Following a woeful year, the end of last week provided a sense of turnaround for investors of Aurora Cannabis (ACB). The stock shot up over 90% after the release of a better-than-expected earnings report.

The company delivered on several key issues weighing on investors’ minds ahead of the results. First of all, Aurora delivered much better sales than anticipated. Revenue of C$75.5 million beat the consensus calls for C$67 million, and represented 18% quarter-over-quarter growth. Recreational cannabis sales jumped 24% to CA$41.5 million, boosted by the success of value brand Daily Special’s February launch.

Cost cutting measures have also been bearing fruit, significantly reducing cash burn in the quarter. The company exited the quarter with C$230.2 million of cash in the coffers.

Additionally, the company’s aim of reaching positive adjusted EBITDA in FQ2021 appears on target. Although still a way off from being positive, Aurora reported an adjusted EBITDA loss of CA$45.9 million, (excluding one-time staff reduction termination costs), a vast improvement on the previous quarter’s adjusted EBITDA loss of CA$80.3 million.

Bottom line, though, the company is still losing money, with a FQ3 net loss of CA$137.4 million, or CA$1.37 per share, far above the consensus estimates of CA$0.77.

Even though CIBC analyst John Zamparo believes Aurora is “making progress on cost cutting, while increasing its consumer market share and maintaining its leading medical business,” the analyst points out that the company still has “much work to do.”

A particular issue needs solving, and quickly, according to Zamparo: “Regardless of progress on cost cutting, if Ontario stores do not start opening in the somewhat near future, industry revenues will not reach the levels required for most firms to reach profitability, and we believe Aurora is no different. A spike in online sales is encouraging, but nowhere near sufficient to supplant brick and mortar. As Ontario goes, so goes this industry.”

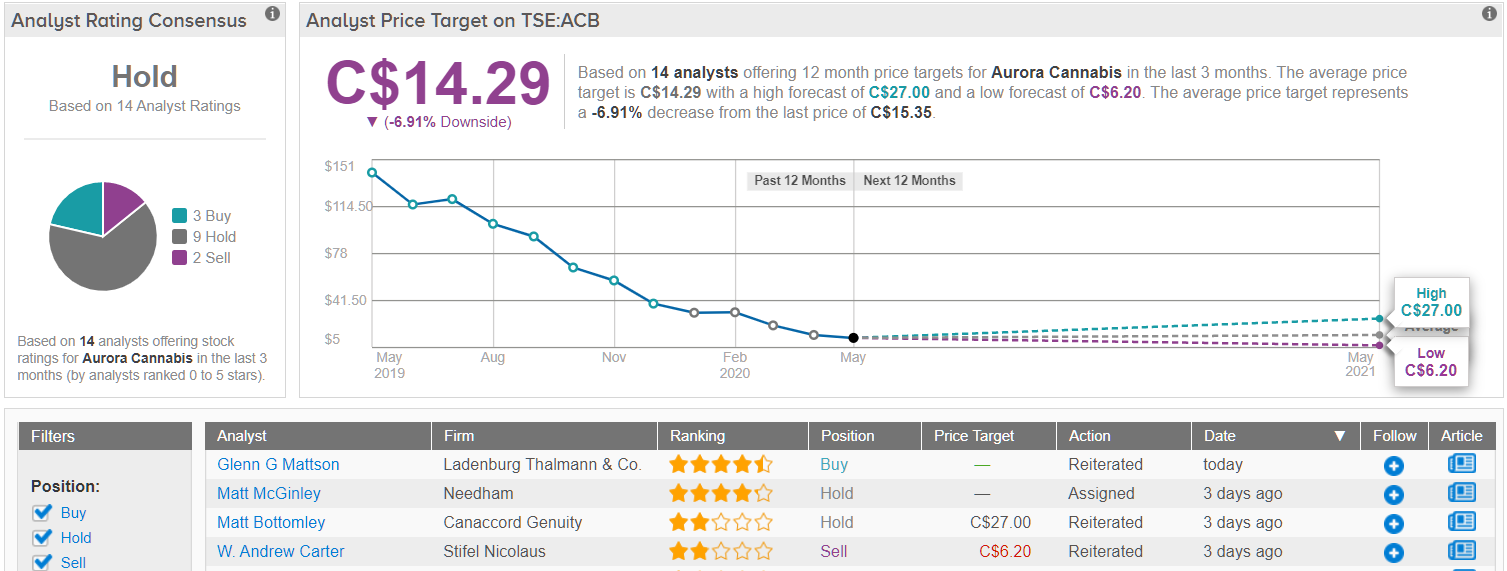

To this end, Zamparo reiterates a Hold rating on Aurora shares, while lowering his price target from C$27 to C$14. The figure represents possible downside of 9% from current levels. (To watch Zamparo’s track record, click here)

Zamparo’s assessment gets the rest of the Street’s backing. A Hold consensus rating is based on 9 Hold ratings, 3 Buys and 2 Sells. The average price target is slightly above the CIBC analyst’s, and at C$14.29 implies downside of 7%. (See Aurora stock analysis on TipRanks)

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.