Starbucks Corp. (SBUX) said it expects to post a loss in the third quarter after losing as much as $3.2 billion in revenue due to the impact of the coronavirus pandemic, while also planning store closures in the U.S. and Canada.

The stock dropped 4% on Wednesday to close at $79.08 after the coffee chain operator provided an annual financial outlook and updated quarterly estimates.

Starbucks expects to post an adjusted loss of $0.55 to $0.70 per share in the third fiscal quarter ending in June, according to preliminary figures. Operating income is estimated to decline by as much as $2.2 billion, representing a flowthrough rate of about 65% to 70% on lost sales.

The coffee chain sees adjusted EPS improve sequentially in Q4 fiscal 2020, which it forecasts to be in a range of about $0.15 to $0.40. Full-year expectations for adjusted EPS are estimated to be in a range of $0.55 to $0.95 for fiscal 2020.

Over the next 18 months, Starbucks plans to close about 400 stores in the Americas and slash the number of its 600 planned new store openings to about 300 this fiscal year. In Canada, the company may close up to 200 stores over the next two years.

On a geographic breakdown, Starbucks expects U.S. comparable store sales in fiscal 2020 to drop 40% to 45% in Q3, and then improve to a decline of 10% to 20% in Q4, yielding a retreat of 10% to 20% for the full fiscal year.

U.S. company-operated stores began to re-open in the second week of May, with about 50% open at the end of April and 91% open at the end of May.

In China, Starbucks said that the recovery, which started in late February, has continued into the third fiscal quarter, with comparable store sales down 21% versus the prior year in May, and down 32% in April. With 99% of stores in China open, comparable store sales retreated by about 14% in the final week of May compared to the prior year. The number of Starbucks stores in China has surpassed 4,400 and the company said that it is on track to add at least 500 new stores this fiscal year.

“With the progress we have seen to date in China, we continue to believe that comparable store sales will substantially recover by the end of the fourth fiscal quarter,” the company said in a letter to shareholders.

China’s comparable sales are expected to improve to a decline of 20% to 25% in Q3, and trend towards roughly flat by the end of Q4, yielding a decline of 10% to 20% for the full fiscal year.

Despite a share surge of 40% since hitting a low in March, Starbucks is still down over 10% year-to-date.

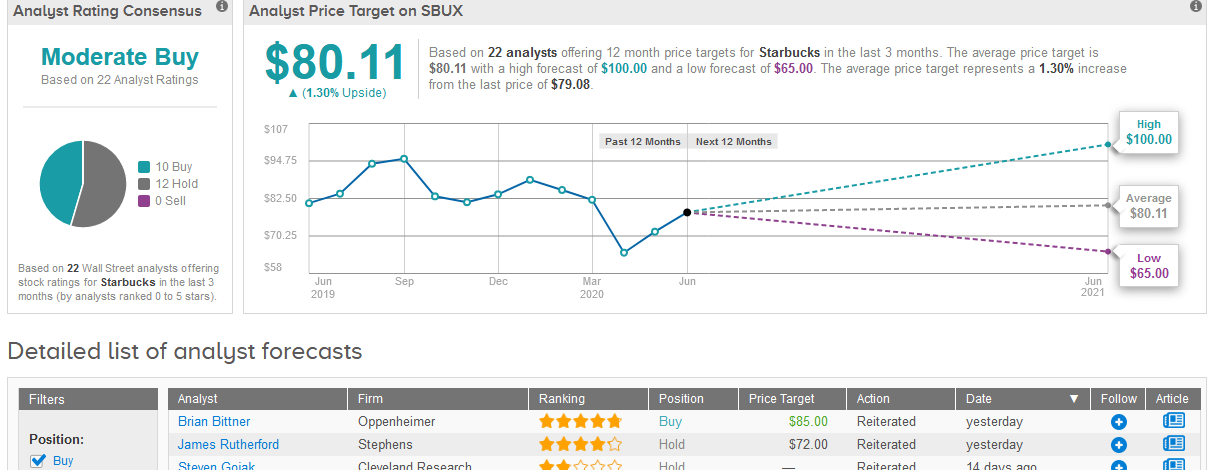

Commenting on the financial update, five-star analyst Brian Bittner at Oppenheimer says he remains more cautious in the near term as sales trends are significantly disrupted by the virus. However, in the longer-term he believes that the brand and the company are “well-positioned to weather this storm”.

Therefore, Bittner maintains a Buy rating on the stock with a $85 price target.

“Overall, the recovery remains choppy and the update aligns with our view that the path in the US to a fully restored annualized unit value (AUV) setting remains challenging,” Bittner wrote in a note to investors. “This could keep the stock range-bound in the near term, and we would look at a pullback toward $70/sh to become more aggressive with our Outperform.”

In addition, Bittner lowered his earnings estimates through F21 to EPS of $2.57 versus the Street’s $2.73.

Meanwhile, the rest of the Wall Street community is cautiously optimistic on the stock. Recent reviews by 22 analysts show 12 Hold versus 10 Buy ratings adding up to a Moderate Buy consensus. The $80.11 average price target reflects analysts’ view that shares are almost fully priced. (See Starbucks stock analysis on TipRanks).

Related News:

Dunkin’ Franchisees To Hire 25,000 Workers As U.S. States Reopen; Keybanc Raises Stock To Buy

Starbucks Back To Business In Japan

Beyond Meat Teams Up With KFC, Pizza Hut In China