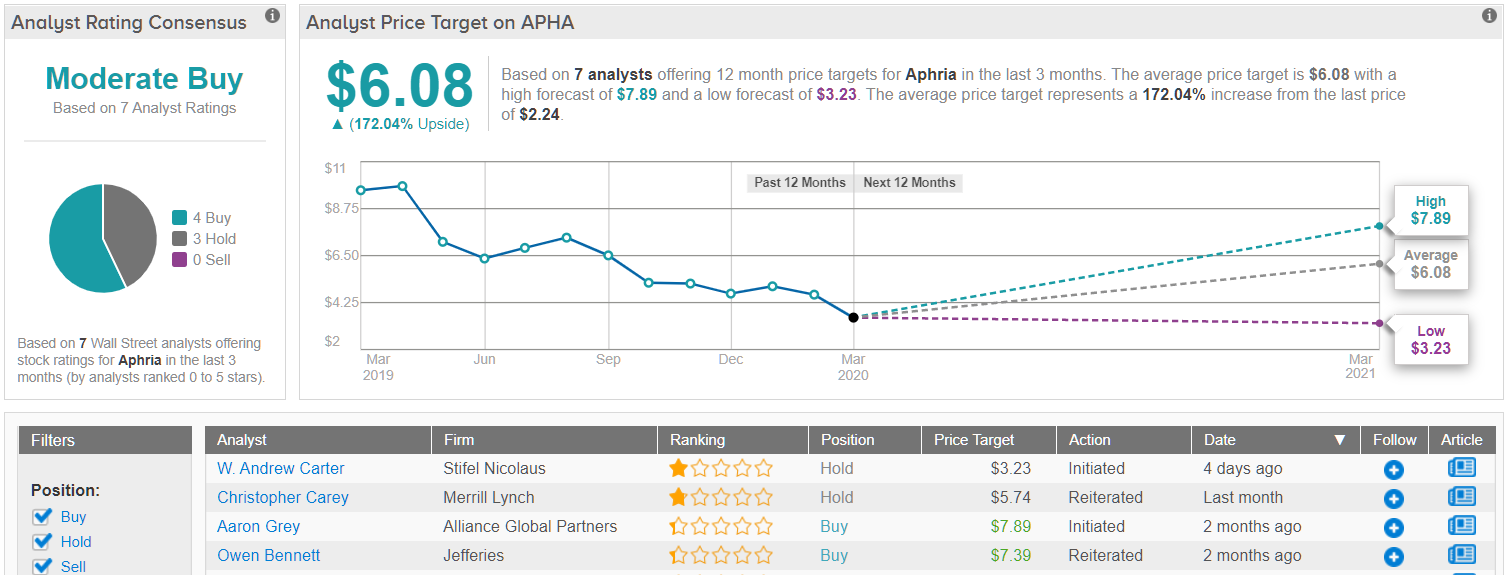

Aphria (APHA)

Even Aphria hasn’t been saved from the market selloff with the stock hitting new multi-year lows of $2.06. The company may not even meet recent guidance provided only a few months ago, but the market is now pricing in substantial weakness with the market value close to $600 million.

Aphria provides an investor buying this basket with access to the Canadian cannabis market and the potential to participate in global cannabis sales. The Canadian market is slowly heading towards opening more retail stores with Ontario starting to add 20 new stores per month in April and the slow roll-out of Cannabis 2.0 products.

The cannabis company recently guided to FY20 revenues in the C$600 million range with adjusted EBITDA of ~C$80 million. Analysts don’t have the company even hitting these targets, but revenues are expected to jump to C$715 million or $519 million in FY21 (May).

The recent license of their Aphria Diamond production site provides Aphria with access to more low-cost cannabis. The biggest risk to the story is over producing product in a weak sales environment with production capacity more than doubled to 255,000 kg of premium weed.

