Biotechnology company BioMarin Pharmaceutical (BMRN) posted 1Q results that beat analysts’ estimates. Revenue decreased 3.2% year-on-year to $486 million but came in $39.65 million ahead of consensus forecasts. GAAP earnings per share came in at $0.09 versus analysts’ estimates for a $0.10 loss.

The decrease in revenue was mainly attributable to generic competition leading to a 42% year-on-year drop in sales of Kuvan to $70.8 million, which was partially offset by a 56% year-on-year jump in Palynziq sales to $54 million.

Commenting on forthcoming regulatory events in 2021, BioMarin Chairman and CEO Jean-Jacques Bienaimé said, “The potential approval in Europe this summer of vosoritide, the first potential therapeutic option for children with achondroplasia, will set the stage for our next significant phase of growth, especially considering the EMEA region is 3 times larger than the U.S. market.”

Bienaimé added, “We plan to re-submit the application for valoctocogene roxaparvovec gene therapy, to treat hemophilia A, to the EMA in the second quarter, to be followed by potential approval of vosoritide in the United States later this year.”

BioMarin expects a 35% year-on-year increase in Palynziq sales in 2021. The therapy has seen a 20% jump in U.S. patients year-on-year and this number is expected to further increase as PKU clinics are expected to reopen in the coming quarters.

BioMarin estimates sales for fiscal 2021 to range between $1.75 billion and $1.85 billion, with non-GAAP income expected to be in the range of $170 million to $220 million . (See BioMarin stock analysis on TipRanks)

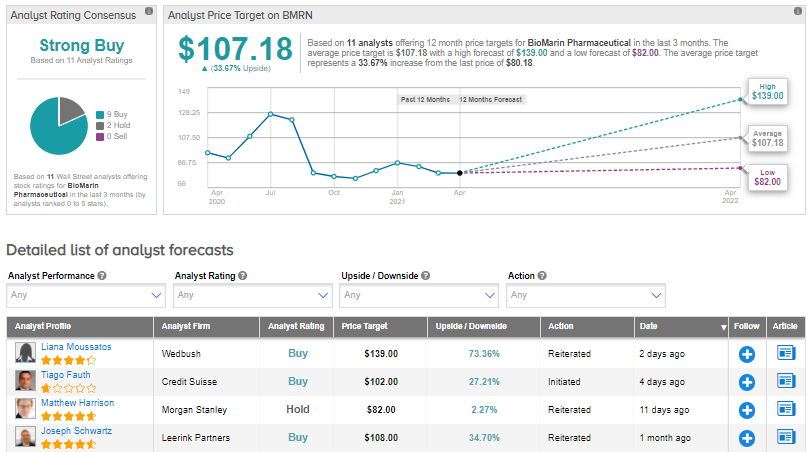

On April 28, Wedbush analyst Liana Moussatos reiterated a Buy rating on the stock with a $139 price target (73.4% upside potential).

Moussatos noted that BioMarin’s collaboration with the Allen Institue (Announced on April 28) expands its product pipeline into rare central nervous system diseases.

Moussatos also noted that unfavorable forex impacts and timing uncertainties in inventory transfers, government contracts, and order shipments make sales forecasting difficult as the company’s quarterly sales reporting can be “Choppy”.

Overall, consensus among analysts is a Strong Buy based on 9 Buys and 2 Holds. The average analyst price target of $107.18 implies 33.7% upside potential. Shares have dropped about 14.9% over the past year.

Related News:

eBay’s 2Q Earnings Outlook Disappoints After 1Q Beat, Shares Drop 5.4%

Teladoc Health Reports Mixed Results In 1Q; Shares Drop 5.5%

Apple’s 2Q Sales Pop 54% As Services and Mac Revenue Booms; Shares Gain After-Hours