Shares of Ontrak were up 8.8% in Wednesday’s pre-market session after the company forecast 2021 revenues that topped the Street’s estimates. Moreover, Ontrak reported better-than-expected results for the fourth quarter.

Ontrak’s (OTRK) 4Q revenues of $29.3 million came in above consensus estimates of $24.6 million and jumped 149% year-over-year.

An adjusted loss of $0.07 per share compared favorably to the year-ago period’s loss of $0.39. Analysts were anticipating a loss of $0.39 per share. The improvement in its bottom line performance reflected higher sales growth and a narrower operating loss in 4Q from the year-ago period.

The company’s CEO, Terren Peizer, said, “While we are extremely disappointed by the upcoming loss of our Ontrak-A contract in June 2021, we are focused on the growth opportunities ahead of us with existing and new customers.” He added, “During the fourth quarter, expanded programs with existing health plans and signed contract renewals with current customers resulted in strong enrollment rates which we expect to see continue through 2021.”

Looking ahead, Ontrak anticipates 2021 revenue of $100 million, higher than consensus estimates of $97.1 million. The company said, “Initially, we were going to guide to 100% growth with revenues of $165 million. In light of Ontrak-A, we believe we are being conservative with our $100 million revenue guidance.” (See Ontrak stock analysis on TipRanks)

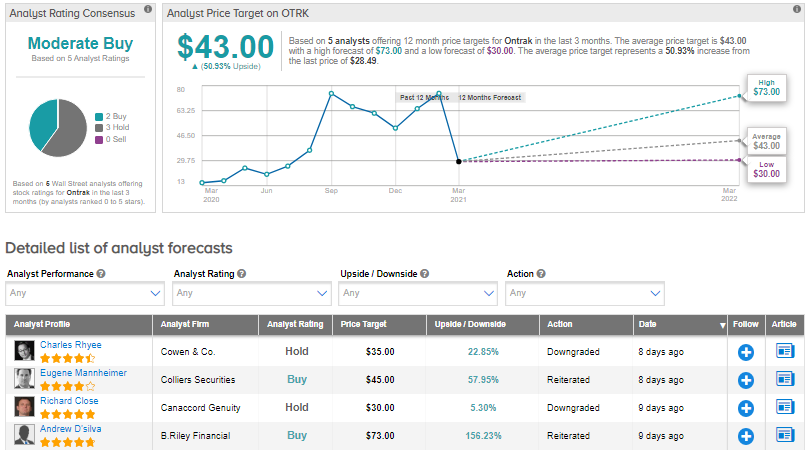

On March 1, Canaccord Genuity analyst Richard Close downgraded the stock to Hold from Buy and lowered the price target to $30 (5.3% upside potential) from $89, “following the impending loss of Aetna, Ontrak’s largest client.”

In a note to investors, the analyst said, “While we don’t see losing Cigna as a short-term risk, customer diversification is desperately needed.” He added, “At this time, we believe that we need to see successful execution in order to justify multiple expansion from current levels.”

Overall, consensus among analysts is a Moderate Buy based on 2 Buys and 3 Holds. The average analyst price target of $43 implies upside potential of about 51% to current levels. Shares have gained around 78% over the past year.

Related News:

Oak Street Slips On Wider-Than-Expected 4Q Loss; Street Sees 29% Upside

Children’s Place 4Q Profit Exceeds Estimates On Strong Digital Sales

Everi Gains Over 3% With 4Q Beat, Despite COVID-19 Headwinds