Streaming giant Netflix (NFLX) pulled back 9% in Thursday’s after-hours trading, after the company’s second quarter earnings results disappointed investors. Specifically, Q2GAAP EPS of $1.59 missed Street expectations by $0.22.

Looking forward to Q3, Netflix guided for streaming paid memberships of 195.45M, representing a 23.4% climb from the year-ago period. That was alongside guidance for 2.5M net additions for the upcoming quarter- which fell far short of the expected 5 million new net additions.

However revenue of $6.15B surged 25% year-over-year, and beat consensus expectations by $70M. Plus NFLX reported net subscriber additions of 10.09M to 192.95M, easily beating the consensus expectation of 7.5M.

Net income came in at $720M, versus the $271M recorded last year, while operating income was reported at $1.36B on a 22.1% margin- again significantly higher than last year’s $706M and 14.3% margin.

As for Netflix’s upcoming content slate, Chief Content Officer Ted Sarandos- who has now been appointed co-CEO- commented that, “outside of North America, parts of India and Brazil, we’re running pretty much in normal fashion in terms of volume around the world … and we’ve got a couple of shooting days in Los Angeles this week … that’s coming back around.”

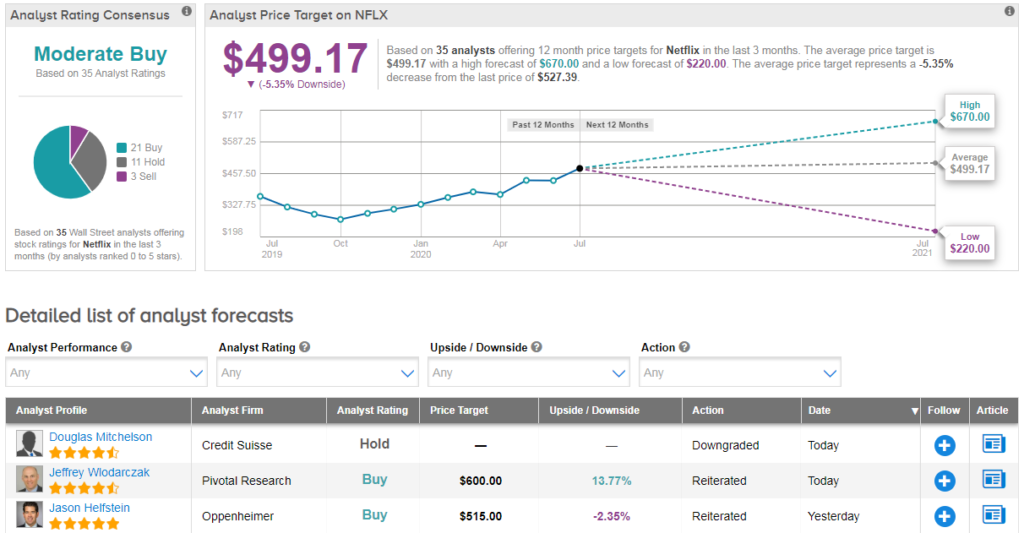

Post-print Oppenheimer analyst Jason Helfstein reiterated his Netflix buy rating while ramping up the price target from $480 to $515. “We believe the current environment continues to favor NFLX’s global production capabilities and extensive content library vs. competitors” he told investors.

“2Q results pointed to a further subscriber pull forward from COVID-19, with 1H:20 net adds of 26M nearly eclipsing FY19 net adds of 28M” the analyst added, although he warned that new subscribers typically churn at a higher rate.

Indeed, on the question of churn CFO Spencer Neumann says new members “look very much like our pre-existing members … they’re coming in from everywhere in the world … they’re highly engaged; retention across every cohort is as good or better than pre-COVID.”

And co-CEO Reed Hastings told analysts on the earnings call “I think of it as, when someone churns, it’s always temporary. They’re gonna come back. It’s just a matter of timing as our service gets better, as maybe their income gets better, as the Internet gets faster.”

Shares in Netflix have now surged 63% year-to-date and analysts have a cautiously optimistic Moderate Buy stock consensus. Due to the recent rally, the average analyst price target indicates 5% downside from current levels.

Speaking from the sidelines, Rosenblatt Securities’ Bernie McTernan stated: “Given our expectation of decelerating revenue growth we continue to believe these valuation levels are difficult to justify.”

NFLX’s dominant position as a global streaming player is not in question, says McTernan, “but we are cautious NFLX may have pulled forward to the less steep part of the S-curve.” He reduced his price target from $440 to $400 on July 16. (See Netflix stock analysis on TipRanks).

Related News:

Google Shifts Business Apps To Accommodate Stay-At-Home Workforce

Guns, Gaming and Zoom – The Companies with the Highest Earnings Momentum Heading into Q2 Reports

Zoom (ZM) Is a Winner, but the Stock Is Fairly Valued Here