Shares of Chipotle Mexican Grill fell 3.8% in the extended trading hours on Wednesday even after the company’s third-quarter results beat analysts’ expectations. The company’s 3Q adjusted EPS of $3.76 exceeded analysts’ estimate of $3.47 but declined 1.6% Y/Y due to higher costs to support robust growth in delivery sales.

Aside from delivery costs, Chipotle’s (CMG) 3Q operating margin and the bottom line were also hurt by elevated beef prices, increased steak orders, and fewer sales of high-margin beverages.

Reopening of restaurants and digital sales growth of 202.5% helped the company in delivering revenue of $1.60 billion in 3Q, reflecting a 14.1% Y/Y growth. Analysts predicted revenue of $1.59 billion. The company bounced back well from a 4.8% revenue decline in 2Q. Comparable restaurant sales increased 8.3% in 3Q as comps were strong in each month of the quarter with August being the high point.

Digital sales accounted for about 49% of the overall 3Q revenue. The company stated that about half of its digital sales were through delivery services. Owing to concerns related to COVID-19, fast food chains and restaurants are seeing higher demand for delivery services offered on sales placed through their apps and websites.

Meanwhile, Chipotle opened 44 new restaurants in 3Q and closed 3, ending the quarter with 2,710 restaurants. Also, 26 of the new restaurants opened in the quarter included a Chipotlane, which is a drive-thru pick-up lane for orders placed through digital channels.

The company stated that though the current uncertainty prevents it from issuing reliable new store guidance for 2021, it expects to open about 200 restaurants next year. Over the long-term, the company is optimistic about increasing its US restaurants count by more than double.

Given the COVID-19 related uncertainty, the company did not provide guidance for the current year. The company disclosed that from mid-September, its comparable restaurant sales grew mid-single digits and this trend has continued in October. (See CMG stock analysis on TipRanks)

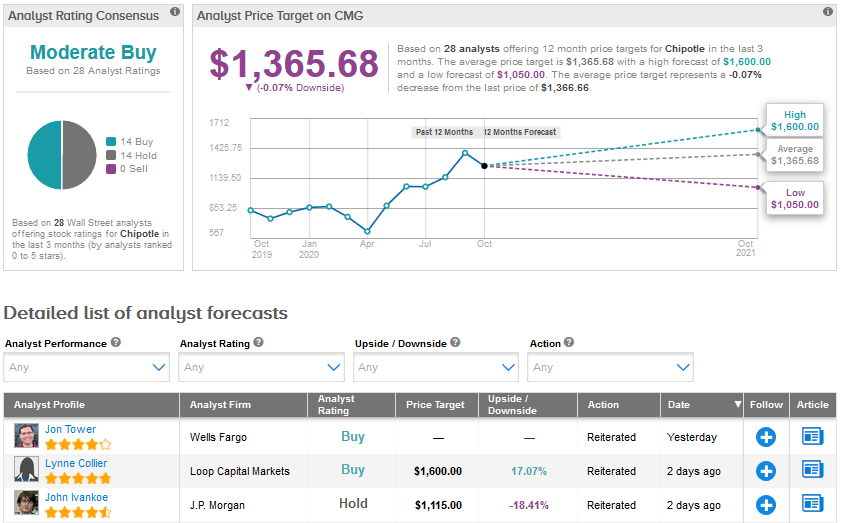

Ahead of the results, Loop Capital analyst Lynne Collier increased her price target for Chipotle to $1,600 from $1,400 and maintained a Buy rating. The analyst stated that her store checks indicate positive data and she sees a “long runway of initiative” to drive Chipotle’s sales momentum for the next several years.

Collier said that the company’s sales growth catalysts include digital, the roll-out of Chipotlanes, the company’s loyalty program, and its “menu innovation”.

A cautiously optimistic Moderate Buy consensus for Chipotle is based on 14 Buys and 14 Holds. With shares surging 62.7% year-to-date, the average analyst price target of about $1,366 indicates that shares are fully priced at the current levels.

Related News:

Albertsons Jumps 5.6% As Online Sales Pop 243%

Procter & Gamble Raises 2021 Outlook As 1Q Sales Surge 9%

Philip Morris Slips 6% As 4Q Profit Outlook Misses Estimates