The hope for a big rebound in the Canadian cannabis market continues to fade towards mid-2020. Aurora Cannabis (ACB) was positioned for a boost from Cannabis 2.0 sales, but the lack of Ontario stores, slow distribution and restrictions by other provinces will put a damper on initial sales. In addition, the global growth story is fading just as fast, delaying any imminent sales gains until mid-year.

Lack Of Ontario Stores

With a robust assortment of Cannabis 2.0 products becoming available to consumers on December 17, Aurora Cannabis faces a double whammy as Ontario slowly moves forward with new stores in 2020. The Alcohol and Gaming Commission of Ontario (AGCO) recently announced a plan that will license about 20 new stores per month beginning next April, but the market was hoping the province would move forward with up to 40 stores per month starting in January.

The new plan won’t see Ontario cross 100 cannabis stores until next summer, while the smaller Alberta province already has over 350 stores. The problem for Aurora Cannabis is that the company has limited Ontario stores to sell product as it hits the market with new vapes, edibles and beverages. The new product formats won’t find a home in Quebec either.

Investors really have to question how the company is going to grow revenues meaningfully enough to eliminate large EBITDA losses in an environment where Germany sales are halted, and the lack of new Ontario stores limits the growth prospects in Canada. Aurora Cannabis generated September quarter revenues of $57 million. Analysts have December revenues growing to $61 million, with March reaching $77 million. With all of the market headwinds, these numbers appear aggressive.

Italy Problem

According to Benzinga, Aurora Cannabis’ supplies most of the imported medical cannabis products to Italy. However, the government is now promoting a domestic provider to expand cultivation to meet demand.

One major thesis all along has been the likelihood that international markets actually shrink cannabis imports. Governments will eventually push domestic companies with local cultivation facilities that employ the citizens of the related country. Aurora Cannabis has been supplying Italy with cannabis from the Netherlands, and the Italian government would clearly like the imports to stop.

The Italian market only consumed 578 kilograms of medical cannabis in 2018, but the market is expected to have seen substantial growth this year. Stabilimento Chimico Farmaceutico di Firenze is expected to increase annual production from 200 kilograms to 500 kilograms next year.

Aurora Cannabis doesn’t have a large international sales figure outside of Germany, but this global growth catalyst is slowly fading away. Germany product sales are already halted as the health authorities investigate a new procedure for attaining a longer shelf life on their cannabis products, and any investor should expect other countries will take the same path as Italy.

Analysts Weigh In

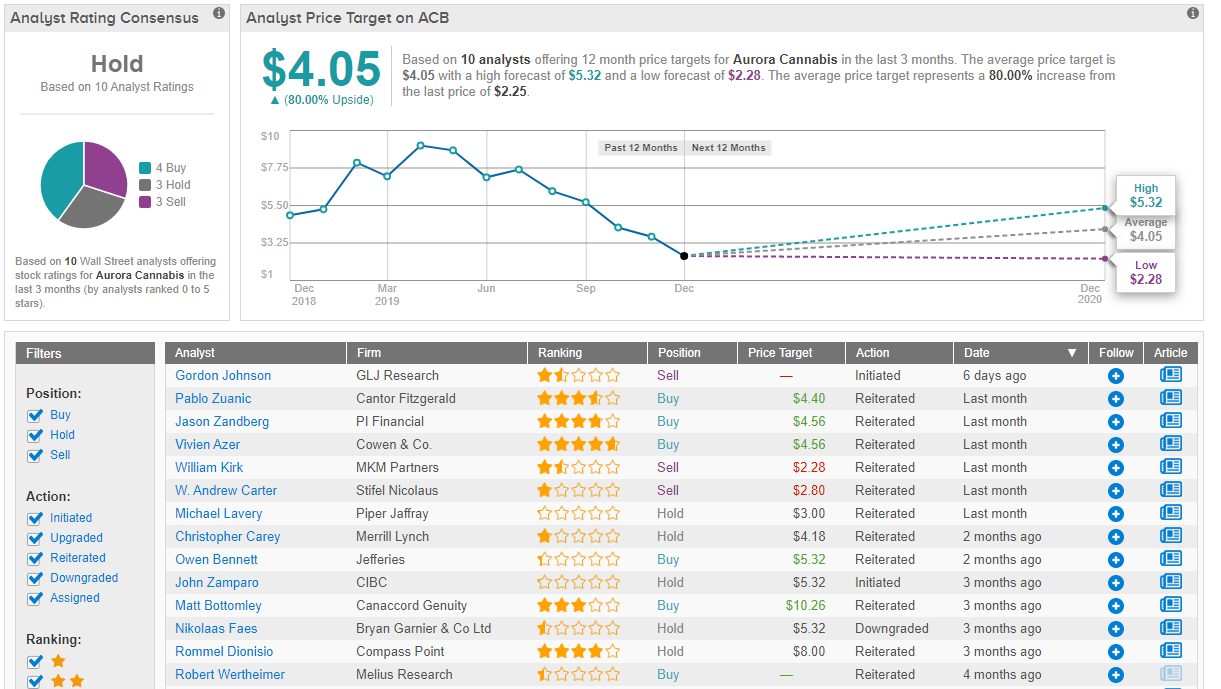

Based on the consensus breakdown from TipRanks, a company that tracks and measures the performance of analysts, opinions are spread out when it comes to ACB. With 4 Buy ratings, 3 Holds and 3 Sells received over the previous three months, the word on the Street is that the stock is a Hold. However, the $4 average price target suggests shares could climb 80% higher in the twelve months ahead. (See Aurora price targets and analyst ratings on TipRanks)

Takeaway

The key investor takeaway is that Aurora Cannabis faces more delays in Canada and new roadblocks in international locations. All of the catalysts for 2020 continue to get pushed back and turned into a mid-year story.

Disclosure: No position.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.

Check out these 5 ‘Strong Buy’ stocks that top Wall Street analysts recommend.