The vast majority of the cannabis market has been beaten down over the last year as the market is concerned about a myriad of issues in the once hyped sector. The Canadian sales aren’t living up to expectations after recreational cannabis legalization in October 2018 and the U.S. companies are facing issues with raising capital at reasonable costs due to a lack of cannabis legalization on a federal level.

The global market is still forecast to top $200 billion in annual sales in the distant future, but investors always need to remember that companies have to survive the present market. The cannabis sector is rife with opportunities under the surface while the majority of the media headlines focuses on the major Canadian LPs that obtained lofty valuations in the initial market over reaction to the potential cannabis opportunity.

Market darling Aurora Cannabis (ACB) is down over 60% from the 2019 peak over $10 and the stock has lost ~28% from the starting price for the year. The original IPO hype from Tilray (TLRY) sent the stock surging to $300. In the months following, the Tilray has lost up 90% of the peak value and the stock is down nearly 70% YTD. A whole list of dozens of Canadian and U.S. cannabis stocks have suffered similar fate in 2019.

The market isn’t all bad, but investors haven’t made any money this year chasing the well-known names. We’ve delved into these three cannabis companies that have generated stock gains in 2019 and are poised for more upside going into 2020:

Trulieve Cannabis (TCNNF)

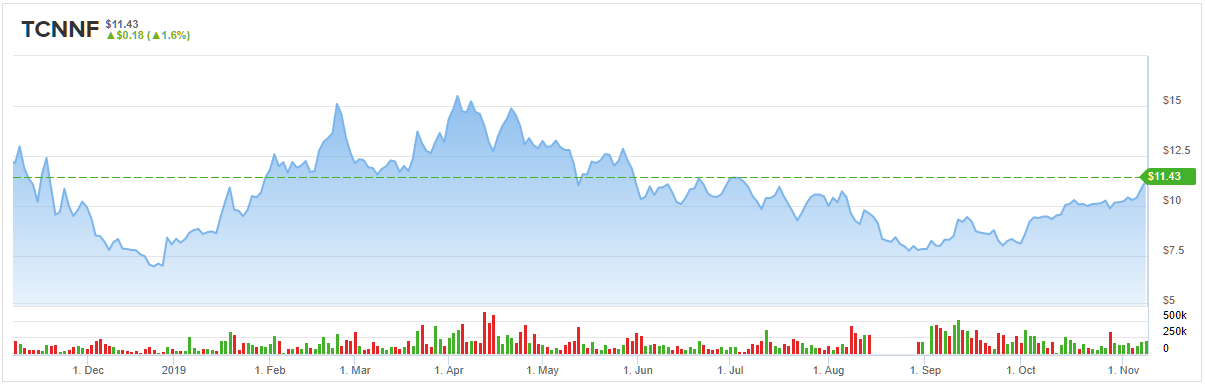

Though Trulieve Cannabis is down from the highs above $16 this year, the stock started the year around $8 and has generated a 35% gain YTD with the current move above $11. The U.S. multi-state operator (MSO) based in Florida avoided the high-profile acquisitions around the market peak that has snagged the other major MSOs. The company focused on profitability over pure revenue growth and the stock has rewarded shareholders this year.

Trulieve recently opened their 39th store in Florida and is slowly moving beyond a Florida focus while most other players took the aggressive expansion plan to reach operations in as many states as plausible. The company now has plans to enter California, Massachusetts and Connecticut plus a couple of other states this year via minor deals where Trulieve will only have one or two retail dispensaries in each of these news states at year end.

Even without aggressive acquisitions, the company still produced 149% revenue growth in the June quarter. The most impressive part of the Trulieve story is that the company has 65% gross margins and only spends mid-20% of revenues on operating expenses to generate a substantial EBITDA margin.

The stock has a market value of $1.2 billion with revenue targets approaching $400 million in 2020. The company generated over $31 million in adjusted EBTIDA in the last quarter alone allowing for more stock gains with these strong bottom line metrics in a market where most companies produce loses.

All in all, Wall Street is quite positive on this ‘Moderate Buy’ stock; Trulieve has received 2 ‘buy,’ and one ‘hold’ ratings in the last three months. Running the numbers across the Street, the 12-month average price target lands at $19.62, representing over 70% upside from current levels. (Find out how the Street’s average price target for Trulieve breaks down)

Village Farms (VFF)

Another company that has generated stock gains this year is Village Farms, despite a scathing report from Citron Research back in April. The research firm known for aggressive short positions suggested the company had so many red flags the stock should be valued at $1.

While half the cannabis sector stocks are actually trading at $1, Village Farms is now up over 140% from the January price in the face of these allegations. The company created a 50%-owned JV to turn greenhouses growing vegetables into a cannabis cultivation business that has worked better than planned.

The stock is worth $412 million, and Village Farms generated $53.5 million in quarterly revenues with $12.1 million from the Pure Sun Farms JV. The ability to generated $4.6 million in EBITDA from converting existing facilities and producing low-cost cannabis has won over investors.

The Pure Sunfarms JV is already working on doubling annual cannabis production to 150,000 kg with the ability to further increase expansion to 330,000 kg via other greenhouses. In addition, Village Farms is busy building up a domestic U.S. network of land in Virginia, North Carolina, South Carolina, Colorado and Texas to grow hemp to extract hemp-based CBD oil.

Analysts only target the company generating $230 million in 2020 revenues providing for substantial upside as additional cannabis and CBD supplies reach the market including recent expansion into higher margin branded products. Village Farms falls into the group of stocks with more upside having not been hyped this year due to the Citron report.

TipRanks’ data shows a bullish camp backing this cannabis player. The ‘Strong Buy’ stock has amassed 4 ‘buy’ ratings in the last three months, with no ‘hold’ or ‘sale’ ratings. The 12-month average price target stands tall at $31.76, marking nearly 284% in return potential for the stock. (See Village Farms stock-price forecast and analyst ratings on TipRanks)

Medicine Man (MDCL)

As the year started, Medicine Man hardly had a visible business in the cannabis sector. The company only generated 2018 revenues of $9.4 million while ending the year with only $3.4 million in current assets.

The stock started the year trading at just above $1 and currently trades above $3 after reaching $4 as recently as September. The main driver of the stock price was an acquisition spree to snap up assets in Colorado following new regulations via the passing of HB19-1090 allowing for the consolidation of the industry via outside investors such as Medicine Man Tech.

Over the course of six months since the passing of the bill in May, Medicine Man Tech. has bought a dozen companies pending approvals not expected until early 2020. The company forecasts the businesses generating 20% EBITDA margins with a goal of reaching 30% margins via collaborative growth and economies of scale.

The major problem with the story is the lack of visibility of the financials from all of pending deals. The company reports Q3 result on November 11, but none of these businesses will be on the books yet. The stock still isn’t well known by the general investing public so any success by Medicine Man Tech to consolidate these businesses into a high margin business would reward shareholders. (Get TipRanks’ free stock analysis report on Medicine Man)

To find good ideas for cannabis stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.