Lululemon Athletica Inc. (LULU) announced yesterday that it will be acquiring the at-home fitness company Mirror for $500 million. It is the first acquisition for the retail apparel company.

According to Lululemon, the purchase price for Mirror is expected to be paid from the primary sources of its liquidity. This will include “over $800 million in cash, its existing $400 million revolving credit facility, and a new one-year, $300 million revolving credit facility.”

“In 2019, we detailed our vision to be the experiential brand that ignites a community of people living the sweatlife through sweat, grow, and connect,” said Lululemon CEO Calvin McDonald. “The acquisition of Mirror is an exciting opportunity to build upon that vision, enhance our digital and interactive capabilities, and deepen our roots in the sweatlife.”

In an interview with CNBC, McDonald said that Mirror has “tens of thousands of subscribers.” He expects to bring in over $100 million in revenue this year and either break even or be slightly profitable in 2021.

Last year, Lululemon expanded its interest in fitness beyond its retail line of yoga apparel with an investment in Mirror for $1 million. Mirror’s interactive, wall-mounted mirror sells for $1,495 with a $39 monthly streaming subscription offering one-on-one personal training sessions and on-demand classes. In-home fitness products have seen an upsurge in sales in light of the COVID-19 pandemic which closed many gyms.

Mirror’s at-home gym competitor and equipment maker, Peloton (PTON) reported earnings in May with sales for last quarter surging 66% from a year ago to $520.6 million. The company stated that its connected fitness subscriber base was up 94% year over year with over 886,100 people.

Like many retailers, Lululemon was impacted by the pandemic with net sales for the quarter ending May 3rd, dropping 17% to $652 million. However, its direct-to-consumer sales jumped nearly 70% according to a company report on June 11.

Susquehanna analyst Sam Poser on Monday reiterated a Buy rating on the stock with a price target of $360 implying 22% upside. “Lululemon has cemented its position as the best publicly traded company in the specialty retailer sector, in our view,” Poser wrote in a note to investors.

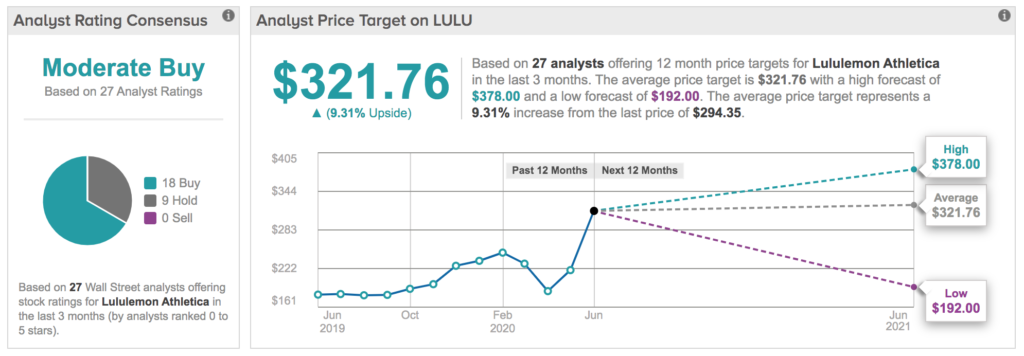

Lululemon’s stock is up 27% year-to-date with a Moderate Buy analyst consensus that breaks down into 18 Buy ratings versus 9 Hold ratings and no Sell ratings. The $321.76 average price target implies 9% upside potential for the shares in the coming 12 months. Shares were up 1.7% at market close on Monday at $294.35 per share. (See Lululemon’s stock analysis on TipRanks).

Related News:

The Growth Story of Lululemon (LULU) Stock Remains Intact, Says 5-Star Analyst

Lululemon Drops 5% in Extended Trading After Quarterly Results Miss

Lululemon Earnings Preview: Will LULU Live Up To The Hype?