The Walt Disney Co. reported fiscal 1Q earnings per share (EPS) of $0.32 as customers signed up for the entertainment company’s streaming services during the coronavirus pandemic. Meanwhile, analysts had expected a loss of $0.45 per share. Shares rose 1.6% in Thursday’s after-market trading.

The profit was fueled by demand for Disney’s (DIS) streaming service, Disney+, which launched in a number of geographies, including India and Indonesia last year, pushing subscriber numbers up 100% year-on-year to 94.9 million. Disney’s ESPN+ streaming service saw a 83% year-on-year jump in subscribers to 12.1 million.

Revenues in the fiscal first quarter were down 22% year-on-year to $16.2 billion but beat consensus estimates of $15.8 billion.

Disney’s CEO Bob Chapek said, “We believe the strategic actions we’re taking to transform our Company will fuel our growth and enhance shareholder value, as demonstrated by the incredible strides we’ve made in our DTC [direct-to-consumer] business, reaching more than 146 million total paid subscriptions across our streaming services at the end of the quarter.”

Chapek added, “We’re confident that, with our robust pipeline of exceptional, high-quality content and the upcoming launch of our new Star-branded international general entertainment offering, we are well-positioned to achieve even greater success going forward.”

Revenue and operating income at the company’s theme parks, experiences and product segment were still severely affected by the pandemic-led closures of its entertainment parks. As a result, the theme parks business segment saw a 53% year-on-year drop in revenues to $3.6 billion. The segment incurred an operating loss of $119 million in 1Q versus a profit of $2.5 billion during the same period last year. (See Walt Disney stock analysis on TipRanks)

Disney expects COVID-19-related costs, due to government regulations and safety measures, to amount to $1 billion in FY21.

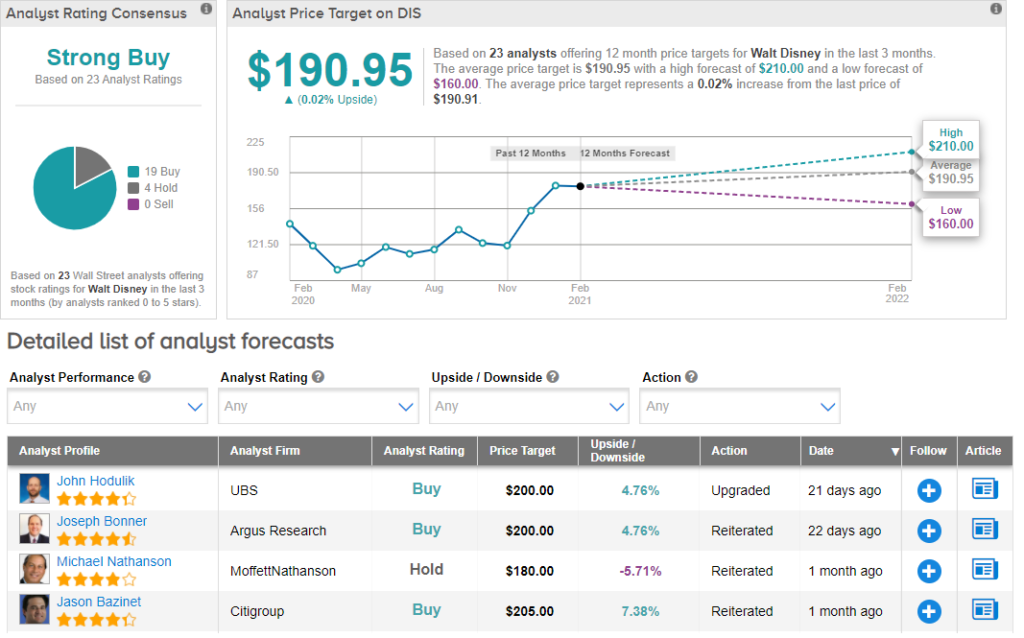

Last month, UBS analyst John Hodulik upgraded the stock from Hold to Buy and assigned a $200 price target, up from $155.

Hodulik wrote in a note to investors, “We believe Disney is positioned to achieve scale similar to industry leader Netflix with 340 million+ global subscribers by 2024, while its premium IP creates pricing power and enables the company to spend less per sub on content, driving better economics over time.”

The analyst expects Disney’s theme parks business segment to do better in the second half of this year due to a pent-up demand for leisure travel and as more and more people get vaccinated.

The rest of the Street is in line with Hodulik’s view with a Strong Buy consensus rating. That’s based on 19 analysts suggesting a Buy and 4 analysts recommending a Hold. The average analyst price target of $190.95 implies that shares are fully valued at current levels.

Related News:

iRobot Spikes 9% On 4Q Profit Beat; Street Says Hold

Baidu In Talks To Raise Funds For Semiconductor Company – Report

Microsoft Showed Interest In Pinterest Takeover – Report