As if there weren’t already enough challenges negative catalysts for HEXO (HEXO) to overcome, the recent resignation of its new CFO has generated questions on the health of its financial division.

According to former CFO Mike Monahan, the reason for leaving the company was in order to spend more time with his family. Yet, having been at the company for only about four months, it appears there was likely more to the issue because Monahan wouldn’t have taken the job in the first place if family time was a top priority.

That suggests something lacking in the company required more of his time than he thought when he made the decision to take the job. If so, it points to more problems ahead for HEXO, beyond the headwinds it already faced.

Major Concern

As some of my colleagues have pointed out, and I agree with them, it appears the reason for Monahan’s departure was related to his job requiring much more of his focus and time than he originally thought. It also means the financial division of the company has far more work to get it up to speed than the market generally is aware of.

What this has done is generated fears on what it is that really drove Monahan to leave so abruptly. There is no way the idea can be kept from the market concerning what is it within the company that isn’t known at this time.

Any time there is a perceived secret hidden underneath the hood of a company, it will cause investors to hold off until there is more visibility concerning the issue.

If Monahan had been a relative CFO newcomer to a public company, a potential lack of experience or lack of ability to move the company financial unit forward could be an explanation. But since Monahan is an experienced CFO that last worked at Nutrisystem, it does appear there is more to the story than lack of family time.

It also could be argued that there was miscommunication between HEXO and Monahan concerning time expectations and commitment, yet with his experience and the need for management continuity at HEXO, it’s hard to believe all those things weren’t openly dealt with. The idea time expectations weren’t on the table from the beginning is difficult to believe.

Bank of America’s Bullish Stance on HEXO Comes to an End

The stock market’s dim view of HEXO has gotten even dimmer.

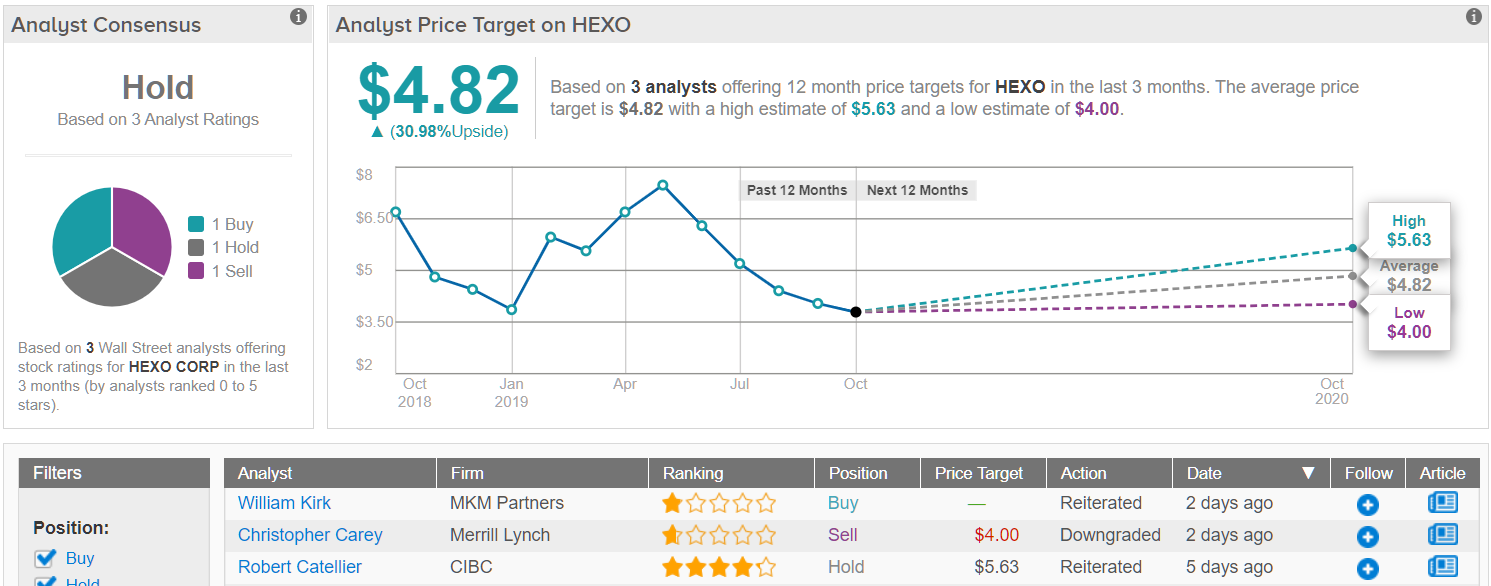

After hearing about Monahan’s departure, Bank of America analyst Christopher Carey wasted no time giving up his “buy” rating on HEXO. The analyst downgraded the stock to Sell, while slashing his price target to $3.00 (from $7.00), which implies about 20% downside from current levels. (To watch Carey’s track record, click here)

Carey commented, “While there were already risks for Hexo, we felt they were balanced by a sound core operation and a new CFO who had a chance to regain Street credibility on forecasts/guidance by resetting the bar, with the potential that momentum regained in CQ120 with the launch of value-add formats. Following [the departure] announcement, this broader thesis is simply untenable.”

Overall, this troubled cannabis player certainly has the Street divided, as TipRanks analytics indicate HEXO as a Hold. Based on 3 analysts polled in the last 3 months, one says “buy,” one suggests “hold,” while the third one recommends “sell” (you can guess who). The 12-month average price target stands at $4.82, marking a nearly about 30% upside from where the stock is currently trading. (See HEXO stock analysis on TipRanks)

Conclusion

With investors now scared off some by this latest event, it means the company may have to dig out of a bigger hole than it has been in from negative sentiment at the macro level of the cannabis sector, and from performance concerns in general. My view is the cannabis market won’t turn sustainably around until at least the end of the first calendar quarter of 2020.

There had been hope that Monahan, with HEXO’s margin strength, would be able to strengthen the balance sheet of the company and help stem some of its cash burn, which was at C$43 million last quarter, with a cash balance of C173 million.

As it stands now, HEXO has the additional headwind of investor suspicion on the condition of its financial department, and the probability it may need a lot more work on it before it reaches a more mature operational level.

Until the market knows, one way or the other, what is happening in HEXO’s financial division, I think it’s shares are going to remain under pressure. It can’t be done from the company making statements, restoring investor confidence will have to come from the next couple of earnings reports.