IBM (IBM) has decided to shutter its facial recognition business, with new CEO Arvind Krishna criticizing the technology for enabling racial and gender bias.

“IBM firmly opposes and will not condone uses of any technology, including facial recognition technology offered by other vendors, for mass surveillance, racial profiling, violations of basic human rights and freedoms, or any purpose which is not consistent with our values and Principles of Trust and Transparency,” Krishna told Congress on Monday.

“We believe now is the time to begin a national dialogue on whether and how facial recognition technology should be employed by domestic law enforcement agencies” he added.

According to a person familiar with the situation, IBM’s facial recognition business did not generate significant revenue, reports CNBC. However the move is nonetheless a bold one- especially as the US government is one of IBM’s key customers.

“Vendors and users of Al systems have a shared responsibility to ensure that Al is tested for bias, particularly when used in law enforcement, and that such bias testing is audited and reported,” Krishna stated in his letter to Congress.

Back in May only 2.4% of Amazon (AMZN) shareholders voted in favor of a proposal to stop the e-commerce giant selling its facial recognition technology to government agencies.

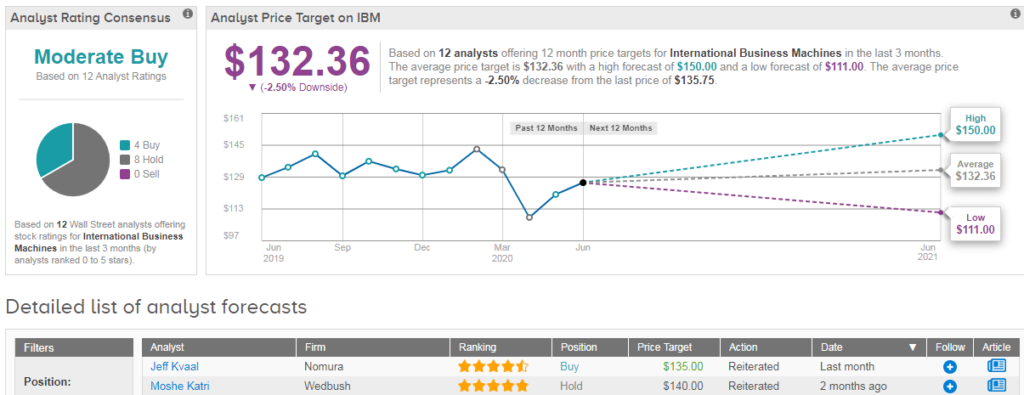

Shares in IBM are trading marginally up on a year-to-date basis, and analysts have a cautious Moderate Buy consensus on the stock with 4 buy ratings and 8 holds. The average analyst price target stands at $132, indicating downside potential of 2.5% from current levels. (See IBM stock analysis on TipRanks).

Despite near-term dislocations, Bank of America’s Wamsi Mohan sees several reasons to like IBM in the long term including the appointment of new CEO Arvind Krishna which he says sets the stage for new strategy, investments and priorities.

Restructuring and running GTS for profitability already underway and likely to be upsized and accelerated, says Mohan, while low SMB (small and medium business) exposure plays favorably to navigate weaker demand. He has a buy rating on the stock and $145 price target.

Related News:

NetEase Sets Global Offering Pricing, Hong Kong Listing For June 11

Zoom (ZM) Is a Winner, but the Stock Is Fairly Valued Here

Google Maps To Roll Out Covid-19 Alerts On Travel Restrictions