Uber Technologies posted a lower-than-expected loss in the fourth quarter, as the ride-hailing company’s demand for its delivery services continues to reflect three-digit growth. Shares declined 4.8% in Wednesday’s extended trading session after closing 6.1% higher on the day.

Against this, Uber’s (UBER) core ride-hailing business still grapples with pandemic-led restrictions and many employees continuing to work from home. The company incurred a non-adjusted loss of $0.54 per share in 4Q, compared with the $0.55 loss per share estimated by analysts. Total sales generated in the quarter amounted to $3.17 billion, falling short of analysts’ expectations of $3.58 billion.

Meanwhile, net revenue at Uber’s delivery unit, including Uber Eats, surged 224% year-over-year to $1.36 billion. The company reported an adjusted EBITDA loss of $454 million, down from the $615 million loss posted in the same quarter last year.

Delivery gross bookings exploded 130% in the reported quarter, while mobility gross bookings, including rides, plunged 50% during the same period. (See UBER stock analysis on TipRanks)

“While 2020 certainly tested our resilience, it also dramatically accelerated our capabilities in local commerce, with our Delivery business more than doubling over the year to a nearly $44 billion annual bookings run-rate in December,” said Uber CEO Dara Khosrowshahi. “With two global businesses stitched together by world-class tech and increasingly valuable membership programs, we are more focused than ever on making people’s lives a little bit easier—helping them go wherever they want and get whatever they need,” he added.

Furthermore, Uber CFO Nelson Chai confirmed that the company remains on track to achieve its profitability goals in 2021.

Last week, the company announced the acquisition of alcohol delivery start-up Drizly for $1.1 billion. On closing of the transaction, Drizly will operate as a wholly-owned subsidiary of Uber and its marketplace will be integrated with the Uber Eats app. The deal is expected to close by the first half of 2021.

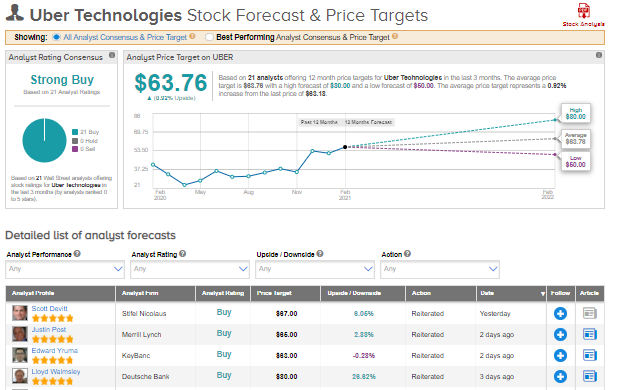

Following the earnings results, Wedbush analyst Daniel Ives reiterated a Buy rating and a price target of $60 (5% downside potential) on the stock.

Ives commented, “Uber’s 4Q results and profitability trajectory for 2021” seems “another major step in the right direction for Dara & Co. The company is clearly seeing a rebound in ridesharing metrics and coupled with a leaner expense structure is setting a stage for snapback in growth and profitability heading towards the end of 2021 and into 2022.”

The analyst believes that the, “the food delivery business around Uber Eats is gaining significant scale and scope both organically, as well as via acquisitions (Postmates, Drizzly, Cornershop).”

“This segment is now worth in a base case scenario roughly $15 per share to the stock with Drizly deal another smart strategic move that is moving delivery well beyond restaurants only,” he noted.

Uber shares have exploded 92% in the past six months, while the stock still scores a Strong Buy consensus rating based on 21 unanimous Buys. That’s alongside an average analyst price target of $63.76, which implies that shares are almost fully valued at current levels.

Related News:

Global Payments Announces Mixed Results, Strategic Partnership With Google

Peloton’s 2Q Results Top Estimates But Delivery Delays Push Shares Down

Linde’s 1Q Profit Outlook Tops Estimates After 4Q Beat; Shares Gain