Analysts from Credit Suisse and Morgan Stanley explain how new product launches will affect shares of Apple Inc. (NASDAQ:AAPL) and BlackBerry Ltd (NASDAQ:BBRY). While one analyst is bullish on Apple’s iPhone entering the mid-tier market, the other questions Blackberry’s new Priv model’s overall profitability amidst slowing growth from other segments.

Apple Inc.

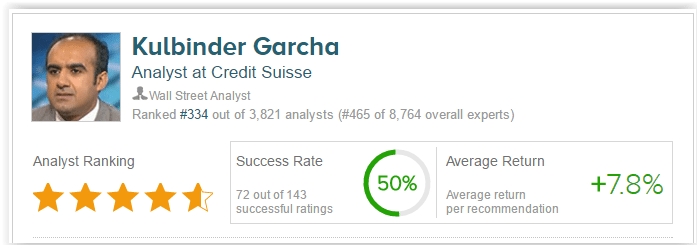

Analyst Kulbinder Garcha of Credit Suisse weighed in on Apple yesterday following the company’s product launch event, where Apple released a 4-inch iPhone SE, a new iPad Pro, additional bands for the Apple Watch, and various software updates.

The analyst is particularly bullish regarding the new 4-inch iPhone’s lower price point of $399 and the additional features represent “a solid move for the iPhone business” for a few reasons. First, the product will make Apple a more viable competitor with other ASP smartphone products priced between $300-$500. Second, the analyst believes the new model will be an “additive to units, projecting ~18mn/30mn units for iPhone SE, in CY16/17.”

While cannibalization does present a risk to current high end users, the analyst believes it will only apply to 6/6S 16GB users , subjecting only 16 million units. Garcha states the new model will result in more upgrade cycles for the iPhone as well as the purchase other products. He states “Finally, the iPhone SE should grow Apple’s iPhone installed base of 600mn active devices given its high levels of retention and could also provide Apple with new users who may upgrade to higher price points over time as well as potentially buy other Apple compute devices.” Although the company released a new, smaller version of the iPad pro, the analyst does not change his estimates for the product and cites only “modest upside over time.”

The analyst reiterated an Outperform rating on the company with a $140 price target. He states, “We believe that the releases complement Apple’s solid portfolio in the compute market. According to TipRanks, Kulbinder Garcha has a 50% success rate recommending stocks with an average return of 7.8% per recommendation.

Out of the 37 analysts who have rated the company in the past 3 months, 31 gave a Buy rating, 1 gave a Sell rating, and 5 remain on the sidelines. The average 12-month price target for the stock is $135.26, marking a 26% upside from current levels.

BlackBerry Ltd

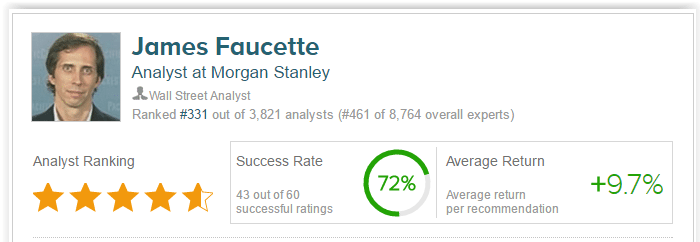

Morgan Stanley analyst James Faucette weighed in on Blackberry prior to its Q4:16 earnings release next week. Specifically, he comments on the recently released Priv model and how a change in revenue recognition will affect profitability. His checks indicated a “slight improvement in demand and availability” compared to other BBRY product launches and a change in revenue recognition to sell-in vs sell –through caused the analyst to slightly up his sales estimates. However, he does not believe the product will have enough demand to meet the company’s 5 mm unit break-even level despite recently reduced headcount. Instead, the company will “need to launch multiple new devices before the segment could achieve standalone profitability.”

Faucette also comments on the company’s recent acquisitions, which should provide “a better sense of the organic growth from software” for investors. However, he points to management’s cautionary comments at CES” and the lack of its legacy service and support segments from revenue calculations as a questionable sign, alluding to slow growth from core QNX, BES12, Certicom and BBM. He states, “Without demonstrating sustained growth after acquiring revenue, we continue to believe the market gives too much credit for software at current valuations.”

As a result of the Priv launch data, the analyst slightly raises his 4Q16 revenue and EPS estimates, though slightly decreases his FY17 revenues due to “pull forward in Priv revenue after changing recognition to a sell-in basis.” Overall, the analyst states that product development plans mixed with “insufficient” software revenue growth will weigh negatively on the company’s net cash position despite cost-cutting measures.

The analyst reiterates his Equal Weight rating with a $7 price target. He states “For the time being, the flexibility of the balance sheet, the opportunity for further cost cuts in the core business and acquired assets and the ability to generate cash at reduced revenue levels outweigh poor business fundamentals for the time being.”

According to TipRanks.com, analyst James Faucette has a total average return of 10% and a 72% success rate. Faucette is ranked #331 out of 3757 analysts.