Two well known companies, SolarCity Corp (NASDAQ:SCTY) and Microsoft Corporation (NASDAQ:MSFT) have been in the news lately regarding acquisitions. Below, analysts discuss Microsoft’s business plans after acquiring LinkedIn and how SolarCity shares will react to Tesla’s acquisition offer.

SolarCity Corp

Analyst Patrick Jobin of Credit Suisse expresses his concerns regarding the approval of Tesla’s proposed offer to acquire SolarCity. Nonetheless, he expresses a short-term bullish view towards SolarCity due his opinion that the announcement will “force SolarCity shorts to cover.”

After markets closed on Tuesday, CEO of Tesla Elon Musk offered to acquire SolarCity. Musk co-founded the company and owns over 20% of its stock, at a premium of 21% to 30%. The proposal has to be approved by SolarCity’s board and voted on by the shareholders of both companies before becoming final. Elon Musk, Antonio Gracias, who sits on the board of both companies, and the CEO of SolarCity, Lyndon Rive, have all agreed to recuse themselves from the shareholder vote.

As a result of the announcement, the analyst expects SolarCity’s shares to soar in the short-term due to investors being forced to end their short positions. He stresses that he only gives the acquisition a 20%-40% chance of going through because of “corporate governance questions and likely shareholder opposition.”

Jobin is not sold on Tesla’s “strategic and financial rationale” behind the proposed acquisition and anticipates Tesla shareholders to feel the same way due to “intense skepticism of the residential solar space, the regulatory risk and vociferous consumption of capital, combined with the limited synergies.”

The analyst feels that SolarCity and Tesla could have worked together in a partnership model and therefore an ownership model is unnecessary. Many investors believe that the main benefit arising from this potential acquisition is an improvement in access to capital markets for SolarCity. Jobin is skeptical of this benefit because of his doubts regarding approval. Additionally, during the approval process SolarCity will be cut off from corporate-level fundraising and Tax Equity, which could prove to be detrimental if the process drags on. This possible disruption to access to capital markets over the next 3-9 months causes Jobin to warn of “medium-term risks.”

Jobin maintains his Outperform rating on SolarCity with a target price of $38, marking an 74% increase from current levels.

According to TipRanks, out of the 16 analysts who have rated the company in the past 3 months, 31% gave a Buy rating, 56% gave a Hold rating and 13% gave a Sell rating. The average 12-month price target for the stock is $30.60, marking a 40% upside from current levels.

Microsoft Corporation

Analyst Phillip Winslow of Credit Suisse discusses Microsoft’s long term plans after acquiring LinkedIn for $26.2 billion two weeks ago. The analyst feels that the acquisition of LinkedIn is compatible with Microsoft’s focus on, “boosting growth in Office 365 and Dynamics CRM, improving the growth and profitability of its search-related businesses, and differentiate its platform capabilities.”

LinkedIn will continue to operate independently, but Microsoft envisions integrating LinkedIn Recruiter, Sales Navigator and Social Selling into Dynamics CRM, Microsoft’s platform that helps companies with their customer service. Microsoft is also starting an initiative, Office Graph, to integrate data between the two companies. Additionally, the analyst expects that Microsoft will improve LinkedIn’s sales and market expenses and capital spending, thus improving its margins.

Winslow anticipates double-digit EPS growth for the company due to several changes Microsoft is undergoing including a more efficient cost structure, the selling off of non-core businesses and “optimization of its capital structure.” With regards to specific Microsoft products, the analyst expects to see several changes. These include more stable Windows pricing and an accelerated shift to Office 365, a subscription that allows access to productive Office applications. The analyst also predicts that Microsoft Azure, a cloud computing program, will emerge as the second “market share player in public IaaS and will arise as a leader in public PaaS.”

Winslow reiterates his Outperform rating on Microsoft, with a target price of $62.50, marking a 23% increase from current levels.

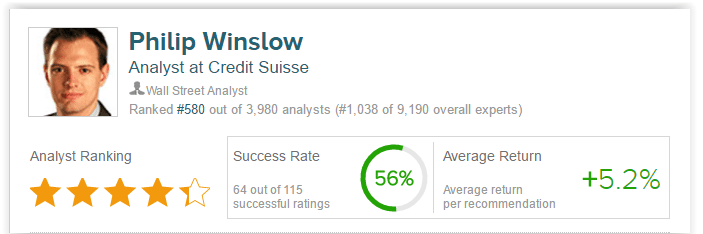

According to TipRanks.com, which measures analysts’ and bloggers’ success rate based on how their calls perform, analyst Philip Winslow has a yearly average return of 5.2% and a 56% success rate. Winslow has a 12.8% average return when recommending MSFT, and is ranked #580 out of 3980 analysts.

Out of the 24 analysts polled by TipRanks in the past 3 months, 71% gave a Buy rating, 21% gave a Hold rating and 8% gave a Sell rating. The average 12-month price target for the stock is $58.37, marking a 14.47% upside from current levels.