Popular ‘athleisure’ retailer Lululemon (LULU) is gearing up to report its earnings results this Thursday, and ahead of this key date analysts are busy ramping up their price targets and reiterating their bullish calls.

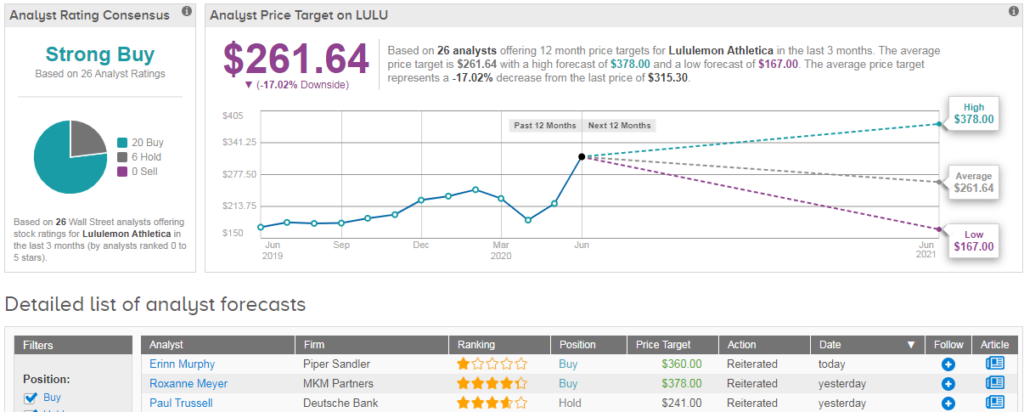

Shares in LULU are currently trading up 36% year-to-date, which means that RBC Capital’s new $360 price target indicates upside potential of 14%. RBC analyst Kate Fitzsimons bumped up her price target from $225 previously, citing updated productivity assumptions and earnings snapback into 2021/22E.

“We expect investors to look past 1Q numbers and focus on commentary on digital momentum, productivity in reopened stores/regions including China, and longer-term growth rate opportunities on the other side of COVID-19” she told investors on June 9.

Indeed, the analyst views any pullback post-print as a buying opportunity, as “LULU is poised for long-term tailwinds on the other side of COVID-19, given its sweetspot of innovation, loyalty, and casual/athletic focused assortments.”

Fitzsimons expects slightly better results than peers given brand heat, favorable category exposure, and expected strong digital demand. Specifically, she is forecasting revenues down (15%) to $668MM and EPS of $0.03 vs consensus of $683MM/$0.23.

For 2Q, she is modelling $770MM in revenues and EPS of $0.14 vs. consensus of $809MM and $0.54, with 2020E EPS of $3.55 (Street $4.34) assuming 9%/15% comps in 3Q/4Q.

Similarly Piper Sandler’s Erinn Murphy sees LULU hitting $360 vs $265 previously. She also reiterated her buy rating, telling investors that she is anticipating strong results especially on the top line thanks to the company’s “robust” digital platform, and activity-based orientation.

Encouragingly, MKM Partners analyst Roxanne Meyer has revealed that her checks “point to a blockbuster quarter online.” She has a buy rating on the stock and took her price target to a Street-high $378 from $230 on June 8.

“Highly bullish” survey work has convinced the analyst that LULU will “recover quickly and strongly and is well positioned longer-term.” With “the national launch of the loyalty program, accelerating new customer growth, and a favorable impact on margins from e-commerce”, Lululemon is “about the marathon, not the sprint” she concluded.

Taking a more cautious approach, Deutsche Bank analyst Paul Trussell boosted his LULU price target to $241 from $197 on June 8 but maintained his Hold rating. He cited the “longer than originally anticipated” store closings during the lockdown period, but added that his sales growth expectations for post-shutdown have now “increased significantly.”

Overall, LULU sports a bullish Strong Buy Street consensus, with 20 recent buy ratings vs 6 hold ratings. Meanwhile the average analyst price target stands at $262 (17% downside potential). (See LULU stock analysis on TipRanks)

Related News:

Macy’s Spikes 15% After-Hours On New Financing Deal

Syracuse Is Said To Be In Talks To Buy Bankrupt J.C. Penney; Shares Leap 55%

Buckle Down Says Street, As Stitch Fix Sinks 7% Post-Print