Apollo Global Management said it has inked a deal to snap up Great Canadian Gaming Corp. for a total enterprise valuation exceeding C$3.3 billion ($2.53 billion).

According to the terms of the transaction, Apollo (APO) will buy all of the outstanding shares of Great Canadian common stock for C$39 per share. The purchase price represents a premium of about 35% as of Tuesday’s close and a 59% premium to the 30-day VWAP as of November 9. Apollo intends to help drive additional, incremental growth through initiatives such as expansion of non-gaming facilities, expanded loyalty and marketing programs, and gaming improvements.

Founded in 1982, Great Canadian is an Ontario-based company that operates 25 gaming, entertainment and hospitality facilities in Ontario, British Columbia, New Brunswick, and Nova Scotia.

“Great Canadian is a leader in the gaming and entertainment industry and, based on our experience and knowledge of the space, we see opportunities to drive additional growth and value,” said Apollo Partner Alex van Hoek. “We also recognize the challenges of the current circumstances and are committed to working with the management team, regulators and health authorities to allow the Company to reopen its properties as soon as it’s safe to do so.”

The transaction is expected to close in the second quarter of 2021. Following the closure, Great Canadian will remain headquartered in Toronto, led by a Canadian management team, with Canadian board members. Apollo also expects Canadian institutions to co-invest in the deal to become equity owners in the company alongside the alternative investment manager once the acquisition is completed.

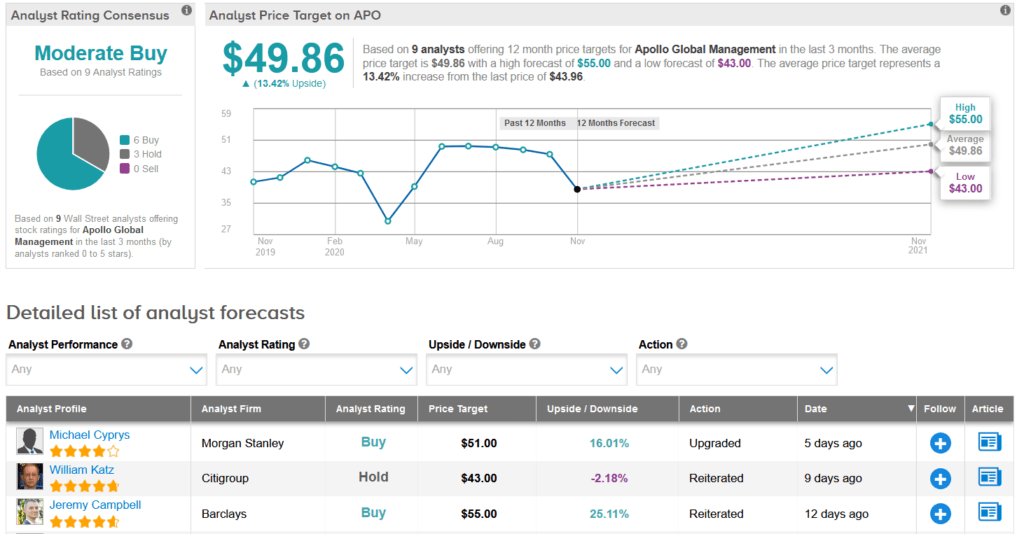

Shares in Apollo have rallied 12% over the past five days, but are still down 7.8% on a year-to-date basis. Looking ahead, the average analyst price target stands at $49.86, implying 13% upside potential over the coming year.

Morgan Stanley analyst Michael Cyprys on Nov. 6 raised the stock’s rating to Buy from Hold with a $51 price target, saying that it offers “compelling value with the market overly discounting key-man risk, despite existing succession planning and a strong bench.”

“Apollo is one of only a handful of phenomenal franchises in the alternatives space,” commented Evercore ISI analyst Glenn Schorr, who last month upgraded the stock to Buy. “Unlike the fragmented traditional asset-management industry, there are only a few alternatives managers who can run money for big institutions searching for non-correlated assets and higher returns.”

The rest of the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is backed by 6 Buy ratings versus 3 Hold ratings. (See APO stock analysis on TipRanks)

Related News:

Take-Two In Bid To Snap Up Codemasters In $973M Videogaming Deal

Trade Desk Pops 27% On Record Quarterly Sales; Analyst Lifts PT

GoPro Jumps 16% On Blowout 3Q; Wedbush Raises PT