Healthcare analysts give their two cents on recent updates by MannKind Corporation (NASDAQ:MNKD) and Dynavax Technologies Corporation (NASDAQ:DVAX). One analyst remains on the sidelines for MannKind as the company relaunches diabetes drug Afrezza, but not without challenges to raise capital. On the other hand, another analyst does not believe a regulatory hurdle will impact a vaccine’s chances of approval, citing a compelling entry point for Dynavax shares.

MannKind Corporation

JMP Securities analyst Jason Butler provided his insights on MannKind after the company announced its commercial strategy to relaunch Afrezza, its inhalable insulin drug, in the U.S. The company’s partner to develop and sell the drug, Sanofi, backed out of the deal in early January due to disappointing sales, leaving MannKind to develop and market the drug alone. MannKind plans to re-launch Afrezza in the U.S. in 3Q:16 and will inform investors on its strategy to raise additional capital.

Butler details the company’s new strategy and its differences following the Sanofi termination. He states, “The strategy will entail focusing on endocrinologists, increasing patient retention in the first 60 days, and continuing to increase patient access.” The company will target between 5,000-7,000 endocrinologists rather than the 3,000 during the initial launch. The analyst states, “Based on the company’s market research, it believes endocrinologists are more likely to be early adopters of Afrezza and are also more willing to be educated and, in turn, to educate patients on the merits and optimal use of the product.”

The second part of the company’ relaunch strategy is to increase patient access to the drug, as 30% of patients who complete the authorization process are rejected from approval. MannKind intends to solve this through a co-pay program and its own prior authorization in the third quarter of 2016. Finally, the company would like to increase patient retention by reducing the patient drop-out rates in the first 60 days of treatment. Butler explains, “To achieve this, MannKind plans to make titration of Afrezza more convenient and to concentrate on endocrinologists who are more focused on diabetic patients.” He continues, “With proper education, physicians can properly titrate the patients in the critical first 30 to 60 days, reducing previous elevated drop-out rates in this initial period.”

The analyst cites CCO Michael Castanga’s belief that Afrezza suffered low sales in the beginning of 2016 due to a feared U.S. discontinuation of the drug. However, now that the drug is relaunching, “the company anticipates stabilization of prescriptions in the coming weeks.” Furthermore, MannKind intends to expand internationally in countries with more lenient approval requirements. Finally, the analyst notes that the “company has not ruled out re-partnering the asset” though this is contingent upon “demonstration of significant commercial success.”

The analyst reiterates a Market Perform rating on the company without a price target, noting “the risks associated with the challenging launch of Afrezza thus far, and the near-term need for additional sources of funding.”

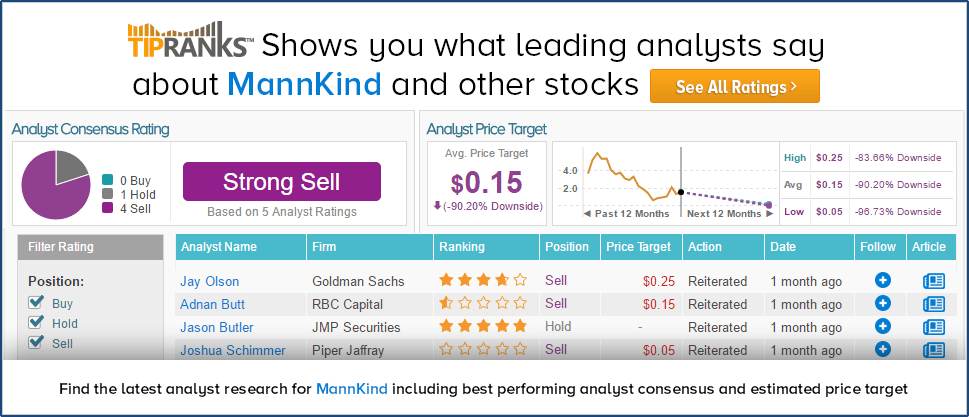

According to TipRanks, Jason Butler has a 59% success rate recommending stocks with an average return of 44.8% per recommendation.

Out of the 5 analysts who have rated the company in the past 3 months, 4 are bearish while 1 remains on the sidelines. The average 12-month price target for the stock is $0.15, marking a 90% downside from where shares last closed.

Dynavax Technologies Corporation

Analyst Phil Nadeau of Cowen & Co. weighed in on Dynavax after news that the FDA has extended the PDUFA date for Heplisav, the company’s investigational Hep B Vaccine, from September 15, 2016 to December 15, 2016, after the company submitted additional data from specific trials, per the FDA’s request.

The analyst does not believe this extension will impact the drug’s chances of approval. If anything, the analyst notes that the FDA is struggling to “[manage] its workload” and the submission request has “little reflection on the content or substance of the BLA.” He explains, “We suspect that the significant size of Heplisav’s database made a 6 month review challenging for the FDA. Therefore we think the FDA wanted more time for the review.” The analyst notes that DVAX already had recently requested individual trial data in January and could have included this data in the original BLA if the FDA requested. Furthermore, the FDA has not indicated any efficacy or safety concerns regarding Heplisav’s trials.

Despite the FDA’s request for additional data, the analyst believes Heplisav will gain FDA approval by the end of 2016 due to its convenience and efficacy over competitors. He states, “We expect that over time it will gain majority share in the HBV vaccine market.” The analyst predicts a $500 million global opportunity for HBV vaccines and predicts favorable market conditions for DVAX. He explains, “Heplisav-B’s combination of superior efficacy and more convenient dosing should allow for pricing somewhat above market leader Engerix ($162/course). Increased compliance and expanded use among target populations including diabetics should also expand the market.” By 2020, Nadeau believes this opportunity should grow to $700 million.

The analyst reiterates an Outperform rating on the company with a $60 price target. He states, “We view the company as significantly undervalued based on Heplisav’s potential.”

According to TipRanks, Phil Nadeau has a 49% success rate recommending stocks with a 4.2% average return per recommendation. Only one other analyst rated the stock in the past 4 months with a Hold rating and $22 price target, marking a 19% upside from where shares last closed.