With estimates forecasting the global cannabis market to reach $66.3 billion by 2025, analysts and investors alike are placing bets on which stocks in this emerging industry are best positioned to reap the biggest rewards from this significant opportunity. While the space is subject to regulatory headwinds and is many years from realizing its full potential, some companies have resonated with analysts as potentially lucrative investment opportunities. Here are three stocks with Moderate Buy consensuses that are expected to dominate in the competitive cannabis landscape.

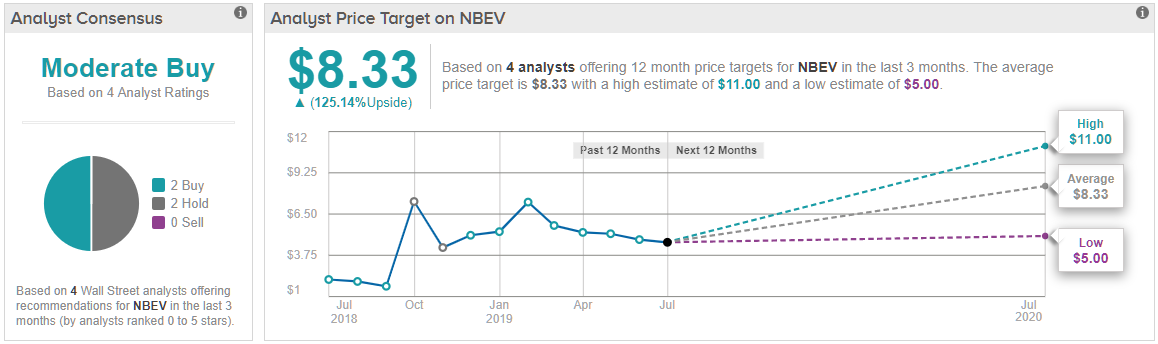

Is New Age Beverages Stock a Buy with 200% Upside?

New Age Beverages (NBEV) produces and distributes healthy functional beverages that are lauded for being all natural and organic. Adding to their existing line of dietary supplements and ready-to-drink beverages, NBEV is developing a line of CBD-infused beverages. In December, the company announced that it is acquiring Morinda Holdings for a cash-and-stock deal worth $85 million. The deal is highly favorable for the company as it now has access to Morinda’s larger product portfolio and distribution network in 60 countries around the world.

Roth Capital analyst David Bain agrees that the acquisition is beneficial as it will allow NBEV to be global in its CBD launch. Bain’s bullish sentiment is demonstrated through a Buy rating and price target of $11 (200% upside!), which is the highest price goal for the stock among analysts (To watch the analyst’s track record, click here).

Bain noted, “Checks cite a June +48% month-over-month result for Morinda China. We believe the Morinda China’s June result gives visibility for NBEV’s CY19 $320mm revenue guidance (while also boosting 2Q19 results).”

Bain notes that New Age’s 2Q19 gross revenue guidance of ~65mm could prove conservative considering the recent China and Japan Morinda results but feels that maintaining CY19 guidance would serve to bolster NBEV’s current valuation.

With promising synergies from the recent acquisition on the horizon, Bain is not alone in his bullish outlook on NBEV stock. TipRanks analysis of 3 analysts shows a Moderate Buy consensus, with two analysts saying Buy and one recommending Hold in the last three months. The average price target among these analysts stands at $8.33, which represents ~125% increase from current levels. (See NBEV’s price targets and analyst ratings on TipRanks)

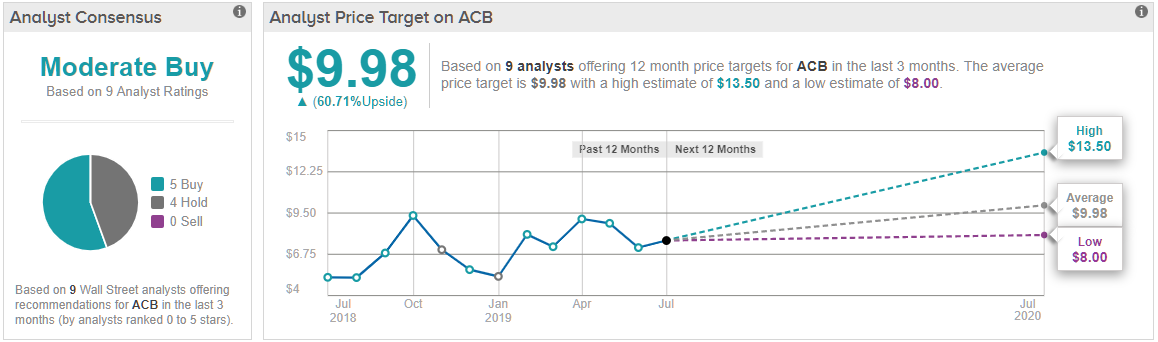

Aurora Cannabis Has Plenty of Juice to Rally Higher

Aurora Cannabis (ACB) is the world’s second largest cannabis company by market cap. It is a licensed producer of marijuana in Canada with sales and operations in 23 international countries. ACB’s production profile allows it to reach an expected annual run rate of over 625,000 kg per year.

