Taiwan Semiconductor (NYSE: TSM) gained 5.3% on January 13 to close at $139.19, after the semiconductor contract manufacturing and design company delivered a blowout fourth-quarter results, and introduced its guidance for the first quarter of FY2022, well above the analysts’ expectations.

The quarterly beat was driven by robust demand induced by COVID-19 for the company’s chips, especially its industry-leading 5-nanometer technology amid the growing use of smartphones, laptops, and other gadgets.

Q4 Outperformance

Markedly, adjusted earnings of $1.15 per American Depositary Receipt (ADR) grew 16.4% year-over-year, and beat analysts’ expectations of $1.12 per ADR.

Furthermore, revenues jumped 24.1% year-over-year to $15.74 billion and exceeded consensus estimates of $15.67 billion.

The increase in revenues reflects a surge in shipments of 5-nanometer technology, which accounted for 23% of total wafer revenue. In addition, advanced technologies, which include 7-nanometer and more advanced technologies, accounted for 50% of total wafer revenue.

During the quarter, the company reported an impressive gross margin of 52.7%, while operating margin came in at 41.7%, and net profit margin was 37.9%.

Impressive Q1 & FY2022 Outlook

Based on robust Q4 results and current business outlook, management issued the financial guidance for the first quarter and full year of 2022. The company now forecasts revenues to be in the range of $16.6 billion to $17.2 billion, significantly higher than the consensus estimate of $15.84 billion.

Furthermore, gross profit margins are expected to be in the range of 53% and 55%, while the operating profit margins are expected to be between 42% and 44%.

For the full-year 2022, revenue growth is projected to be in the mid-to-high-20% range.

Notably, management plans to make capital spending of $40 billion to $44 billion in FY2022, much higher than the $30 billion spent in FY2021 as it plans to incrementally invest in new technologies.

Management Weighs In

Looking ahead, TSM CFO, Wendell Huang, commented, “Moving into first quarter 2022, we expect our business to be supported by HPC-related demand, continued recovery in the automotive segment, and a milder smartphone seasonality than in recent years.”

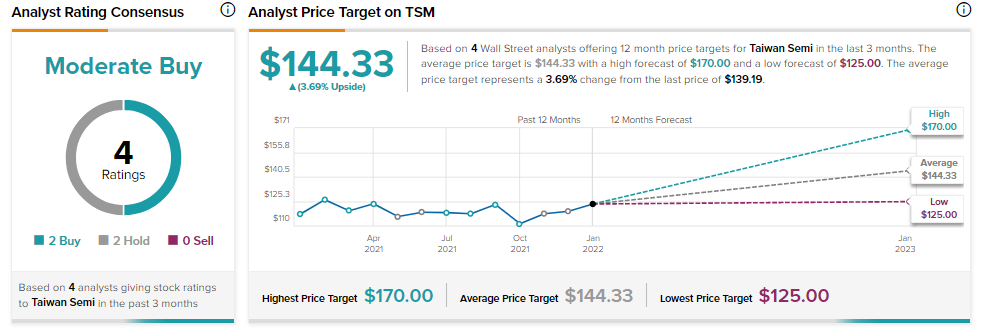

Wall Street’s Take

Following the robust Q4 results, one of the Top Analysts from Needham & Company, Charles Shi increased the price target on Taiwan Semiconductor to $152 (to NT$760.00 from NT$690.00) and reiterated a Buy rating.

Sharing views on the strong outlook, Shi commented, “We calculate the strong outlook suggests pricing increase will contribute at least ~15 pts to overall revenue growth (vs. 8 pts in our previous model), or more than half of TSMC’s projected 2022 increase. The large anticipate price increase, in our view, reflects that the cycle is likely stronger for longer.”

Overall, the stock has a Moderate Buy consensus rating based on 2 Buys and 2 Holds. The average Taiwan Semiconductor price target of $144.33 implies 3.7% upside potential from current levels.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

Jefferies Tank 9.3% as Revenues Disappoint

Koninklijke Philips Shares Plunge 14.7% on Profit Warnings

Paragon 28 Acquires Disior Oy; Shares Down 3.6%