As 2017 winds to a close, what key gold takeaways and sharpest insights stand out from the year?

When Does Gold Thrive? The Shiny Metal Can Succeed in Good Times

First, gold actually can shine amid a sour macroeconomic backdrop. Generally speaking, gold’s performance prospers most throughout an economic slowdown or even turmoil. Consider that through the course of this year, the conditions seen from the economy ranged far from a climate of recession. Economic gains from around the world fired up, becoming all the more synchronized among nations. The economy on the domestic front performed quite well, the unemployment rates sank to a historic low, and all the while inflation continued to be subdued.

The Fed hiked interest rates three times, while the Republicans managed to pass a tax bill. Meanwhile, the U.S. stock market kept up its rally as cryptocurrencies skyrocketed on a parabolic rise at the end of a year.

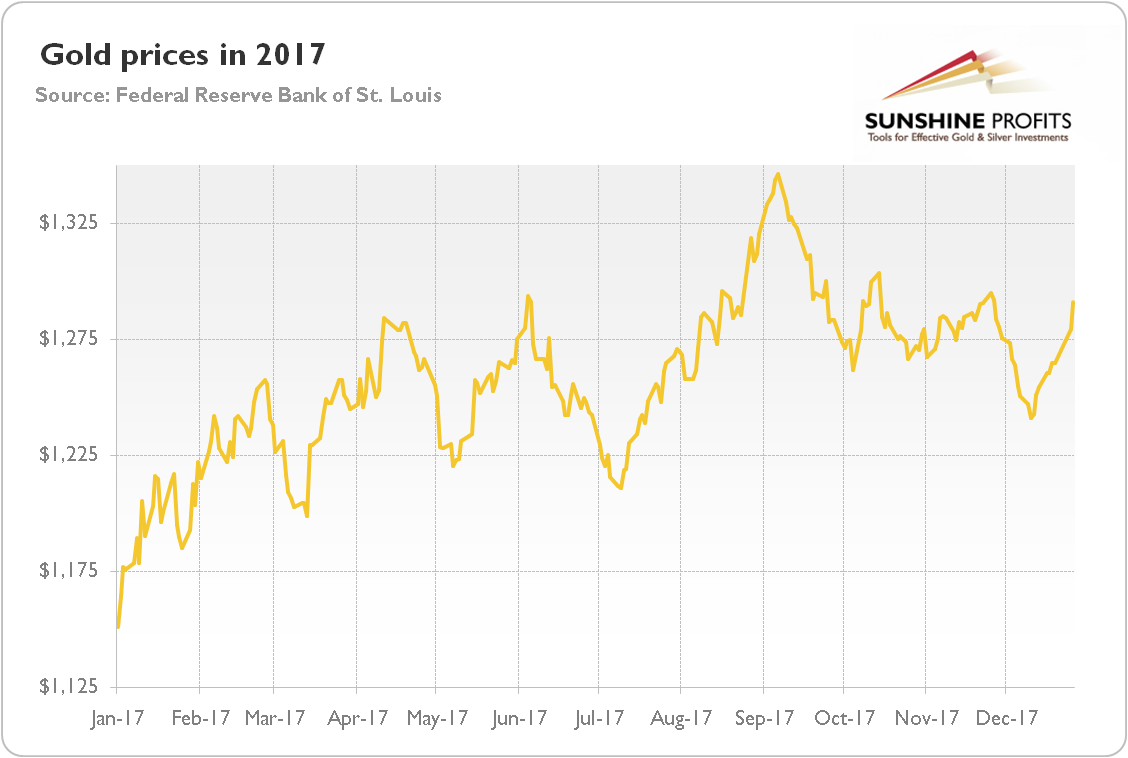

Does it look like a supporting environment for gold? Not really. However, worthy of note, the price of the yellow metal has risen past 12 percent in 2017, as can be seen in the chart below. Perhaps it’s not very impressive, but not bad given the state of the macroeconomic environment- and much better than a savings account or Treasuries.

Chart 1: Gold prices over the last twelve months.

Gold Is Largely Tied to the U.S. Dollar

How was gold able to gain beyond 12 percent this year, a year that suffered from an unpleasant macroeconomic atmosphere afflicting other precious metals? A weak greenback. The broad trade-weighted U.S. dollar index fell from 128 to 120, or more than 6 percent. Real interest rates are also an important driver of the price of gold, but the correlation was significantly stronger with the greenback in 2017. And the level of yield of the inflation-protected 10-year Treasuries at the end of the year was similar to the level at the beginning of the year (about 0.5 percent). The end verdict to be drawn is clear: the dip in the U.S. dollar’s value distinctively supported the yellow metal over the last twelve months. Given that gold is a bet against the greenback, it is not surprising. Thus, one can bank that the key to gold’s future rests in the hands of the U.S. dollar.

