The vast majority of the Canadian cannabis sector gets beaten down almost every day. The Canadian cannabis sales aren’t living up to expectations after recreational cannabis legalization in October 2018 and the provinces over ordered product during Q2. The vast majority of the sector faced returns and allowances that crushed the sector during the recent Q3 reporting season.

Despite a global market still forecasted to top $200 billion in annual sales in the distant future, investors need to focus on the present market conditions in the Canadian cannabis sector as the global opportunities are still mostly limited. The Canadian sector still has major catalysts in 2020 with the Cannabis 2.0 rollout and the eventual retail store expansion in key provinces like Ontario.

On the recent earnings call, Canopy Growth forecast the potential for Ontario to open 40 retail stores a month during 2020 after operating with only 24 stores since early April. The big question remains whether the government will actually open up the market to such a large degree.

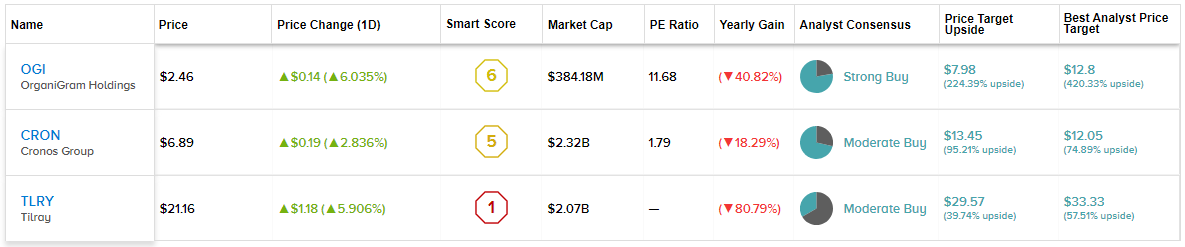

The stock market has been mostly bad in 2019, but investors now need to look at the opportunities in beaten down cannabis stocks. We’ve delved into these three cannabis companies that missed the market in Q3 that investors need to watch for a rebound in 2020:

Stock Comparison Tool | TipRanks

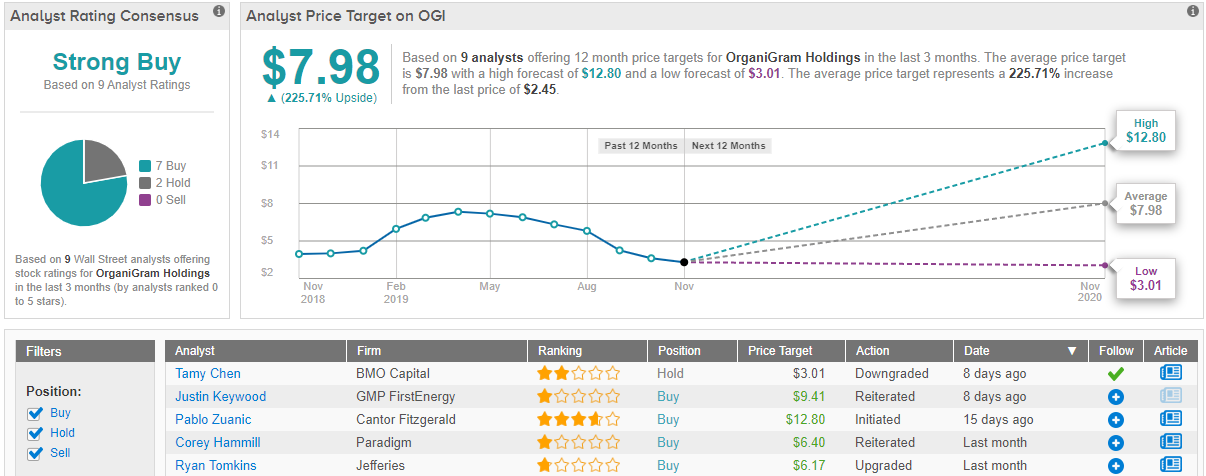

OrganiGram (OGI)

OrganiGram Holdings is down about 70% from the highs above $8 back in May. Last week, the company released a corporate update where revenues were set to miss the mark due to product returns and pricing adjustments.

