If there’s a theme surrounding marijuana analyst coverage of Aurora Cannabis (ACB) these days, it would be this:

Yes, Aurora is a great Canadian cannabis company. You don’t get to nearly $5 billion in market capitalization on a whim. Yes, it’s a leader, and yes, it might very well turn out to be one of the big survivors in the cannabis industry.

But man, oh, man! Would you look at that debt load?

In contrast to larger cannabis concern Canopy Growth (CGC), which has nearly $740 million in net cash on its balance sheet, or smaller HEXO (HEXO) — $105 million in net cash on a very small debt load, Aurora occupies the unenviable position of being a company with nearly $250 million in net debt — and its debt is growing by the day.

Make no mistake: There aren’t a whole lot of marijuana companies that you could call “healthy” today. Most are burning cash like it’s going out of style (the aforementioned Canopy and HEXO included). But the thing is, with cash in the bank, these companies can sort of afford to keep spending on growth (for a while at least). Aurora, a quarter-billion in the hole already, and burning through cash at the rate of more than $460 million a year at last report, maybe cannot.

This is the crux of the reason why earlier this week, CIBC analyst John Zamparo announced he is initiating coverage of Aurora stock with only a “neutral” rating and a C$7 price target. (To watch Zamparo’s track record, click here)

“Aurora has demonstrated a clear presence as a leading Canadian producer,” concedes Zamparo, noting that the nearly C$100 million in cannabis that Aurora moved in Q2 was about 40% better than its nearest competitor could manage. The company is capturing market share in Canada, and even “beyond Canada’s borders.”

In Europe, for example, its “international revenues should continue to grow” as it competes in an industry suffering from a shortage of EU Good Manufacturing Process-certified (EU-GMP) facilities. Already, Aurora is selling about 12,000 kilograms per year of product, and on track to double its revenues to C$28 million in fiscal 2020, then nearly double again to C$50 million in fiscal 2021.

And yet, it’s this very production capacity that Aurora boasts of that’s contributing to analyst worries about the stock. “The company’s ongoing investments in non-GMP cultivation capacity,” warns Zamparo, could “generate limited returns.” From a condition characterized by product shortages earlier this year, by 2020, he predicts that domestic cannabis supply will “reach 3x that of demand” — probably causing prices to plummet.

Worse, 2020 is the very year in which Aurora will be called upon to repay its “$230 million convertible debenture” (in March). Unless Aurora can find some way to finally start generating cash in an environment of rapidly falling marijuana prices (most analysts don’t expect the company to turn free cash flow positive before 2022 by the way), Aurora may be forced to take on new debt to pay off its old debt — or more likely, dilute its shareholders with yet another equity issuance to raise the cash it needs.

In that regard, it’s worth pointing out: From June 2017 to June 2019, Aurora has already roughly tripled its share count as it sold shares to raise cash. Sadly for the stock’s early investors, who have seen their ownership stakes severely diluted, it seems Aurora is every bit as good at selling shares, as it is at selling marijuana.

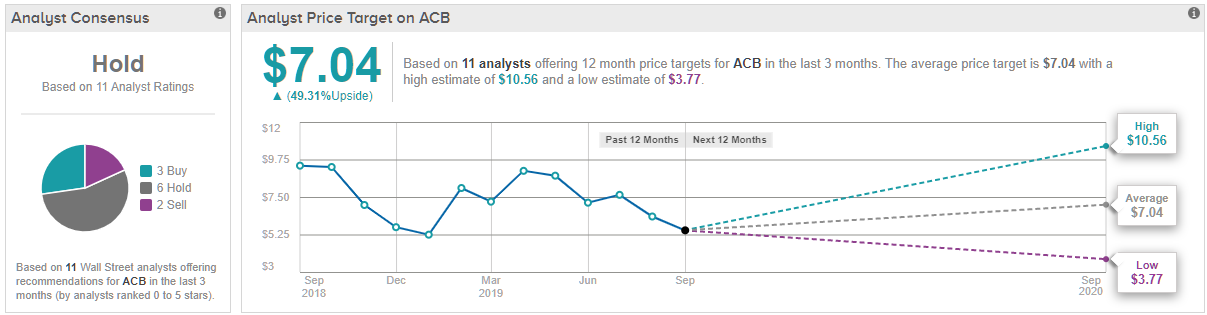

Wall Street believes Zamparo is smart to play it safe when it comes to Aurora’s prospects ahead, as TipRanks analytics reveal ACB as a Hold. Out of 11 analysts polled in the last 3 months, 3 are bullish on Aurora stock, 6 remain sidelined, and 2 are bearish on the stock. That said, the consensus average price target points to $7.04, or nearly 50% upside potential for the stock. This suggests that by consensus expectations, for now, the bulls win on Aurora. (See ACB’s price targets and analyst ratings on TipRanks)