Gold Is Not a Perfect Hedge Against Geopolitical Risks

This year was perhaps not very politically turbulent, at least compared with the year before, when markets had to deal with surprising outcomes between the Brexit referendum and the whirlwind U.S. presidential election. However, the crisis over the Korean Peninsula revived. For many years, North Korea was a small and fusty country. Yet, in 2017 North Korea evolved, suddenly becoming a nuclear power able to threaten the U.S. with a hydrogen bomb. The price of gold reacted to the war of words between President Trump and Kim Jong-un. But the incidents related to North Korea failed to trigger anything but a short-term and limited response in the gold market.

Investors should always remember this and do not make long-term investments in gold based on geopolitical risks. In other words: although gold may rise after some unexpected conflicts (especially if they threaten the U.S. economy), never forget long-term trends in the gold market are shaped by fundamental factors, including the likes of the U.S. dollar’s strength or real interest rates instead of geopolitical threats.

Gold’s Volatility Was Very Low

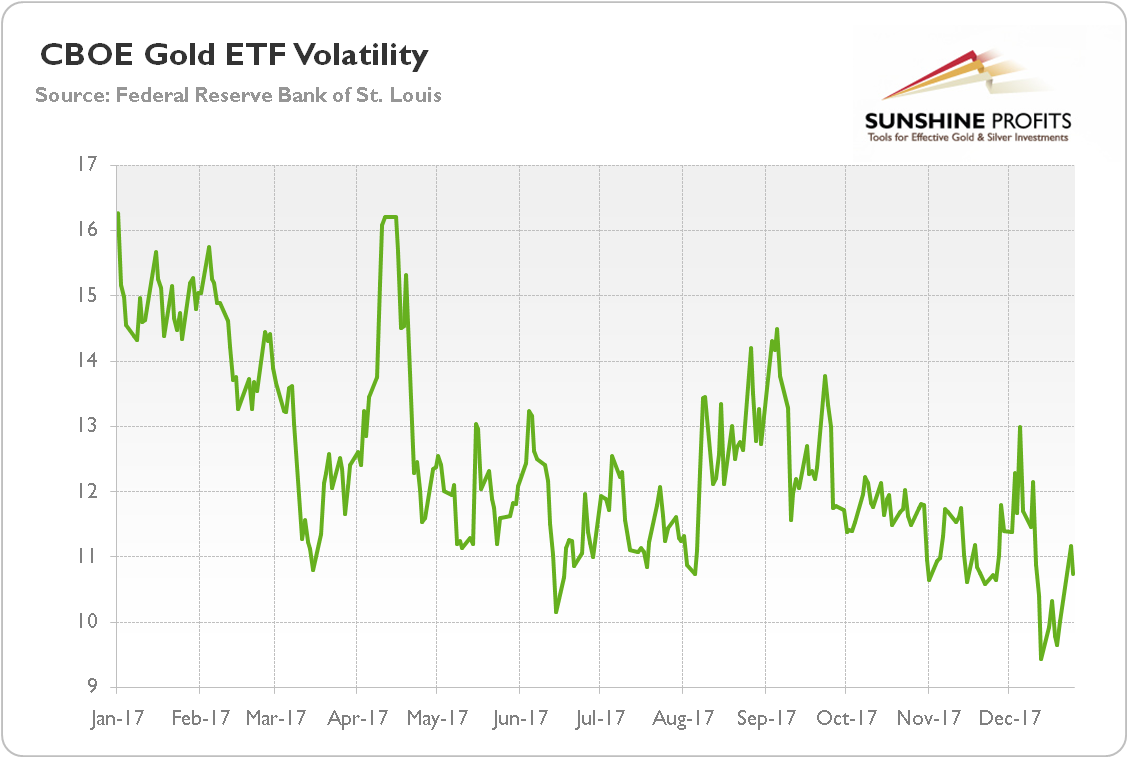

The volatility of gold has been on a downward turn this year. As the chart below indicates, the CBOE Gold ETF Volatility Index, which measures implied volatility calculated through call and put options, has declined from 16.23 to 10.73 over the year.

Chart 2: CBOE Gold ETF Volatility Index over the last twelve months.

The low volatility in the gold market in 2017 (especially at the end of the year) was not something unusual, but it was a reflection of a general low volatility in the financial markets; partially due to the presence of central banks. Gold prices remained in a narrow trading range, as investors got used to the presidency of Trump and the Fed’s tightening cycle. However, it may be the calm before the storm. The big jump in the price of gold may follow the unusually quiet period in the gold market.

Golden New Year

For long-term investors, low volatility is overall positive. However, the sideway trend may be discouraging. Looking ahead, we can only hope for a New Year with a more dynamic gold market and many profitable trading opportunities.