Thursday was not a good day to be invested in Canadian cannabis company Aurora Cannabis (ACB).

Last month if you recall, Canada’s second largest marijuana company lowered guidance for fiscal Q4 sales with an earnings pre-announcement warning that sales would range from only $100 million to $107 million. Wall Street assumed Aurora management was lowballing its estimates, though, with analysts’ consensus expectations continuing to call for sales of $108 million heading into earnings.

Instead, Aurora missed its own guidance range (and Wall Street’s) entirely, reporting Wednesday evening that its actual sales for the final quarter of fiscal 2019 were only $98.9 million.

Earnings were a disappointment, too. And to be clear, we’re talking here not about actual GAAP earnings, but just the more lenient version — earnings before interest, taxes, depreciation, and amortization — that Wall Street has been focusing on all across the marijuana industry (in an implicit acknowledgement that none of these companies are going to be truly profitable anytime soon).

In its Q3 earnings report, Aurora management had hinted that after several quarters of negative margins, it might finally turn EBITDA-profitable in Q4. Heading into earnings day, some analysts agreed that profitability was on the horizon — while the consensus on Wall Street was that Aurora would report a slightly negative EBITDA of $4.1 million.

As it turned out, EBITDA for the quarter was negative $11.7 million, far worse than anyone expected.

Even that negative EBITDA number doesn’t capture the full extent of how much money Aurora Cannabis is burning however. In a note following the earnings release, Seaport Global analyst Brett Hundley pointed out that Aurora increased the amount of cash spent on capital improvements by 73% year over year. The $167.4 million in capital expenditures made in the quarter, when added to the $4.6 million in negative cash from operations, resulted in total free cash flow of negative $172 million.

With cash reserves dwindling, and no cash coming in from operations to offset them, Hundley warned: “Assuming overall cash burn remains at elevated levels” — and Aurora management in fact confirmed that it will continue to spend heavily on capex through next quarter at least — [then even “accounting for additional cash from its expanded credit facility and disposal of Green Organic Dutchman shares, the company has enough cash on hand [to fund only about] 2.4 quarters of operation.”

That gives Aurora barely half a year to figure out a way to make money selling marijuana — or else issue and sell a bunch of new shares to keep itself solvent.

Commenting on the results, BMO Capital Markets analyst Tamy Chen characterized Aurora’s revenue miss as only “modest,” and noted that “Aurora expanded its [recreational marijuana market] share in the quarter.” (Aurora’s market share in recreational weed is now 21.9%, up 340 basis points from last quarter).

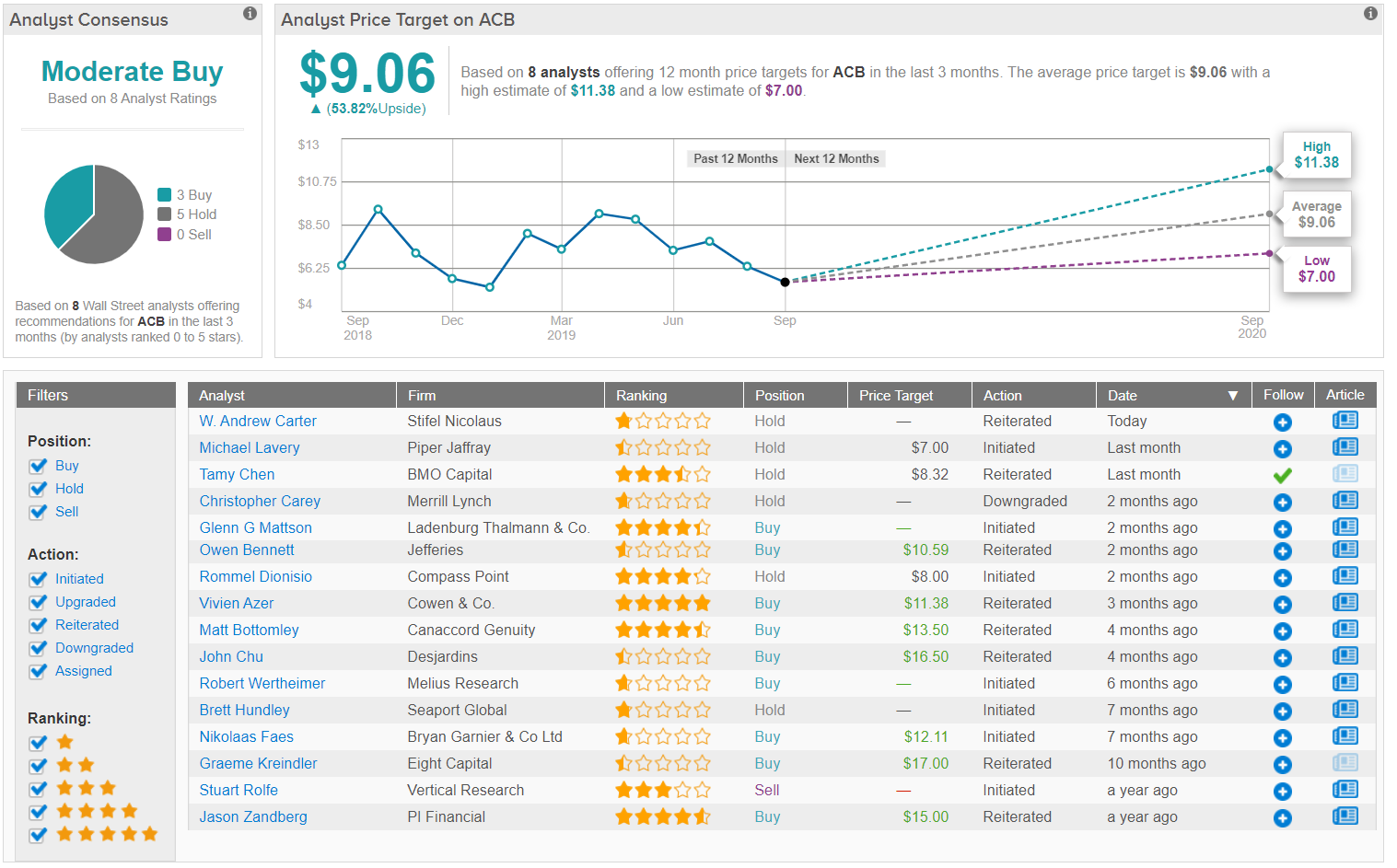

Nevertheless, the upshot of all the above is that both Seaport Global and BMO Capital are only willing to rate the stock “neutral” and “market perform,” respectively — both hold-equivalent ratings. Even after the stock fell 9.4% on Wednesday’s news, neither one is willing to clamber out on a limb and recommend buying the stock.

With sales failing to climb as expected, profitability still a ways away, and cash reserves dwindling, I cannot say as I blame them.

Consensus Verdict

Ultimately, the word on the Street points to a sidelined majority on Aurora Cannabis. In the last three months, the cannabis stock has landed 3 ‘buy’ ratings vs. 5 ‘hold’ ratings. That said, the consensus average price target points to $9.06, or nearly 54% upside potential for the stock. This suggests that by consensus expectations, for now, the bulls still win on ACB.