Shares of Wix.com rose 6% in Wednesday’s pre-market trading session after the cloud-based website development platform provider reported a lower-than-feared loss in the fourth quarter.

Wix (WIX) posted a non-GAAP net loss per share of $0.03 during the fourth quarter, which came in ahead of the $0.11 net loss expected by analysts. Revenue increased 38% year-on-year to $283 million topping analysts’ estimates of $270.22 million.

In 2020, the company added about 1 million net new subscriptions and crossed $1 billion in annual collections.

Wix CEO Avishai Abrahami said, “At this growth rate, in the next 5-7 years, 50% of anything new built on the internet will be done on Wix.”

Lior Shemesh, CFO of Wix commented, “We are investing heavily in business and new products, most notably Wix Payments as online commerce businesses continue to come to Wix.”

During fiscal 2020, Wix generated sales of $988.8 million, up from the $761.1 million in the year-ago period. Revenue was driven by 22% growth in creative subscriptions revenue and 76% growth in business solutions revenue. Th company posted a non-GAAP net loss per share of $0.44 versus non-GAAP net income per share of $1.17 in the year-ago period.

Wix’s gross margin decreased from 74% in 2019 to 68% in 2020 due to incremental investments in customer care, hosting and growth at its business solutions segment. (See Wix stock analysis on TipRanks)

Looking ahead to 1Q, the company estimates revenue to generate between $291 million to $296 million and fiscal 2021 revenue to be in the range of $1.27 billion to $1.29 billion. This outlook reflects expectations of an increase in collections growth, stronger partners activity on Wix and the launch of new products.

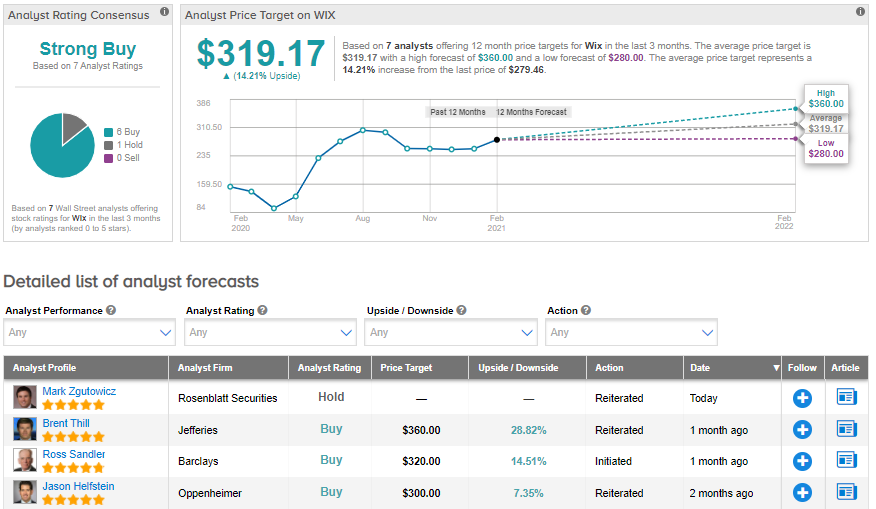

Following the earnings results, Rosenblatt Securities analyst Mark Zgutowicz reiterated a Hold rating on the stock with a price target of $270 (3.4% downside potential).

Zgutowicz noted, “A closer look at 4Q and 2021 guided collections and revenue suggests growth driven by lower margin Business Solutions while higher-margin Creative Subscriptions has peaked. Additionally, the guidance implies both segments’ gross margins will further deteriorate in 2021”.

The rest of the Street has a Strong Buy consensus rating on the stock. That’s based on 6 Buys and 1 Hold. The average analyst price target of $319.17 implies about 14% upside from current levels. Thats after the stock surged about 89% over the past year.

Related News:

Kar Auction Services Tanks 16% After Posting Quarterly Loss

Cornerstone Pops 16% After-Hours As Quarterly Earnings Blow Past Analysts’ Estimates

ACI Teams Up With Auriga For Self-Service Banking Platform; Street Says Buy