For the June quarter, OrganiGram generated revenues of $24.8 million setting the stage for a big year. Instead, the company forecasts FQ4 revenues of only $16.3 million. Not only did shipments decline sequentially to $20.0 million, but also the company was faced with $3.7 million in provisions.

The end result was a Canadian cannabis LP proudly reporting adjusted EBITDA profits for FQ3 suddenly turning into a FQ4 loss. While OrganiGram suggests FQ1 sales are higher than the comparable period in FQ4, the company isn’t an expected leader in the initial rollout of Cannabis 2.0 products.

The company forecasts only entering the market when open mid-December with vape pens. Chocolate infused-edibles aren’t expected until the March quarter with beverages not reaching the market until sometime in the June quarter.

OrganiGram ended the August period with $47.9 million with an equal amount of debt. For this reason, the company filed a preliminary base-shelf prospectus for up to $175.0 million.

The company has a listed market cap of $350 million with analysts now forecasting FY20 sales of $122 million. The valuation is very reasonable for the sector making the stock a buy as OrganiGram raises more cash and once the 2.0 rollout gets into full force around Q1 to Q2.

If we step back and look at the analyst consensus, we can see that overall the stock has a ‘Strong Buy’ rating. In the last three months, the stock has received 7 “buy” ratings versus 7 “holds.” With an average analyst price target of $8, analysts are projecting upside potential of 225% from the current share price. (See OrganiGram stock analysis on TipRanks)

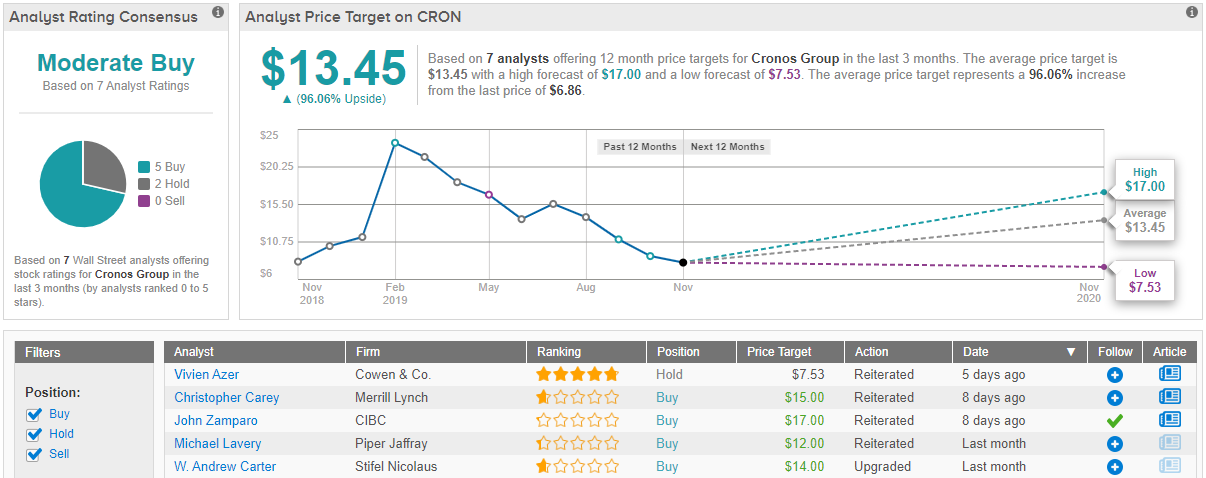

Cronos Group (CRON)

The Cronos Group missed revenue estimates for Q3 by over $1.3 million, but the company still grew revenues sequentially. The stock still hit new lows as the cannabis company has failed to generate anything meaningful out of a large cash hoard.

For Q3, Cronos generated $12.7 million in net revenues while the market cap is still up at $2.2 billion. The company has only generated $29.4 million in revenues for the nine-month period.

Where the company really disappointed investors was selling 8x the kg in the September quarter at half the net revenue per gram. The company ramped up production at no real benefit to shareholders with rates dipping to $3.75 from $7.18 last year.

The major catalyst for Cronos Group is a cash rich balance sheet. The company ended the quarter with C$1.5 billion on the balance sheet placing the enterprise value as only $0.7 billion.

If the company can wisely use this cash balance to snap up competitors on the cheap and consolidate the industry, Cronos has the ability to invest while other players are cash strapped.

