Analysts from Morgan Stanley and Cannacord recently weighed in on Tesla Motors Inc (NASDAQ:TSLA) and Nokia Corporation (ADR) (NYSE:NOK), following production delays and a court decision, respectively. One analyst remains bullish on Tesla, though decreases his price target, expecting half of Tesla’s guidance for 2020. The other analyst downgraded Nokia as a result of a disappointing outcome regarding the recent patent decision.

Tesla Motors Inc

Analyst Adam Jonas of Morgan Stanley recently weighed in on Tesla, highlighting production delays. The analyst noted past launch delays of the Model X due to “Manufacturing and engineering challenges” which have resulted in the addition of “hundreds of millions of dollars to costs” and the loss of customers. He also predicts a “slower ramp to ensure top quality of the early vehicles.” The analyst predicts a 2018 Model 3 launch, a year after the company’s prediction, as “Tesla’s technical resources have been diverted from other projects to ensure proper execution of X.” Additional reasons for his Model 3 production cuts include “low demand for electric vehicles categorically and globally in a $30 oil environment.” He continues that his 2020 vehicle delivery estimates are “less than half of Tesla’s 500k unit target.”

The analyst also weighed on Tesla Energy, reducing its valuation. He stated “The true cost of owning an energy storage unit appears even higher than we previously thought based on ‘all-in’ price quotes from SolarCity.” He continues, “This further suggests that the economics may not justify much of the gigafactory output being diverted to the power sector any time soon. Additionally, while only an indirect factor, we would be remiss not to factor in some greater degree of risk from low energy prices into our valuation of Tesla Energy.”

The analyst also states a recent greater interest in “electric, shared, and autonomous vehicles over the past 4 or 5 months” which relate to Tesla’s “core vehicle business and… shared mobility model.” He states that “competing efforts” from companies such as Ford, LG, and Google will only increase, predicting “further significant follow through with investment and collection of human capital.” As a result of this “competitive pressure”, he predicts higher deflation rate and increased R&D expenses for the company and is lowering his long–term OP margin rates and 2016-2017 EPS estimates.

Yesterday, the analyst maintained his Overweight rating on the company but lowered his price target from $450 to $333. Adam Jonas has a 44% success rate recommending stock with an average return of 11.6% per recommendation on TipRanks.

According to TipRanks’ statistics, out of the 14 analysts who have rated the company in the past 3 months, 6 gave a Buy rating, 3 gave a Sell rating, while 5 remain on the sidelines. The average 12-month price target for the stock is $286.25, marking a 45% upside from current levels.

Nokia Corporation (ADR)

Analyst Michael Walkley of Canaccord weighed in yesterday on Nokia following its award issued by the International Court of Arbitration regarding its arbitration with Samsung. This decision settles the amount that Samsung must pay Nokia for the five year extension of their license agreement to use Nokia patents, starting January 1, 2014. Following the settlement, Nokia’s annualized technologies division will have a net sales run rate of E800 million, “well below [the analysts] expectations” of E1.2 billion. He continues that he thought this segment would “deliver materially large and higher margin licensing revenue longer term with the Samsung Arbitration resolved.” As a result, the analyst is lowering his 2016 technologies division revenue and EPS for 2016 and 2017.

The analyst is also unsure about whether or not this deal will successfully “generate additional licensing revenue with Samsung.” He’s also unclear about other parts of the company’s licensing portfolio and states that this settlement creates a lower value and extended time period for signing up new licensees. The analyst also cites macro environmental concerns, anticipating that 2016 will have a “soft start” and “could represent flat overall sales growth.”

The analyst does cite a few positives, including the Alcatel-Lucent deal’s “product portfolio, technology leadership, and scale perspective.” He also comments on CEO Rajeev Suri’s past restructuring success and “strong leadership team” as catalysts for the integration of Alcatel-Lucent. Despite these positives, the analyst remains on the sidelines regarding the “disappointing licensing outcome.”

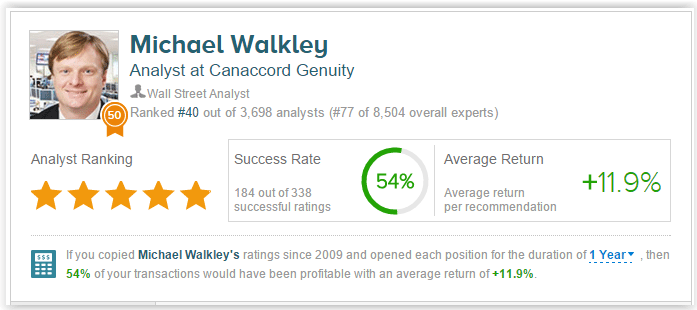

On February 1, 2016, the analyst downgraded the stock from Buy to Hold, decreasing his price target from $10 to $6.50. Michael Walkley is ranked #40 out of 3,698 analysts on TipRanks. He has 54% success rate recommending stocks with an average return of 11.9% per recommendation.

According to TipRanks’ statistics, out of the 5 analysts who have rated the company in the past 3 months, 3 gave a Buy rating while 2 remain on the sidelines. The average 12-month price target for the stock is $10.50, marking a 65% upside from current levels.