Shares of Rexnord Corp. rose almost 4% in Tuesday’s pre-market trading after the water management solutions provider reported better-than-estimated quarterly results.

Rexnord (RXN) posted adjusted earnings per share (EPS) of $0.39 during the third quarter, which came in ahead of the $0.38 expected by analysts. Revenue decreased 0.4% year-on-year to $490 million, but topped analysts’ estimates of $449 million.

For calendar year 2020, the company generated sales of $1.98 billion, down from the $2.06 billion posted in the year-ago period. Adjusted earnings per share came in at $1.77, down from the $1.98 in the comparable year-ago period. Annual free cash flow increased 13% to $276 million year-on-year.

Sales in Rexnord’s aerospace end markets declined 36% decline year-on-year. The company expects an improvement in order rates in the second half of 2021.

Rexnord’s CEO Todd Adams said, “For 2021, we believe we are positioned for an improvement in sales growth and structural cost reduction initiatives to enable margin expansion.”

Rexnord’s water management platform saw 15% year-on-year sales growth, 5% of which came from its previous acquisitions of Just manufacturing and Hadrian.

Looking ahead to the March quarter, Rexnord sees its water management platform sales increase year-on-year by high single digit rate and its adjusted EBITDA margin to be in the range of 25% and 26%.

For full-year 2021, Rexnord sees sales growth of mid single digit percentage and a modest expansion in margins. (See Rexnord stock analysis on TipRanks)

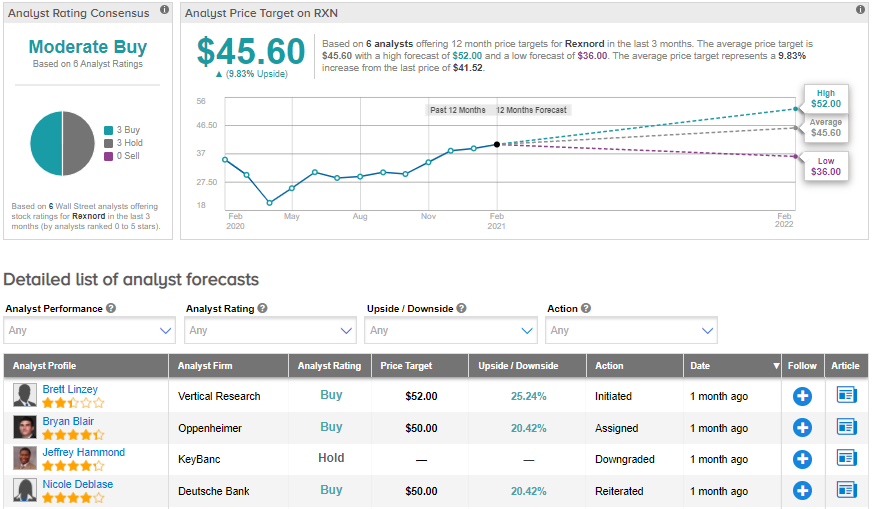

On Jan. 14, Oppenheimer analyst Bryan Blair raised Rexnord’s price target to $50 (20.4% upside potential) from $44 and reiterated a Buy rating, saying that “valuation remains a relative catalyst at current levels.”

“We believe Rexnord has received well-deserved credit over the last three months and has runway for further outperformance,” Blair wrote in a note to investors. “We continue to see upside vs. 2021 expectations, driven by PMC’s early-cycle rebound, WM’s hygienic solutions ramp, and strategic M&A.”

“Equally important, we expect Rexnord can remain a catalyst-rich story

through 2H21 and into 2022,” the analyst added.

The rest of the Street has a Moderate Buy consensus rating on the stock. That’s based on 3 Buys and 3 Holds. The average analyst price target of $45.60 implies 9.8% upside from current levels.

Related News:

Lincoln Electric Posts Better-Than-Expected Quarterly Profit; Street Sees 5% Upside

CAE’s Quarterly Profit Lags Estimates Amid Air Travel Slump

Moody’s Posts Better-Than-Expected 4Q Revenue But Profit Disappoints