Aphria (APHA) recently stated that it has received its cultivation license from Health Canada for its 51-percent owned Aphria Diamond subsidiary, which when fully operational, will have an annual production capacity of 255,000 kilograms.

Only Aurora Cannabis and Canopy Growth have more production capacity at this time.

In this article we’ll look at why the timing of the approval of the license is important to Aphria’s performance.

Recent performance

In its last earnings release in the middle of October 2019, Aphria revenue of $126.1 million, up 849 percent year-over-year. Sequentially, revenue climbed from $28.6 million in the fourth quarter to $30.8 million in the first fiscal quarter.

Aphria generated a profit for the second quarter in a row, generating net income of $16.4 million, or $0.07 per share. That was up from the $15.8 million or $0.05 per share generated in the fourth quarter. Last year in the first quarter the company had a loss of $0.09 per share.

Adjusted cannabis gross margin in the reporting period was 49.8 percent, down from the 53 percent in the prior quarter. The decline was attributed to a decrease in sales in higher margin items from temporary higher costs per gram, and a fire at its Broken Coast facility.

The company spent a lot more than normal in the quarter, finishing at about $100 million. Management stated that that amount of spending won’t happen in the quarters ahead, saying, “… outflows in the quarter included approximately $35 million for the final earn-out related to our CC Pharma acquisition, an important part of our German strategy, $5 million of one-time payments on our long-term debt, $30 million of CapEx and a $15 million increase in working capital supporting our increased production capacity.”

In the current quarter the company expects to have capital expenditures in the range of $20 million to $25 million. Requirements for working capital are also expected to drop in Q2.

At the end of the first quarter the company had $464 million of cash and marketable securities, positioning it for more than enough capital to handle its needs and growth.

Why the timing of licensing approval is important

The reason why Aphria is receiving licensing approval from Health Canada is opportunistic is because in the near future the company will be able to sell derivatives in Canada, grow revenue from the increase in pace of the opening of new retail stores in Canada, and the importance of international demand in the markets it has a presence in.

While the Canadian cannabis market has been underwhelming because of the low number of retail store outlets, that is finally starting to change, and over the next several years expectations are there will thousands of cannabis retail stores operational in Canada over the next several years.

That, combined with higher margin derivatives, will be major revenue and earnings growth catalysts over the next few years for Aphria.

Two of its more important international markets are Germany and Colombia. With its partnership with exclusive partnership with Colombia Medical Federation, the company has access to more than 70,000 doctors and other medical professionals.

In Germany, it was one of only three cannabis companies to be awarded with cultivation licenses.

The German medical cannabis market is expected to grow to more than one million patients by 2024, according to Prohibition Partners, with the German cannabis market potentially growing to $18 billion by 2028.

With the increase in production capacity, Aphria is positioned to meet the growing demand of cannabis around the world, and in Canada.

Consensus Verdict

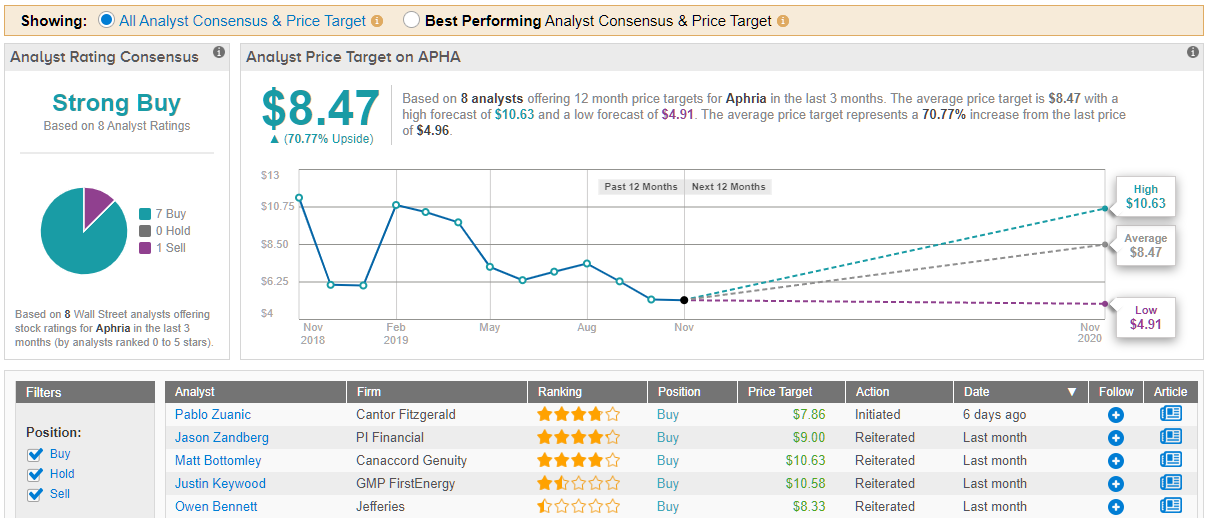

Wall Street loves the Canadian cannabis maker, scoring one of the most bullish consensus ratings of the cannabis universe. TipRanks analytics demonstrate APHA as a Strong Buy. Based on 8 analysts polled by in the last 3 months, 7 rate Aphria stock a Buy, while only one says “sell.” The 12-month average stock-price forecast stands tall at $8.47, marking about 70% upside from where the stock is currently trading. (See Aphria stock analysis on TipRanks)

Conclusion

For some time my thesis has been that the larger cultivators are going to overwhelm most of their smaller competitors because of their ability to supply the fast-growing global cannabis market.

With Aphria now becoming the third-largest Canadian producer behind Aurora Cannabis and Canopy Growth, it should be able to not only survive, but thrive in the years ahead.

Even though the lack of retail stores to serve the Canadian market give the impression of oversupply in that market, the fact is the demand remains strong, and once those stores are increased to significant levels, it will not only allow Aphria to scale, but help it take away share from black market operators that have been able to stay around longer and in larger numbers than originally anticipated.

As that is resolved, Aphria will not only increase sales from more retail outlets, but also from taking away share from its black market competitors in Canada.

With all of this unfolding, the timing of the approval of the license for Aphria Diamond couldn’t be better. Once it is fully operational, Aphria will be set to ride the long-term growth trajectory of the cannabis industry.

To find good ideas for cannabis stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.