The good news for GW Pharmaceuticals (GWPH) was it generated a profit in its latest reporting period. The bad news is it was the result of a $104.1 million one-off sale of its Rare Pediatric Priority Review Voucher in the quarter. The better news is its core product Epidiolex significantly exceeded sales expectations, and should retain growth trajectory going forward.

In this article we’ll look at six reasons GW Pharmaceuticals should continue to find support, even though it’s certain it’ll have a loss in its next reporting period; albeit the losses should continue to narrow. It’s probably not too long before the company starts to produce a sustainable profit.

Positive Catalysts for Epidiolex

The first three of the six reasons to like GW Pharmaceuticals in the future are associated with its flagship product Epidiolex, which accounted all but $3.6 million in revenue for the quarter.

First, sales of Epidiolex wildly exceeded expectations, as it had net sales of $68.4 million in the second quarter, far above the $47 million analysts on average were looking for. Total company sales in the quarter came in at $72 million.

Next, health care prescribing by health care providers has been increasing, with over 12,000 patients now having used the treatment since it launched in 2018. At this time over 2,500 physicians have prescribed Epidiolex, with the vast majority of them continuing using the therapy, according to Chief Executive Justin Glover.

Last, private and public payers don’t appear to have any qualms about covering Epidiolex, with approximately 93 percent of them covering it in the U.S. market.

That suggests sustainable performance in the quarters ahead, although the pace of that growth may not be what it was in the last quarter.

Probable New Treatments for Epidiolex

I put this 4th reason to like GW Pharma into a separate category because it points to future potential and not the existing use of Epidiolex. It’s highly probable that the company will gain approval for using the drug in Europe, but that has yet to be confirmed.

GW Pharmaceuticals is awaiting the approval of the EU for using Epidiolex to treat Lennox-Gastaut syndrome (LGS) and Dravet syndrome in the early part of October.

It would be surprising if the company didn’t receive approval, and its fairly safe to at least this will be another revenue stream for the company.

Assuming approval, it would launch first in the two largest European markets, Germany in France, with the goal of doing so some time in the fourth quarter. After that it’ll launch in Italy and Spain in 2020.

More speculative is its research on how Epidiolex may be effective on treating Rett syndrome. It has plans to launch a clinical study to determine if Sativex can be used to treat spasticity in multiple sclerosis patients. The goal there is to obtain approval to use the treatment in the U.S.

Finally, it has started to look at recruiting participants in a study that will determine if cannabidivarin can effectively treat autism.

Most important here is GW Pharmaceuticals is working on building out a pipeline that would generate meaningful long-term growth for the company, if a number of them are cleared to treat patients. This would significantly increase it patient base, revenue and earnings.

Solid Balance Sheet and Cash Position

Investors should understand that even with all the positive sentiment surrounding GW Pharmaceuticals, it’s still going to burn through a lot of cash as it ramps up research and expands to other markets.

In the near future it’s not going to have another one-time sale of an asset to offset the spending in its earnings results.

That could be extremely detrimental to a number of weaker cannabis companies, but GW Pharma has under $30 million in long-term liabilities at this time, and a lot of cash on hand to keep the company from having to issue equity to raise capital, which would dilute existing shareholders’ shares.

At the end of the reporting period GW had cash and cash equivalents of $583.7 million. That’s only about $8 million less than it had at the end of calendar year 2018.

The company should obtain some approvals in the near future, and that will generate more revenue and earnings to bolster its balance sheet. It won’t immediately catch up with spending, but it does show a path to profitability that it can obtain with probably little need to increase its share count.

So the fifth thing to like about GW is it has a strong balance sheet and cash on hand to spend on research and growth without diluting its shares.

Analysts Still Bullish on the Company

The sixth reason to like GW in the future is it still attracts a lot of bullish sentiment from analysts.

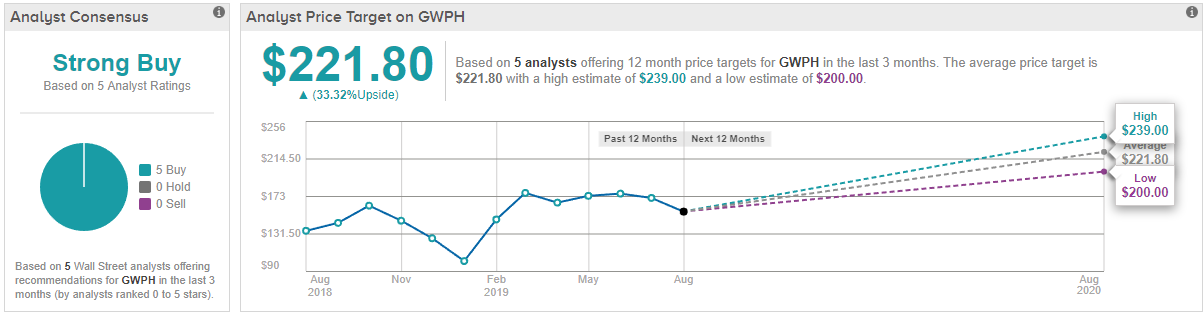

Both Oppenheimer and Stifel Nicolaus raised their price targets on GW, with Bank of America/Merrill Lynch retaining its ‘buy’ rating on the stock.

Oppenheimer raised its one-year price target from $234 to $239, and Stifel Nicolaus boosted its one-year price target from $227 to $228.

Overall, TipRanks reveals that GWPH has a Strong Buy analyst consensus rating with 5 back-to-back ‘buy’ ratings in the last three months. Meanwhile the average analyst price target of $221.80 suggests the stock has upside potential of just over 30% from the current share price for the next 12 months. (See GWPH’s price targets and analyst ratings on TipRanks)

Although I don’t make my long-term investment decisions on the outlook and estimates of analysts, many investors do, and in the case of boosting their bullish case for a stock, usually provides a higher floor and ceiling.

Combined with the other positive catalysts above, it should provide further upward trajectory for the share price of the stock, assuming GW doesn’t drop the ball in some way.

Conclusion

There is a lot to like about GW Pharmaceuticals, especially the future potential of Epidiolex and other potential treatments in its pipeline, which will without a doubt generate significant revenue if they’re approved, And as mentioned above, some of the less speculative are close to certain to being approved in the EU, which will open up another revenue stream.

With the overall health complex in the U.S. having a positive response to Epidiolex at various touch points, this is going to be an ongoing growth engine for GW; investors will probably need to lower expectations on future growth trajectory, even though the company surprised so strongly on the revenue side in the latest quarter.

I don’t believe it has reached an incremental growth stage yet, but eventually it will. By that time it should have other markets to sell into, partially offsetting the slowing sales trajectory in the U.S. in the future. That time isn’t here yet, but it’s not a long way off. It could happen within a year in the U.S. market.

The pace and timing will be determined on how consumers think concerning moving away from competitive drugs into the perceived safety of Epidiolex. If it gains more U.S. market share, its growth trajectory could last longer than I’m expecting as the company stands today.

With a strong balance sheet and cash position, along with the potential to grow out its product pipeline in new markets and treatments, the long-term future of GW Pharmaceuticals looks very profitable for those in it for the long haul.

GW Pharmaceuticals boasts an 8 score from TipRanks Smart Score. That’s thanks to a combination of bullish datapoints, including a ‘Strong Buy’ consensus from the Street, bullish blogger opinions, and even positive sentiment from investors. (More details here)