Shares of Mohawk Industries surged 10.9% on Oct. 30 as the company exceeded the Street’s expectations for the third quarter.

The flooring products maker’s 3Q adjusted EPS of $3.26 crushed analysts’ estimate of $2.14 and grew 18.5% year-over-year. Mohawk’s (MHK) revenue of $2.57 billion also came ahead of analysts’ estimate of $2.5 billion. The company attributed the 2.2% revenue growth in its topline to pandemic-induced demand for its products as people are spending more time at home and working remotely, thus driving increased investments in home remodeling.

The company stated that it entered 4Q with improved sales and margin trends and a solid order backlog. It expects residential remodeling and new home construction to remain strong amid the pandemic.

However, Mohawk expects its higher-margin commercial business to continue to be slow, with completed projects likely to outpace new starts. The company also cautioned that business visibility continues to be limited due to many uncertainties. Currently, it predicts 4Q EPS between $2.75 to $2.87. (See MHK stock analysis on TipRanks)

Regarding the previously disclosed subpoenas from the U.S. Department of Justice and the SEC relating to allegations in a class action suit against Mohawk, the company said that its Audit Committee and outside legal counsel completed a thorough investigation and concluded that the allegations are without merit. The lawsuit alleged that the company fabricated its revenues, among other allegations. The company also said that it is cooperating fully with the ongoing governmental investigations and will continue to vigorously defend against the lawsuit.

Following the earnings release, Raymond James analyst Sam Darkatsh noted, “Mohawk’s 3Q results easily surpassed views, with the beat coming “across the board” and via better than expected margins in each reportable segment. The FNA [Flooring North America] segment margins in particular beat Street views by ~170bp – important as this segment’s margins historically correlate well with the stock’s relative performance.”

“Further, regarding the class action lawsuit/SEC/DOJ investigation, Mohawk’s now-changed verbiage (and newly announced $500 million share repurchase authorization) strongly suggest the company’s increasing confidence in its legal positioning,” Darkatsh added.

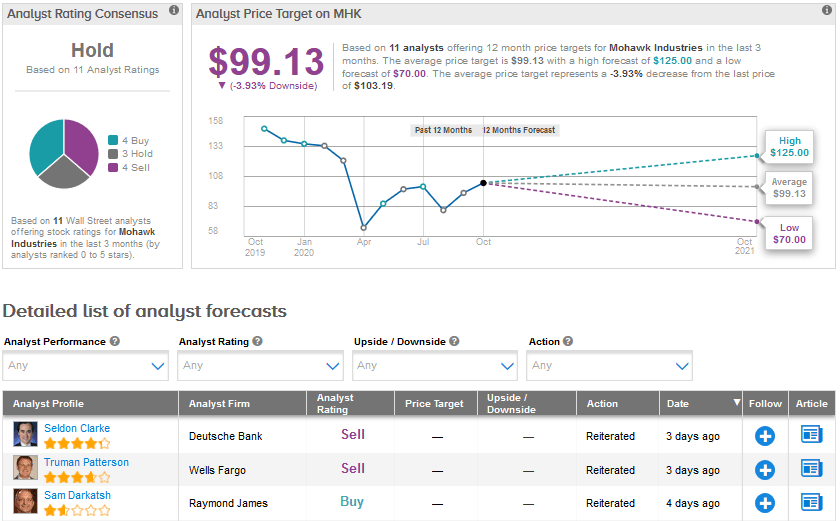

The Street remains sidelined about Mohawk. A Hold analyst consensus is based on 4 Buys, 3 Holds and 4 Sells. The average analyst price target of $99.13 indicates a downside potential of 3.9% from the current levels. Shares are down 24.3% year-to-date.

Related News:

Honeywell’s 3Q Sales Drop 14% As Covid-19 Hurts Aircraft Demand

O’Reilly Bumps Up Share Buyback Plan By $1B After 3Q Profit Beat

Ford Targets Sale Of 100,000 Hands-Free Cars In First Year