Cowen analyst Vivien Azer’s belief that Aurora’s cultivation footprint “provide ACB with the necessary infrastructure to weather early storms in adult use while continuing to grow higher-value revenues in the medical market.” That’s enough for Azer to rate the stock a Buy with a C$15 price target, which implies nearly 140% upside from current levels. (To watch Azer’s track record, click here).

Azer points out that in addition to its leadership position in capacity, Aurora’s growing supply will also serve to bolster profitability. Further, through its large-scale production network and near-term operating leverage, ACB distinguishes itself as one of the few Canadian LPs positioned to reach positive EBITDA as soon as 4Q19 at a time when many peer companies in the industry have struggled with profitability.

Beyond Aurora’s current operational rigor, many believe that the announcement of a major partnership could be a significant catalyst for Aurora’s stock. Azer expects “ACB to add at least one strategic partner in 2019 (likely brokered by strategic advisor Nelson Peltz) with the company focused on opportunities across a number of consumer and medical verticals.”

Despite acknowledging potential obstacles ACB could face including increasingly restrictive regulatory roadblocks and lower than expected consumer demand, Azer is still steadfast in her belief that “ACB should trade at a premium to the peer group given its near term path to profitability in conjunction with strong early stage execution within the nascent Canadian cannabis adult use market.”

All in all, given the infrastructure ACB has built to take advantage of the always-changing market, Azer is confident that Aurora is well-positioned to dominate globally. Wall Street is almost evenly split between the bulls and those choosing to play it safe. Based on 9 analysts polled in the last 3 months, 5 rate ACB stock a Buy, while 4 maintain a Hold. Notably, the 12-month average price target stands at $9.98, marking a nearly 60% in return potential for the stock. (See ACB’s price targets and analyst ratings on TipRanks)

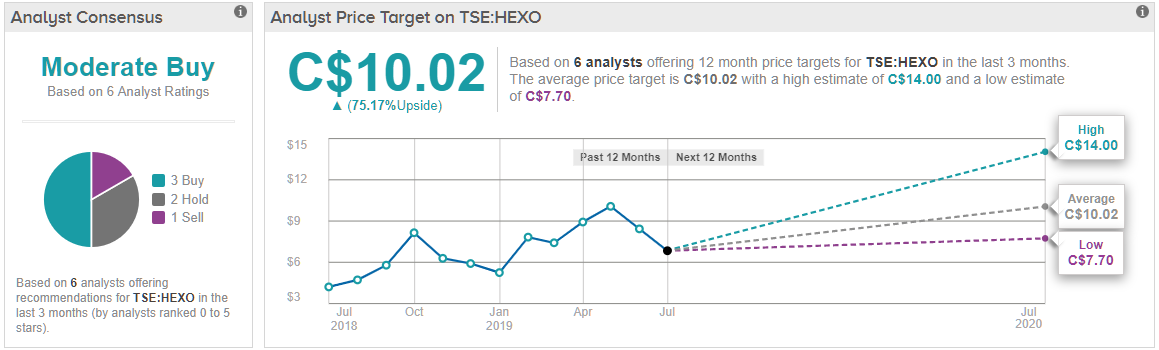

This Analyst Likes HEXO Stock… Should You?

In July, HEXO Corp. (HEXO) uplisted to the NYSE with the clear intent of attracting long-term investors. Looking back, HEXO received a lot of buzz after announcing its joint venture with Molson Coors Brewing that will focus on cannabis-infused beverages. Beyond this value-add partnership––which opens the company to what could become a $1.4 billion canna-beverages market by 2023––HEXO is an innovation-forward organization with an impressive growing pipeline of differentiated products.

Desjardins analyst John Chu looks at HEXO’s ramped up production and 4Q FY19 and FY20 net revenue guidance as promising potential upside for the stock. With a bullish outlook for the company, the analyst rates HEXO a Buy rating with a C$14 price target, which implies nearly 144% upside from current levels. (To watch Chu’s track record, click here).

Chu believes that HEXO’s infrastructure, which prepares it for edibles legalization, positions the company to have a major first-mover advantage over most of its peers and capture a fair share of the Canadian market. The analyst notes that “signs point to industry sales improving on the back of increased distribution in Québec, Ontario and Alberta, which should benefit HEXO given its production ramp-up” of its new greenhouse and Belleville facility. With continued expansion projects, the company should be able to overcome the previous bottleneck and accommodate higher packaging capacity.

Even though HEXO is losing money more slowly than its larger peers, near-term margins could face headwinds as the company expands its capacity. On the back of a 20,000kg supply contract with Québec, however, the analyst has more confidence in HEXO’s sales outlook than other companies in the industry. In fact, Chu shares that “there are fewer companies focused on advanced products (eg edibles) and/or that a limited number of those companies will have products ready when legalization starts.” Beyond its ambitious plans for Canadian legalization and to be a top 3 player in Canada, HEXO is positioning itself to be in eight U.S. states by the end of 2020 and plans to have a few Fortune 500 partners by then.

With HEXO primed to reap the rewards of its hard work, Chu is not alone in his support of the company, as TipRanks analytics showcase HEXO as a Moderate Buy. Out of 6 analysts polled in the last 3 months, 3 are bullish on the stock, 2 remain sidelined, while 1 is bearish. Worthy of note, the 12-month average price target stands at C$10.02, which implies nearly 75% upside from current levels. (See HEXO’s price targets and analyst ratings on TipRanks)