Amgen (AMGN) is a global biopharmaceutical company based in California. It is a member of the Dow Jones index. The company develops treatments for various diseases, including cancers and cardiovascular conditions.

For Q3 2021, Amgen reported a 4% year-over-year increase in revenue to $6.7 billion, exceeding the consensus estimate of $6.69 billion. It posted adjusted EPS of $4.67 versus $4.19 in the same quarter last year and beat the consensus estimate of $4.26.

The FDA recently approved Amgen’s Otezla drug as a treatment for plaque psoriasis in adult patients. About 8 million people in the U.S. suffer from plaque psoriasis and Otezla can be used at all severity levels of the disease. Amgen has also secured FDA approval of its Tezspire drug for the treatment of severe asthma in adults and children over 12 years of age. Tezspire is the product of a collaboration between Amgen and AstraZeneca (AZN). 34 million people live with asthma globally.

Amgen ended Q3 with $2.9 billion remaining under its share repurchase program after buying back $1.1 billion during the quarter. It has recently boosted the program with an additional $4.5 billion. The company finished Q3 with $12 billion in cash. It plans to distribute a quarterly dividend of $1.94 per share on March 8 and has set February 15 as the ex-dividend date.

With this in mind, we used TipRanks to take a look at the newly added risk factors for Amgen.

Risk Factors

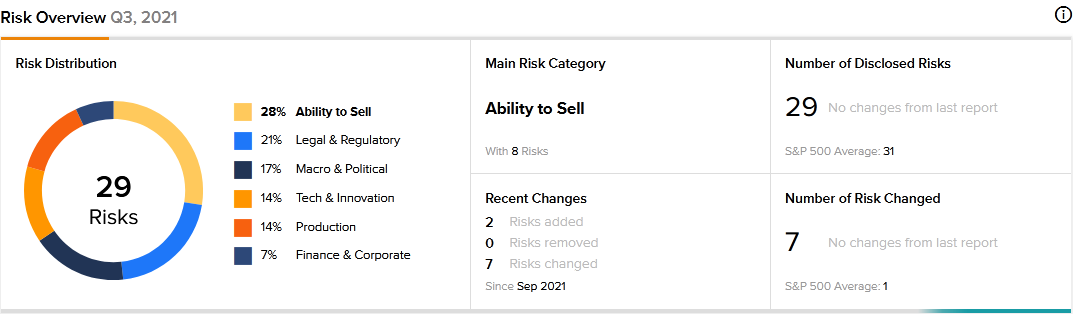

According to the new TipRanks Risk Factors tool, Amgen’s main risk category is Ability to Sell, representing 28% of the total 29 risks identified for the stock. Legal and Regulatory and Macro and Political are the next two major risk categories, accounting for 21% and 17% of the total risks, respectively. The company recently updated its profile with two new risk factors.

Amgen informs investors that Congress and the White House are seeking multiple drug pricing reforms that could adversely affect the sale of its products. It mentions that the Build Back Better bill has incorporated proposals from a drug-pricing bill called H.R. 3. It cautions that the proposals include a penalty against drug manufacturers for failing to reach agreements with the government on negotiated drug prices.

Amgen further says that the federal government wants to allow the import of certain drugs from Canada, including a version of its Otezla drug. It cautions that allowing such imports could have a material adverse impact on its business.

Amgen tells investors that while the COVID-19 pandemic persists, efforts to contain the disease may continue to adversely affect its product development, clinical trials, manufacturing, and sales activities.

The Ability to Sell risk factor’s sector average is 9%, compared to Amgen’s 28%. Amgen’s shares have declined about 4% since the beginning of 2021.

Analysts’ Take

Leerink Partners analyst Geoff Porges recently reiterated a Hold rating on Amgen stock without assigning it a price target.

Consensus among analysts is a Hold based on 4 Buys, 10 Holds, and 1 Sell. The average Amgen price target of $229.31 implies 4.24% upside potential to current levels.

Related News:

Carnival Books Wider-than-Expected Q4 Loss; Shares Rose

BlackBerry Q3 Earnings Preview: What to Expect

CIBC Invests C$100M to Stimulate Climate Innovations