Medical device makers are facing challenging times as elective surgeries have either been cancelled or postponed with hospitals and healthcare facilities shifting their entire focus toward addressing the COVID-19 pandemic.

In May, the CovidSurg Collaborative estimated that about 28.4 million elective surgeries could be cancelled or postponed globally in 2020 due to COVID-19. However, the easing of lockdowns and social distancing restrictions is driving the recovery of medical device makers’ sales as reflected in Medtronic’s recent results.

Using the TipRanks’ Stock Comparison tool, we lined up Medtronic and Intuitive Surgical alongside each other to see which stock offers a more compelling investment opportunity.

Medtronic (MDT)

On August 25, Medtronic reported better-than-feared results for the first quarter of fiscal 2021, which ended on July 31. The company’s sales declined 13.2% to $6.51 billion as COVID-19 continued to impact the demand for medical devices. However, sales were well above the analysts’ forecast of $5.54 billion. Management disclosed that procedure volumes began to recover in multiple markets and the recovery was faster-than-expected.

An additional week in the fiscal quarter added sales of $360 to $390 million. Ignoring the impact of an extra week, foreign currency fluctuations and Titan Spine acquisition, the company’s organic revenue declined 17% in the fiscal 2021’s first quarter. The decline rate marked an improvement compared to the 25% fall in fiscal 2020’s fourth-quarter sales. The first-quarter adjusted EPS of $0.62 indicated a 51% decline due to lower sales and margin contraction.

Sales of ventilators more than doubled in the fiscal first quarter. Despite that, sales of the Minimally Invasive Therapies Group sales fell 14.2% to $1.8 billion. Sales of the Cardiac and Vascular Group, Medtronic’s largest business, declined 12.8% Y/Y to $2.4 billion. The Restorative Therapies Group’s sales were down 15% to $1.7 billion while the Diabetes Group’s sales declined 5.1% to $562 million.

Meanwhile, Medtronic has a strong pipeline and received 130 regulatory approvals so far this year in the US, Europe, Japan, and China. Notably, FDA approved the company’s Percept PC deep brain stimulation system with BrainSense technology and the Interstim Micro device for bladder and bowel control. The company secured CE mark for its MiniMed 780G insulin pump.

Plus MDT is eyeing growth in the robotics surgery market. In June, Medtronic teamed up with Titan Medical to develop robotic-assisted surgical technologies. Earlier this year, the company acquired London-based Digital Surgery to bolster its robotic-assisted surgery platform.

Management recognizes that it is lagging in the diabetes market. It is putting efforts to advance its technology in this area and grow through organic investments and acquisitions like that of smart insulin pen maker Companion Medical.

Several analysts raised their price targets for Medtronic stock following the company’s first-quarter results. BTIG analyst Ryan Zimmerman reaffirmed a Buy rating and increased his price target to $111 from $102. He said, “In our view, the most notable aspect of the call was mgmt.’s tone around the company’s reinvigorated pipeline and outlook for revenue growth.”

He added, “We expect MDT and investors to reap the benefits of a steady cadence of product introductions in the back half of FY21, and longer-term we believe these products could materially shift MDT’s growth profile on a sustainable basis.” The analyst sees the stock rising based on attractive valuation, higher market share, and robust product pipeline. (See MDT stock analysis on TipRanks)

