Auto technology supplier Veoneer on Thursday announced a cooperation with Qualcomm Technologies to develop a software platform for its advanced driver assistance systems (ADAS), sending shares up 17% in early market trading.

The stock surged to $12.84 in Thursday’s morning trading. The two companies have signed a non-binding letter of intent and expect to finalize a definitive agreement during the second half of 2020.

Under the terms of the collaboration, Veoneer (VNE) will develop an integrated software platform with Qualcomm tailored to address the growing complexities associated with developing ADAS, including safety compliance, which require highly advanced and power-efficient compute, connectivity and cloud service capabilities across all vehicle tiers. The companies expect the integrated platform to be available through automotive Tier-1 suppliers or directly to manufacturers for 2024 vehicle production.

“We are pleased to work with Qualcomm Technologies to develop next generation solutions for ADAS and collaborative and autonomous driving,” said Veoneer CEO Jan Carlson. “Working with a recognized leader like Qualcomm, using their ground-breaking Snapdragon Ride products, provides us the remaining piece of the puzzle.”

The platform will integrate Veoneer’s 5th generation perception software and driving policy software with the current and future Snapdragon Ride portfolio. Qualcomm (QCOM) intends to make the integrated SoC (System on a Chip) and software stack platform available to global automakers and Tier-1 suppliers.

Veoneer will serve as a Tier-1 system integrator for the new solution, while continuing its current strategies, which include developing, selling and launching its full line of ADAS and collaborative driving products and systems.

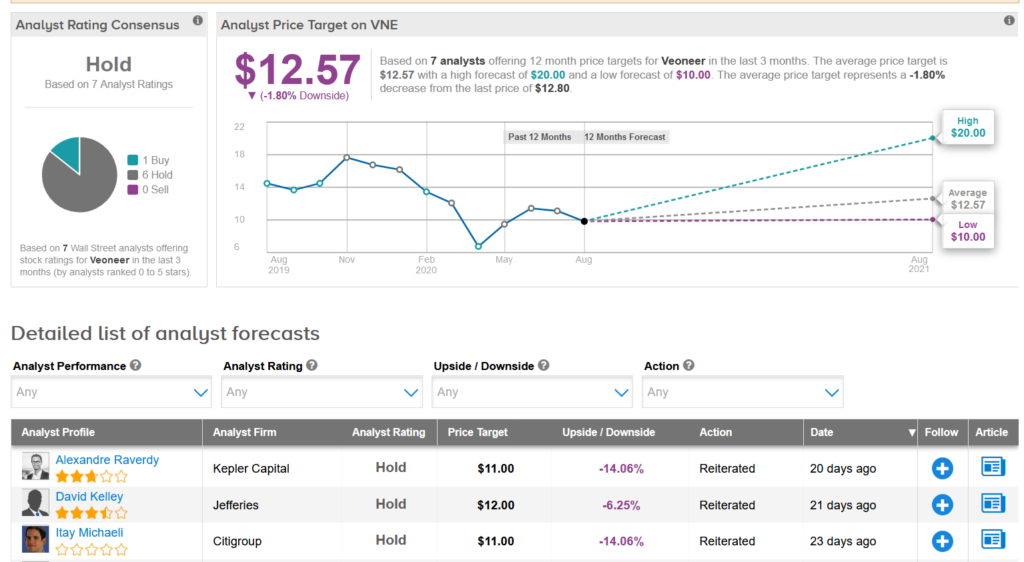

With Veoneer shares down 30% so far this year, the $12.57 average analyst price target implies 1.8% downside potential over the coming year.

Mizuho Securities analyst Vijay Rakesh said last month that despite near-term challenges he is maintaining a Buy rating on the stock with a $20 price target, citing the company’s good order book and improved balance sheet.

“While we believe VNE is doing a good job driving operating leverage, the key will be driving further leverage into 2021E to reduce cash burn,” Rakesh wrote in a note to investors. “We believe the 2H20-21 LVP [light vehicle production] outlook can improve with a continuing strong order intake despite a tough LVP landscape.”

The rest of the Street is sidelined on the stock. The Hold analyst consensus breaks down into 6 Holds versus Rakesh’s Buy rating. (See VNE stock analysis on TipRanks)

Related News:

Splunk Slips In Pre-Market As Revenue Outlook Disappoints; Street Stays Bullish

NetApp Leaps 11% In After-Hours On Strong 1Q Results

Nordstrom Drops 5% On Larger Quarterly Loss As Analyst Says Stock Valued