Aphria (APHA) has had to battle itself out of a hole because of reputational issues coming from short-seller reports that suggested the company paid far too much for some of its foreign assets, along with deals that personally benefited some of its management at the time.

One thing to take into account is a number of those in the financial media have been hammering the cannabis industry in general concerning whether or not they overpaid for some of their assets, so it’s not something exclusive to Aphria, although it has had to endure the most visible and aggressive public attack in that regard.

While there remains some overhang from the assertions, the company has been showing signs of rebounding after getting hammered after the news went public.

According to interim CEO Irwin Simon, his major concern once taking over leadership wasn’t the issues surrounding the negative reports, but rather how the company was operating in a disjointed way.

He said this in early August in the Calgary Herald:

“There was not a strategic plan or vision. You had grow, marketing, sales, operations, Broken Coast (a licensed producer owned by Aphria) all in silos. So, you know, how do you pull all that together?”

Although concerns over the value of its international assets remain, the last earnings report and accompanying guidance point to the company possibly being able to sustainably increase production and sales.

While some believe guidance was too optimistic, if it is able to execute and meet its goals, it would be a huge boost to the value of the company.

A key issue weighing on the company

Something that refuses to go away concerning Canadian-based companies is what their strategy is to enter the U.S. cannabis market. Those that provide visible plans, such as Canopy Growth and it buying the rights to acquire Acreage Holdings if the U.S. ever legalized pot at the Federal level.

Other companies such as Aurora Cannabis have also been hit hard by the perception a company needs to reveal a U.S. strategy in order to command a premium price.

Aphria has to deal with the same issue, as it focuses primarily on the Canadian market and building out an international business. I tend to think the major reason it isn’t getting more interest from investors, beyond the short-seller reports, is its perceived lack of having a plan to compete in the giant U.S. cannabis market.

What’s interesting about that, now that Canopy Growth has faltered even with its U.S. entry plan known, some investors no longer appear to care about Aphria’s strategy for the U.S.

The point there is there is some schizophrenia in the market concerning this because of the double standard in regard to Canopy Growth and many of its peers. For Canopy Growth it was considered a major catalyst until it plummeted in value. Now with Aphria, some financial writers aren’t even talking about it because they’ve apparently transferred their optimism from Canopy Growth to Aphria, are aren’t including an American entry plan as important.

I’m actually in agreement with that, but because of the emphasis on the U.S. market with Canopy, it looks like Aphria, at least in part, isn’t getting the boost to its share price it could be getting based upon its current performance.

Aphria has what many in the market are looking for

For some time I’ve stated that revenue was going to be the major catalyst driving the cannabis industry, and I retain that belief. That said, the market is increasingly looking for the combination of sales growth and a clear path to profitability, or as in the case of Aphria, current profitability.

In the fourth quarter Aphria reported $15.8 million net income and adjusted EBITDA of $1.9 million.

While the company increased its recreational sales, it didn’t experience the lower costs associated with adult-usage pot, as it was able to increase its average selling price from $5.14 in the third quarter to $5.73 in the fourth quarter. At the same time it was doing that it managed to slash costs per gram from $2.85 in the third quarter to $2.35 in the fourth quarter.

It also closed a $335 million-plus convertible note offering in the fourth quarter at a 5.25 percent rate, bringing the total amount of cash on its books to $571 million.

That provides the company with flexibility and the ability to scale domestically and internationally.

It’ll also help it achieve the goal of producing up to 255,000 kilograms annually.

Conclusion

Aphria went through a tough period because of uncertainty concerning the value of its assets and behavior of some of its management. When that was happening the cannabis market in general started to take a beating because of concerns over an economic slowdown, and what the fallout from the trade wars would be.

Investors sought out safe havens at that point, which the volatile and more risky cannabis sector didn’t represent.

It’ll be interesting to see how this plays out for Aphria, especially with the very optimistic guidance from the company, which some are somewhat dubious about.

Since the company is trading at low multiples and has nowhere to go but up, if it does reach its guidance, the share price is going to soar. If not, I think it’ll still do fairly well over the long term, but in the short term it’ll go through more downward pressure.

My thought is Aphria’s management wouldn’t never have guided so positively unless it believed it really could reach its numbers. And if they don’t reach the numbers, how much the market punishes it will depend upon the severity of the miss.

The bottom line to me is Aphria looks good for the long term, assuming it can execute on its strategy, and even if it doesn’t present a plan to enter the U.S., it should be a solid performer on the top and bottom lines.

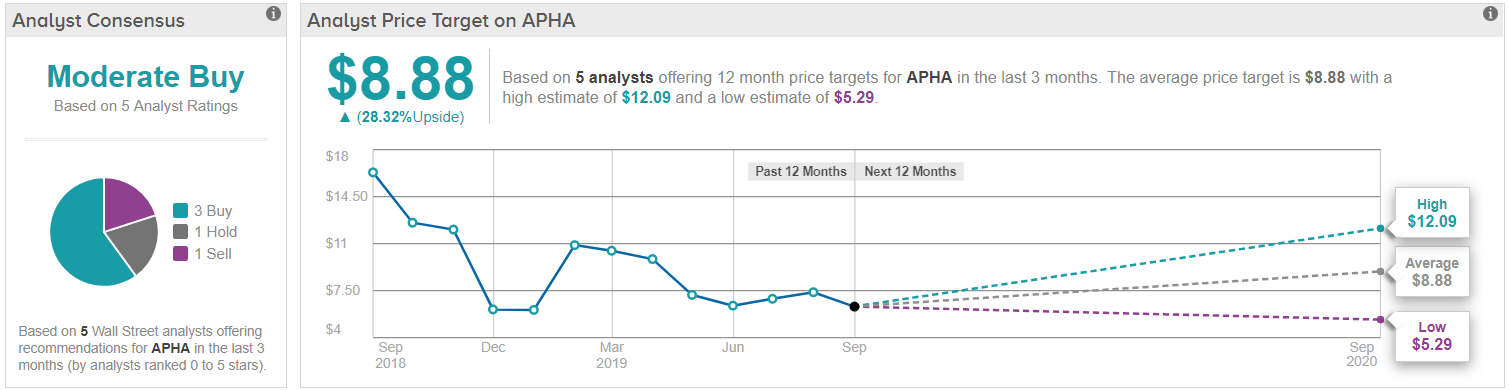

See APHA’s price targets and analyst ratings on TipRanks

Disclosure: No position.