CRON has a cautiously optimistic Moderate Buy consensus rating from the Street. This breaks down into 5 “buy,” and 2 “hold” ratings in the last three months. We can also see from TipRanks that the average analyst price target is $13.45 – 96% upside from the current share price. (See Cronos stock analysis on TipRanks)

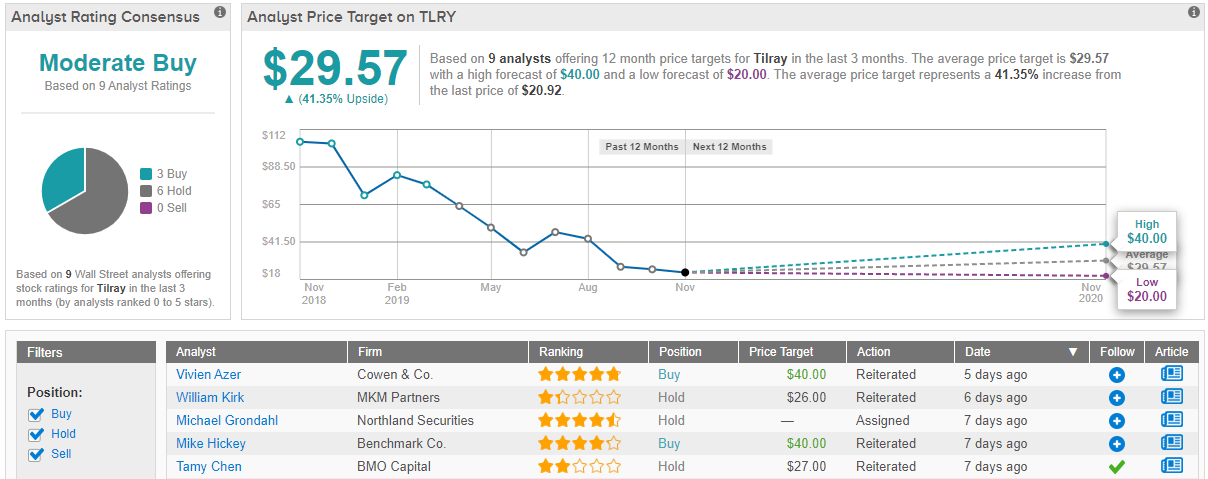

Tilray (TLRY)

Tilray is the wild card of the group. The company has long pointed towards Cannabis 2.0 via specifically a JV partnership with Anheuser-Busch InBev and their Fluent Beverage Company as a major catalyst for the stock.

Due to the insane prices following the IPO where the stock surged over $300, the market is likely more bearish on the stock due to the negativity surrounding the large losses. Similar to Cronos Group, Tilray saw substantial increases in product sold without much of a revenue benefit.

Kilogram equivalents sold in Q3 increased six-fold to 10,848 kg. Unfortunately, the average net selling price per gram collapsed to $3.25, down from $6.21 in the prior year period. The end result was a weak gross margin of 31% and the surging adjusted EBITDA loss of $23.5 million.

The recently bought U.S. hemp business saw revenues decline sequentially again leading to the thought process of chasing far too many markets leading to under performance in the sector. The company ended the year with only $122 million in cash while burning substantial cash from operations.

Tilray appears well positioned with High Park to release a board-based portfolio of cannabis products including CBD beverages, edibles and vape products to tackle the Cannabis 2.0 market. The combination with the InBev JV positions Tilray for catalysts in 2020.

The issue is the valuation is actually still far off base. The stock is still worth $2.0 billion and 2020 revenue estimates are only at $316 million. Tilray reported Q3 revenues of $51 million so the market isn’t exactly forecasting substantial growth going forward, especially considering the large EBITDA losses need more revenues to elimiate.

Overall, TLRY has drawn optimism mixed with caution when it comes to consensus opinion among sell-side analysts. Out of 9 analysts polled in the last 3 months, 3 are bullish on the stock, while 6 remain sidelined. Importantly, with a potential upside of over 40%, the stock’s consensus target price stands at $29.57. This suggests that by consensus expectations, for now, the bulls win on Tilray. (See Tilray stock analysis on TipRanks)