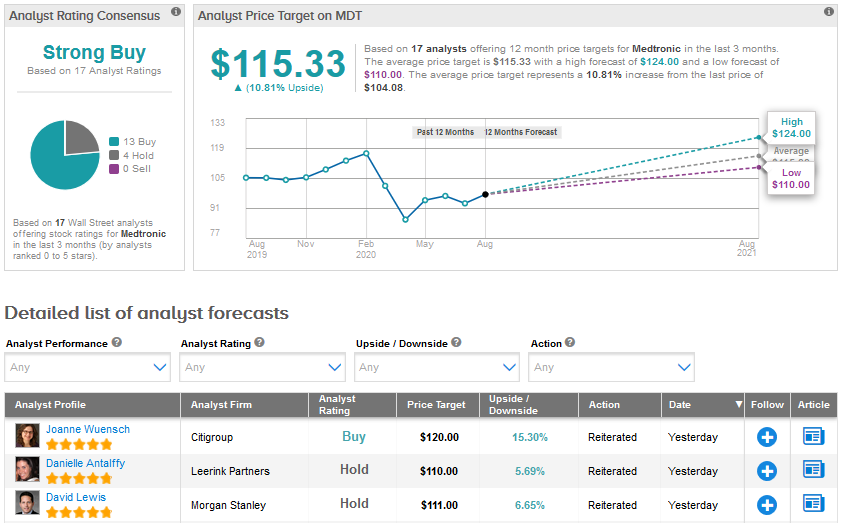

Medtronic stock is down 8.3% year-to-date. However, the Street has a Strong Buy MDT consensus based on 13 Buys, 4 Holds and no Sell rating. There could be an upside of 10.8% in the stock over the next 12-months based on the average analyst price target of $115.33.

Intuitive Surgical (ISRG)

Intuitive Surgical is the leader in the robotic-assisted surgery devices market. The company generates revenue through the sales of its da Vinci Surgical systems, instruments and accessories. The Da Vinci Surgical system is expensive and to expand its reach the company started leasing its robotic surgical systems in 2013.

A notable feature about Intuitive Surgical is its high recurring revenue. In 2019, the company’s recurring revenue, which includes revenue from instruments and accessories, service revenue and operating lease revenue, accounted for 72% of the overall revenue.

Intuitive Surgical’s revenue grew 20.3% to $4.48 billion in 2019. However, the pandemic significantly slowed down the company’s growth as elective procedures were either delayed or cancelled.

Most notably, the second-quarter revenue declined 22.5% to $852.1 million, following a 13% rise in the first quarter. The second-quarter adjusted EPS fell 66% to $1.11.

And while the installed base of da Vinci Surgical System grew 9% Y/Y to 5,764 systems, the da Vinci procedures were down 19% globally due to the pandemic and led to a 20.3% fall in the company’s instruments and accessories business. Revenue from systems and services declined 24.1% and 26.2%, respectively.

Management cautioned that system placements will continue to be under pressure due to the impact of COVID-19 and economic uncertainty on hospital spending. The company shipped 178 da Vinci Surgical Systems in the second quarter, reflecting a 35% drop.

On August 14, Leerink Partners analyst Richard Newitter raised the price target for Intuitive Surgical to $690 from $650 following his conversation with management. He continues to believe that the company is a “premium MedTech asset with a large underpenetrated TAM [Total Addressable Market] that should continue to fuel a long-term multi-year growth story.”

However, the analyst maintained his Hold rating as he would prefer a more attractive entry point in the shares “especially with the near-term hospital cap-ex spend outlook still uncertain and potentially limiting near-term estimate upside prospects.” (See ISRG stock analysis on TipRanks)

Intuitive Surgical stock has risen 18.4% year-to-date. The average analyst price target of $675.62 suggests a possible downside of 3.5% over the next 12-months. The Street has a cautiously optimistic Moderate Buy consensus for Intuitive Surgical based on 9 Buys, 5 Holds, and 1 Sell.

So which stock is a better pick right now?

Intuitive Surgical is a pioneer in the robotic-assisted surgeries market and it is well-positioned to capture the growing demand for robotic surgery devices in the long-term though COVID-19 related headwinds might impact the near-term demand.

Intuitive Surgical does not pay any dividends while Medtronic is a dividend aristocrat and has raised its dividends for 43 straight years. Medtronic has a dividend yield of 2.2%. Amid the current crisis, Medtronic looks to be a better choice based on its diverse product portfolio, strong pipeline, dividends and the Street’s optimism.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment