My suspicion surrounding the stated reason for former CFO Mike Monahan leaving Hexo (HEXO) has been confirmed, as almost immediately afterward the company announced a revenue warning, as well as withdrawing its financial outlook for fiscal 2020.

It’s certain that Monahan changed his mind after going through the financials and taking into account the weakening sentiment in the cannabis market. I think he was looking forward to participating in an exciting sector that was about to take off, and rather, not soon after taking the CFO job, found the exact opposite.

The company would never confirm that one way or another, and in reality, it no longer matters. Why Monahan left has little impact on the performance of the company going forward. That said, losing the high-profile CFO does weaken the stature of Hexo at a time when it would have helped.

What matters going forward is how long it’ll take Hexo to recover, and how it’ll deal with cash burn as revenues continue to plummet.

The macro cannabis picture

For cannabis companies based in Canada, investors need to include the slow rollout of retail outlets in their models. More than any other factor, this has weighed on the performance of companies, and will continue to do so for at least two or three quarters.

The reasons for this is not only the lack of stores to sell out of, but also the propensity for many consumers to go to the black market for their cannabis needs.

Although there are those that have suggested supply is the culprit because it’s oupacing demand, that isn’t an accurate assessment of the situation. There is plenty of pent-up demand in the Canadian cannabis market. Again, the issue is the lack of physical stores to sell products in.

From the point of view of supply temporarily exceeding demand because of few places to sell from, that would be true. But for the overall market, there is still plenty of demand that current supply could meet if there was a place to sell it out of.

Eventually supply will exceed demand, but that time hasn’t arrived yet. For now, investors need to discount revenue until confirmation that many more physical stores have opened in Canada. This is especially true for Quebec and Ontario.

Changed outlook

The company guided for revenue in the quarter ended July 31 to be in a range of C$14.5 million to C$16.5 million. That is about a third less than the C$24.8 million consensus from FactSet.

In the short term the reason given for a decline in expected revenue was “lower than expected product sell through.” Other companies have pointed to similar reasoning, but it puzzles me because it has been clear for some time that Health Canada was far behind in the approval process for licensing of physical stores. Why this wasn’t pointed out much earlier doesn’t make a lot of sense to me.

What is surprising the market, in my opinion, is the fact the companies continued to operate under assumptions made early in 2019, where expectations were there would be a lot more retail stores to sell out of. But it has been apparent that wasn’t going to happen in the near future.

That means either Hexo believed it was going to be able to generate higher sales with or without the increase in outlets, or it failed to adjust its numbers to align with the market realities. The cost for that failure is the share price of the company getting hammered.

If that’s not bad enough, the company also downwardly revised it financial outlook for fiscal 2020, citing “regulatory uncertainty” concerning derivative products that are to be approved to be sold in Canada as of October, and to start to be sold in the latter part of December 2019.

Hexo management said the result is an “increased level of unpredictability.”

Consensus Verdict

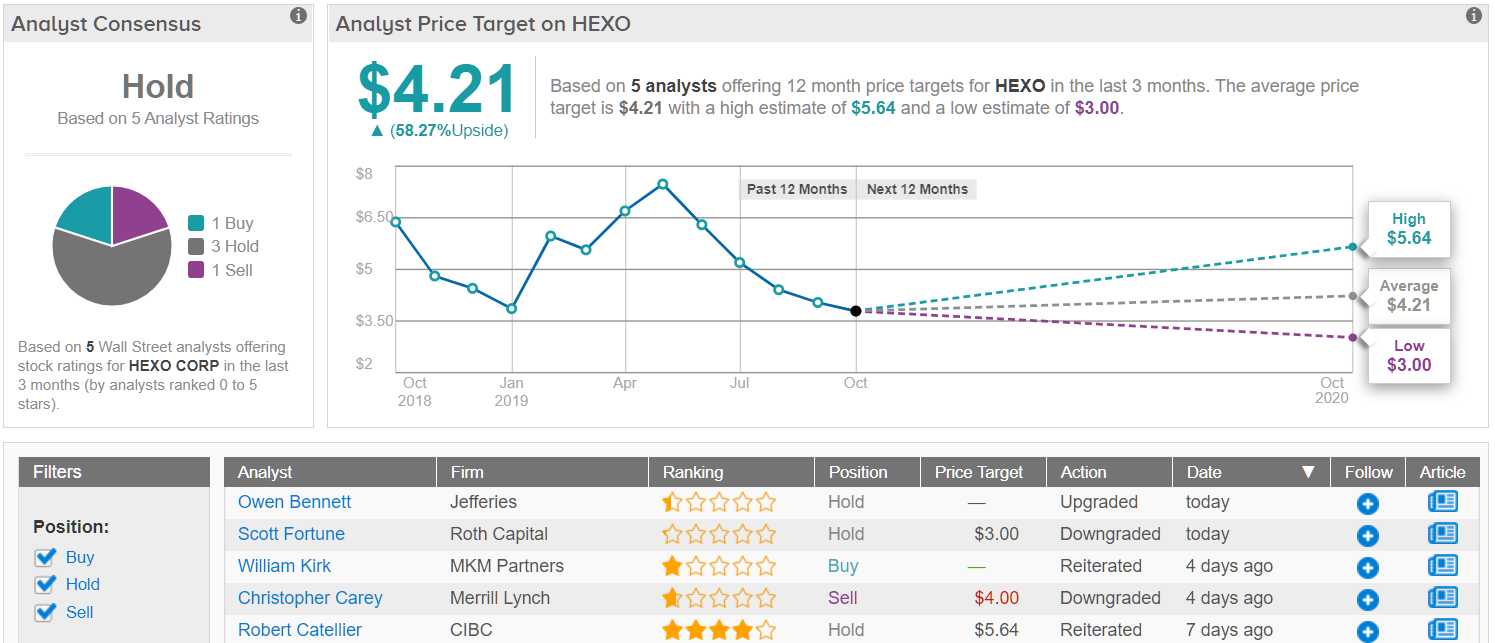

Most of Wall Street is surveying the troubled cannabis player from the sidelines, with TipRanks analytics demonstrating HEXO as a Hold. Based on 5 analysts polled in the past week, three rate a “hold” on HEXO stock, one says “buy”, and one recommends “sell.” (See HEXO stock analysis on TipRanks)

Unsurprisingly, investor sentiment is very negative, with individual portfolios in the TipRanks database showing a net pullback from HEXO.

Conclusion

For any of the Canadian companies, there was never going to be any meaningful impact on the top and bottom lines concerning derivatives until the first calendar quarter of 2020 because it will be the first full quarter of sales.

Even there investors probably need to lower expectations until there is further clarity on how derivatives will be handled in light of the health concerns associated with vaping.

Hexo had been getting a lot of positive momentum in the past from the company’s partnership with brewer Molson Coors, but as seen from Canopy Growth with Constellation Brands, and Cronos with Altria, having a big partner or deal in place doesn’t mean it’s going to result in improved performance.

The most important thing Hexo needs is for there to be a lot more physical cannabis stores in operation. While it’s not certain at this time it’s the only reason for the decline in sales, there is no doubt it’s the largest factor, as evidenced by peers like Canopy Growth and Aurora Cannabis, which also had a drop in expected sales.

Presumably this is only a delay factor for Hexo, and the company will return to an improved pace of revenue growth as more stores are opened across Canada. For now, it’s probably going to take two to three quarters before it reverses direction.

If you believe in the long-term growth narrative for Hexo, this would be a buying opportunity at the current share price.