Shares in Mohawk Industries (MHK) dropped almost 5% in extended market trading on Monday after the flooring company disclosed that it is being sued for allegedly “fabricating” sales and overproducing products to report higher operating margins, among other violations.

The stock declined to $72.99 in Monday’s after-market trading. According to a SEC filing, an amended class action complaint for violations of federal securities laws was filed against Mohawk and its CEO Jeff Lorberbaum in the Northern District of Georgia on June 29. The complaint alleges that Mohawk fabricated revenues by attempting delivery to customers that were closed and reporting these as sales. It is also claimed that the flooring company overproduced product to report higher operating margins and maintained “significant” inventory that was not salable and that it improperly delivered inventory knowing that it was defective and customers would return it.

“The company intends to vigorously defend itself in the lawsuit,” Mohawk said in the filing.

Furthermore, the company reported that on June 25, it received subpoenas by the U.S. Attorney’s Office for the Northern District of Georgia and the SEC on topics similar to those raised by the amended complaint adding that it is cooperating with those authorities.

Mohawk’s operations have been hit hard by the lockdown mandates during the coronavirus outbreak sending its shares down 49% so far this year.

Commenting on its financial situation, Mohawk said that it is well positioned with a strong balance sheet and limited debt to navigate through the current economic disruption.

“We have recently issued over $1 billion of long-term bonds to strengthen our ability to strategically invest and better position Mohawk for the future,” the company said. “Our operations are improving as countries adapt to Covid-19.”

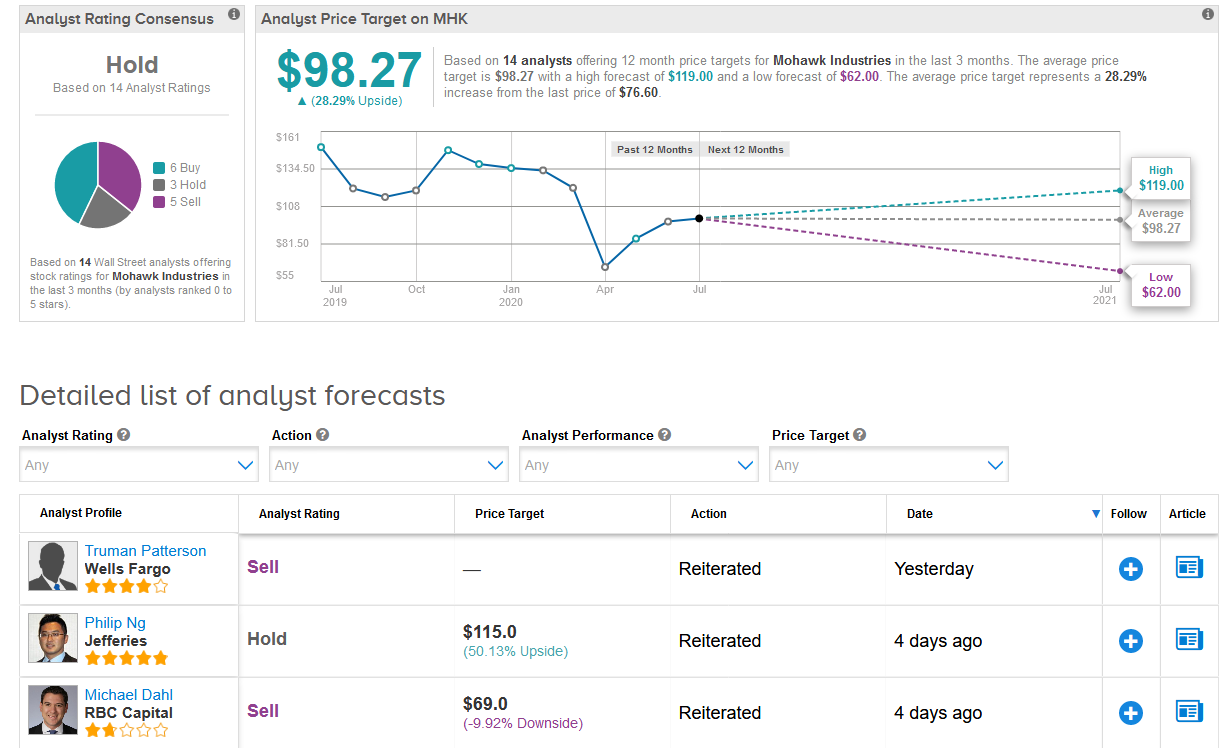

Five-star analyst Philip Ng at Jefferies reiterated a Hold rating on the stock with a $115 price target (50% upside potential), saying that while shares could see short-lived rally relief following “far better than feared” decline in U.S. floor covering sales in Q2, he also could see shares fading given ongoing concerns around the pending litigation.

The rest of the Street is in line with Ng’s sidelined rating outlook. The Hold analyst consensus shows 3 Holds and 5 Sells versus 6 Buys. Meanwhile, the $98.27 average price target suggests shares are poised to advance 28% over the coming year. (See MHK’s stock analysis on TipRanks)

Related News:

Hewlett Packard To Buy Silver Peak For $925M To Boost Cloud Solutions

Google Faces Antitrust Investigation From Its Home State, California

Facebook Files Lawsuits In U.S., Europe Against Abuse On Its Platforms