All in all, shares in APHA are priced at just $2.23, a bargain for a stock with over 170% average upside potential. That potential is derived from the average price target of $6.08. With 4 Buy and 3 Hold ratings given in recent weeks, the analyst consensus on APHA is a Moderate Buy. (See Aphria stock analysis on TipRanks)

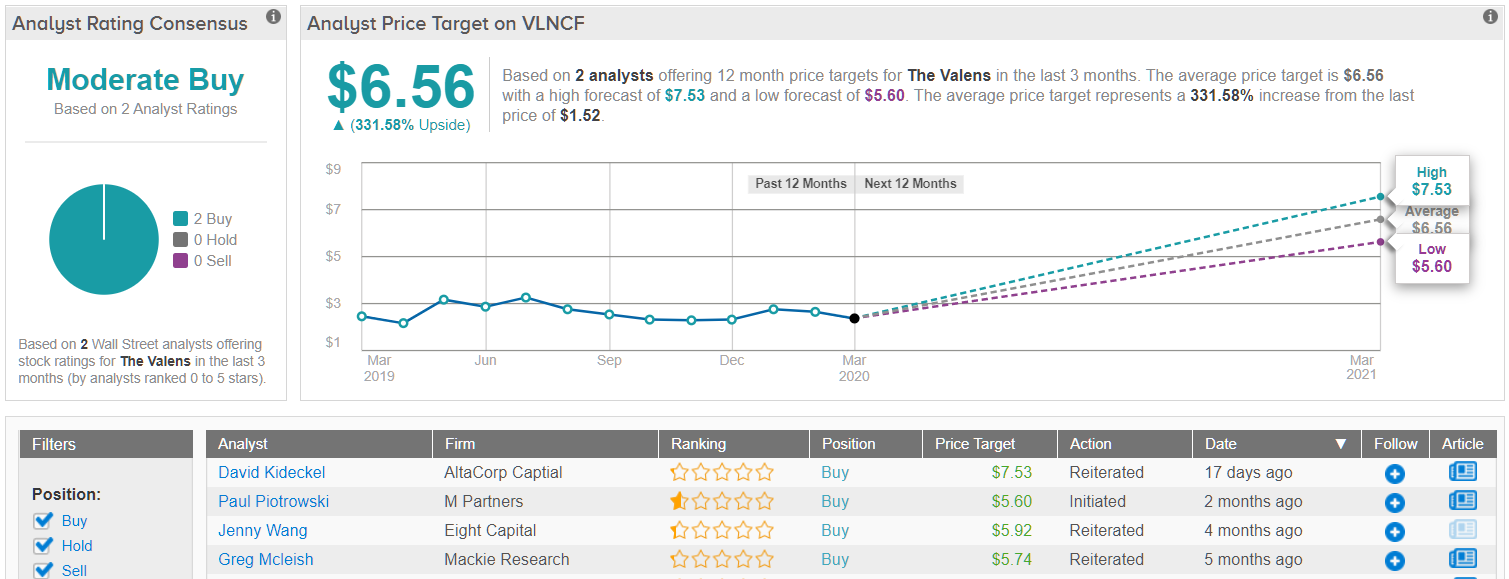

Valens GroWorks (VLNCF)

The wild card on this list is Valens GroWorks. The company focuses on cannabis extractions for oils and Cannabis 2.0 products.

The company recently reported revenues grew 86% during FQ4 ending in November to C$30.6 million. Valens even produced an amazing EBITDA of C$17.7 million for the quarter, or 57.7% margins.

The fear in the stock is that slowdowns in the cannabis sector will eventually hit the company. The focus on white-label products might save Valens from the destruction in the space.

After year end, the cannabis extraction company began formulating 19 SKUs to meet customer demands for Cannabis 2.0 products in the categories of vape pens, edibles and concentrates, amongst other categories. In addition, Valens recently bought Pommies Cider Co. to accelerate its entry into the cannabis-infused beverage space and edibles.

Valens only extracted ~24,000 kg of dried cannabis in the last quarter for an annualized rate of 100,000 kg. The company has expanded extraction capacity to 425,000 kg providing substantial upside growth potential as the Canadian market grows over time.

AltaCorp Capital analyst David Kideckel has Valens generating 2021 revenues of $246 million and adjusted EBITDA of $108 million. Both very solid numbers for a stock with a market value of only $178 million.

The stock only trades at slightly above 1.0x those sales estimates and 2.5x EBITDA estimates. With several growth opportunities, Valens provides an interesting stock for a basket of cannabis stocks.

Judging from the consensus breakdown, it has been relatively quiet when it comes to analyst activity. Over the last three months, only 2 analysts have reviewed Valens. Both of which, however, were bullish, making the consensus a Moderate Buy. On top of this, the $6.56 average price target puts the upside potential at 332%. (See Valens stock analysis on TipRanks)