Domino’s Pizza (DPZ), the largest pizza company in the world based on retail sales, has provided an encouraging business update- revealing a material increase in US same store sales (SSS) since its Q1 earnings on April 23. Shares are rising 2% in Wednesday’s pre-market trading, and are now trading up 23% year-to-date.

Specifically, US SSS came in at +20.9% from mid-April through mid-May, up +7.1% from mid-March through mid-April as consumer habits increasingly shifted to trusted delivery/carry-out brands. For 2Q to date, comps are now +14%, well ahead of the Street’s +6.8% estimate for the full quarter.

Meanwhile international SSS were +3.3% from mid-April through mid-May. Despite choppiness this still represents a strong acceleration from the -1.1% in the first four weeks of the quarter. Quarter-to-date trends are now +1%, much better than consensus’ -3.2% estimate.

Ritch Allison, Domino’s CEO, commented: “Our U.S. sales results accelerated materially over weeks five through eight of the second quarter when compared to weeks one through four.”

He continued: “We are seeing a tailwind as consumer behavior across the restaurant industry has shifted toward delivery and carryout, though we are not sure whether this trend will continue for the remainder of the second quarter or how long this tailwind may last.”

However, Allison also told investors that international sales results continue to be choppy – and may be for the foreseeable future. In some markets, sales results are matching or exceeding those in the US- but in others, where “master franchisees are still experiencing significant operating limitations or temporary store closures, those sales are down materially versus last year” he said.

Indeed, at its peak, DPZ had approximately 2,400 temporary store closures due to the coronavirus pandemic. And while master franchisees continue to reopen stores, Allison expects that temporary closures, partial openings hours and limited service methods will continue to pressure international same-store and retail sales in the near-term.

DPZ cited the “dynamic situation related to the COVID-19 pandemic” as behind its decision to release this information before its July 16 earnings date- but added that going forward it will now return to normal quarterly reporting.

Following the update, Oppenheimer’s Brian Bittner reiterated his buy rating and $405 price target. “The strength in the overall business reinforces the best-in-class unit opening story which drives DPZ’s strong growth algorithm” he cheered, adding “We raise sales and earnings estimates through ’21E.”

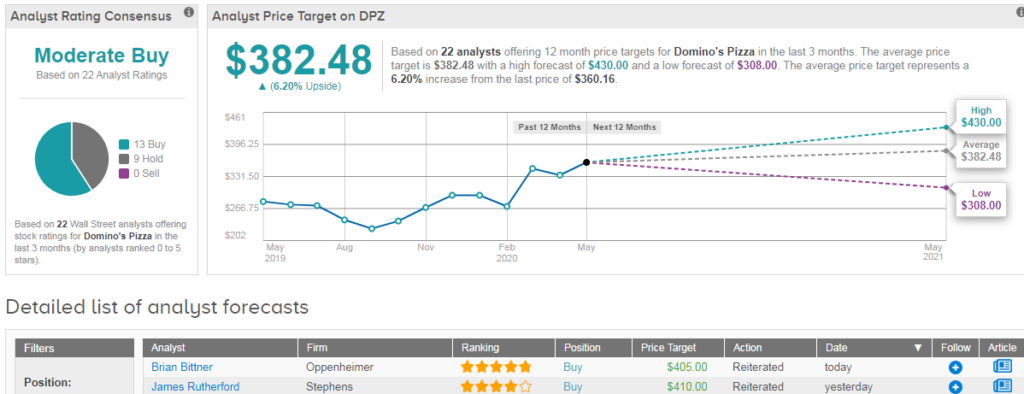

Bittner’s ’20E/’21E EPS now moves to $11.25/$12.20 from $10.98/$11.92, and includes the recent $100M debt paydown. “We continue to assume 3% unit growth this year, with a return to more normalized 7% growth in ’21E” he says. Overall, analysts have a cautiously optimistic Moderate Buy consensus on DPZ with an average analyst price target of $382 (6% upside potential).(See DPZ stock analysis).

Related News:

‘Holy Cow’ Exclaims Analyst On Tractor Supply’s Record Guidance; Shares Surge 9%

Six Flags Set to Partially Reopen in June, Stock Jumps on News

Uber In Partnership With MoneyGram For Driver Discount During Pandemic