Petco Health and Wellness Company (WOOF) beat analysts’ expectations in fiscal Q1 (ended May 1) driven by record sales and a rise in the number of new customers.

The U.S. pet retailer posted Q1 adjusted earnings of $0.17 per share and beat Street estimates of $0.09. A loss of $0.07 per share was reported in the same quarter last year.

Net sales jumped 27% year-over-year to $1.41 billion and surpassed analysts’ expectations of $1.27 billion. Comparable sales growth was 28% during the quarter. Additionally, adjusted EBITDA expanded 45% to $125.7 million. (See Petco stock analysis on TipRanks)

Petco CEO Ron Coughlin commented, “We’re attracting new customers and gaining market share in a growing category through our unique end to end health and wellness ecosystem. There are more pets in homes than ever and the 1.2 million net new customers we gained in the quarter is a multi-year high, that provides an annuity for years to come. The category acceleration combined with a strengthening of our customer base give us confidence to raise our full year guidance.”

For Fiscal 2021, the company projects revised adjusted EPS to be in the range of $0.73 to $0.76 per share, versus analysts’ expectations of $0.66. Revenue is expected to land between $5.475 billion and $5.575 billion, versus the consensus estimate of $5.33 billion.

Following the Q1 results, Wells Fargo analyst Zachary Fadem maintained a Buy rating and a price target of $30 (17.8% upside potential) on the stock.

Fadem commented, “All in, Q1 results should add further credibility to the narrative that WOOF has considerably improved its competitive position, the underlying category is strong/stable (despite lingering concerns), and the company’s multi-channel initiatives are resonating. With a +4%/+6% increase in the FY21 sales/EBITDA outlook now in the base, we continue to see a very achievable/beatable model for FY21.”

Consensus among analysts is a Strong Buy based on 3 Buys and 1 Hold. The average analyst price target stands at $29 and implies upside potential of 13.9% to current levels.

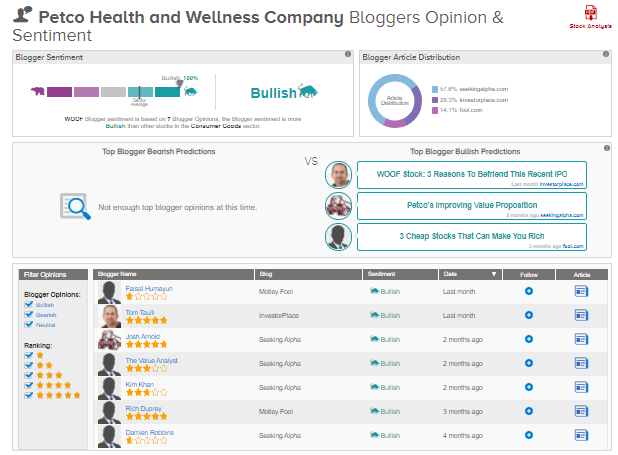

Furthermore, TipRanks data shows that financial blogger opinions are 100% Bullish on WOOF, compared to a sector average of 70%.

Related News:

Cisco’s Q4 Earnings Outlook Miss Estimates After Q3 Beat; Shares Drop After-Hours

Shoe Carnival Posts Quarterly Beat As Sales Improve, Q2 Revenue Outlook Disappoints

Lennox Bumps Up Quarterly Dividend By 19%