Aurora Cannabis (ACB) announced it was going to cut 500 jobs, with 25 percent of them being corporate positions, while taking impairment charges of about $752.79 million. It also announced CEO Terry Booth would be stepping down from his position, with executive chairman Michael Singer taking over leadership of the company until a new CEO is found.

In this article we’ll look at what Booth stepping down could mean for the strategy of the company going forward.

Long-Term Position on Cash Infusion

The position of Aurora Cannabis for some time has been to resist the idea of getting a huge cash infusion from a larger firm, which would result in losing control of company.

With Chief Commercial Officer Cam Battley being forced to step down in December, this could result in significant changes to its former resistance to losing some, if not all control, of the company going forward, assuming a large suitor takes in interest in the company while it has lost a lot of its valuation; it could take a position and control for a lot less than it could have even a couple of months ago.

I think the key there will be how Nelson Peltz feels about the future prospects of Aurora, and if it remains viable or desirable to continue to go it alone.

Nelson Peltz Factor

In March 2019, Nelson Peltz was taken on as a strategic adviser by Aurora, which also granted him 20 million stock options he can acquire at C$10.34 each.

The assumed primary purpose in bringing on Peltz was to help open doors for partnerships with larger consumer packaged-goods companies, without giving up control via large cash infusions.

One of the major disappointments for Aurora since that announcement has been the failure of Peltz to deliver any type of deal that would have changed the performance of the company, even as the Canadian government dropped the ball on rolling out retail stores.

The big question in the months ahead is whether or not Peltz changes his mind concerning the control factor and decides to push for an agreement with a large company interested in taking a significant position in Aurora at a bargain price.

It wouldn’t even surprise me if a company, knowing the future prospects for Aurora, were to make a bid to acquire it altogether.

Some may think of the debacle surrounding Constellation Brand’s investment in Canopy Growth, citing resistance to acquiring Aurora because of the write-downs Constellation has had to take because of the weakness now inherent in the cannabis market.

The point is, with Battley and Booth out of the way, it’s almost certainly on Peltz as to whether or not the company is going to change its mind on seeking an investment from another firm, or believes it can continue to go it alone.

Peltz can be aggressive, and if he doesn’t want it to happen, I don’t think it will. On the other hand, if he pushes for it, the doors will open for a perspective suitor.

The main issue here is if things don’t go the way Peltz wants them to, it could result in litigation that few companies would want to engage in, taking into consideration it could take several quarters before Aurora starts to turn around in a meaningful way.

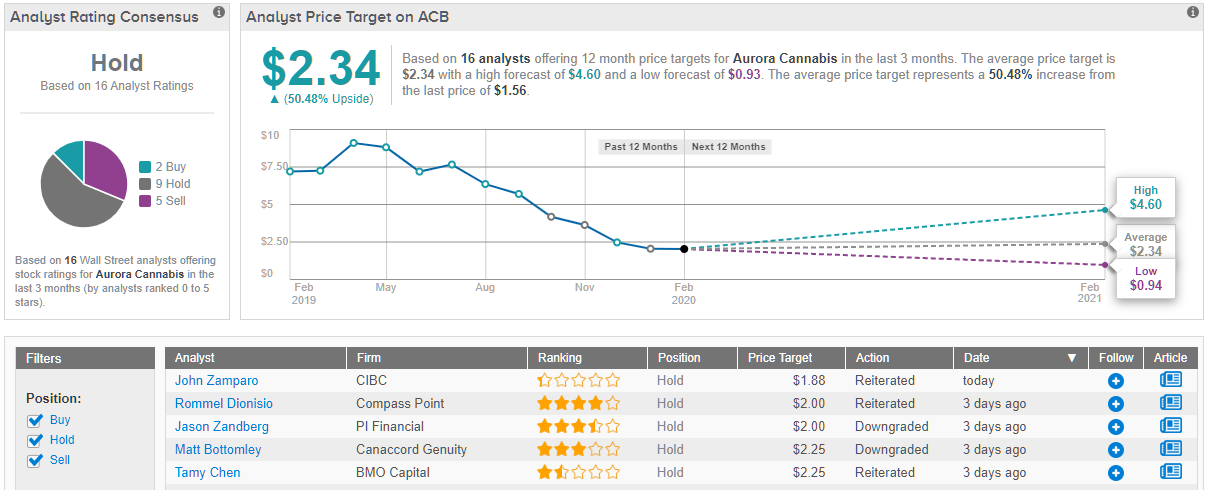

Consensus Verdict

Caution roars loud on Wall Street analysts surveying the challenged cannabis giant’s prospects. Out of 16 analysts tracked in the last 3 months, only 2 are bullish, while 9 remain sidelined and 5 are bearish on the stock. Yet, the stock’s consensus price target stands tall at $2.34, which implies about 50% upside from current levels. (See Aurora stock analysis on TipRanks)

Conclusion

No investor should consider taking a position in Aurora because of a possible acquisition, or even a potential partnership deal with some packaged-goods companies.

Under current Canadian cannabis market conditions, it would be best to wait until anything like that is announced, than to take on the risk in the short term. The short-term risk/reward isn’t worth it at this time.

We still have to wait and see if Ontario really does aggressively roll out stores in the last three quarters of 2020, as it has stated it will. If it doesn’t, there really isn’t much Aurora can do to turn things around this year.

Selling derivatives will help some, but until the new stores are rolled out, the company is only selling into the existing Canadian market. More stores to sell in, along with the potential of derivative sales and new customers, is the key to its success until the international medical cannabis market increases in size.

For these reasons, I remain bullish on Aurora Cannabis over the long term, but will wait until the earnings report for the first calendar quarter of 2020 to see how derivatives are doing for the company, and in the second calendar quarter, whether or not Ontario is starting to add a lot more retail outlets.

If the company does publicly signal a willingness to listen to offers from companies wanting to take a large position in it in exchange for cash, it could be a huge catalyst beyond its general performance.

The company is in a holding pattern until the above questions are answered.

To find better ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.