Mondelez International delivered better-than-expected results for the third quarter driven by elevated demand in developed markets as consumption of candies and cookies remained strong with people spending more time at home amid the pandemic. Shares were down 0.85% in the extended trading session on Monday despite the upbeat results.

Revenue from developed markets increased 9.6% to $4.38 billion while revenue from emerging markets improved sequentially but was still down 3.1% Y/Y to $2.29 billion. Overall Mondelez’s (MDLZ) 3Q revenue grew 4.9% Y/Y to $6.67 billion, surpassing analysts’ estimate of $6.49 billion.

The maker of Oreo and Toblerone chocolate posted adjusted EPS of $0.63, reflecting a 1.6% Y/Y decline but beat analysts’ forecast of $0.62. Earnings declined despite improvement in margins due to “unfavorable taxes.”

Looking at guidance, Mondelez now expects organic net revenue growth of over 3.5% in 2020 and adjusted EPS growth of over 5% on a constant-currency basis. It expects to generate free cash flow of about $3 billion this year. (See MDLZ stock analysis on TipRanks)

On the 3Q conference call, the company indicated that it is planning to resume its share buyback plan in the fourth quarter. It had earlier suspended the program in March to ensure financial flexibility in response to COVID-19.

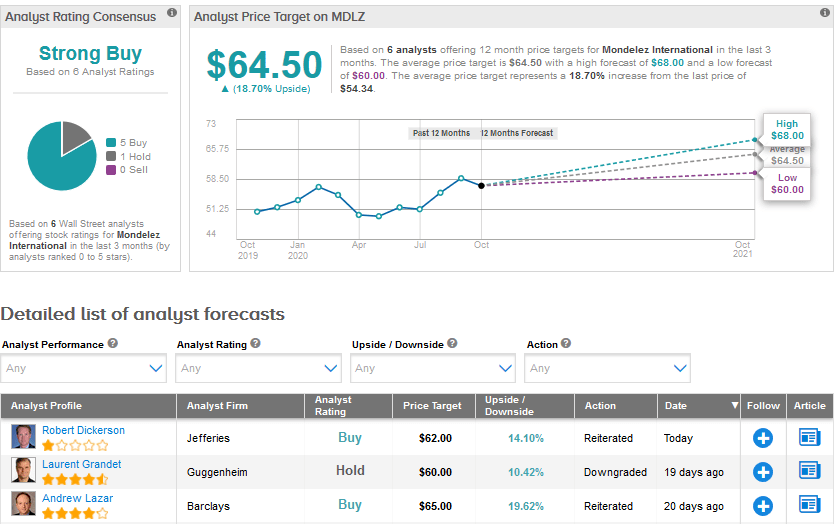

Following the print, Jefferies analyst Robert Dickerson reiterated a Buy rating for Mondelez with a price target of $62 and commented, “Topline growth seems sustainable longer-term given end-market exposure, liquidity and leverage remain healthy, global share trends impressive, and emerging market trends increasingly reassuring, yet valuation is still discounted relative to other larger CPG multinationals. We continue to see 15%+ upside in the stock over the NTM [near-term], as long as the unknowns (COVID, Brexit, and U.S. tax policy) prove to be limited shocks.”

The Street has a Strong Buy analyst consensus for Mondelez based on 5 Buys versus 1 Hold. With shares down 1.3% year-to-date, the average analyst price target of $64.50 suggests an 18.7% upside potential in the months ahead.

Related News:

Clorox Hikes 2021 Guidance Due To Cleaning Bonanza; Shares Rise 4%

Skechers Falls 9% Despite Earnings Beat, Street Stays Bullish

Dunkin’ To Be Taken Private By Inspire Brands In $8.8B Deal