Toilet paper isn’t the only item consumers are stocking up on. Adult-use marijuana sales surged recently as consumers in the U.S. prepared to be stuck at home. As a result of all the panic buying, sales in California are over 2.5x higher than in March 2019 and 1.5x higher in Colorado. A dozen other markets appear to be on their way to notching all-time year-to-date highs.

Many states have deemed dispensaries as an essential service, ensuring that they can remain operational under certain limitations and guidelines. While Canaccord analyst Matt Bottomley acknowledges that the industry isn’t fully insulated from the effects of the COVID-19 pandemic, he argues that any negative risks are limited substantially thanks to dispensaries. To this end, the analyst tells clients that he sees big things in store for a few U.S. Multi-State-Operators (MSOs).

Bearing this in mind, we used TipRanks’ database to take a closer look at three cannabis stocks backed by the investment firm. Not only have all of the names received enough support from other analysts to earn a “Strong Buy” consensus rating, but each also boasts some brag-worthy upside potential. Let’s get started.

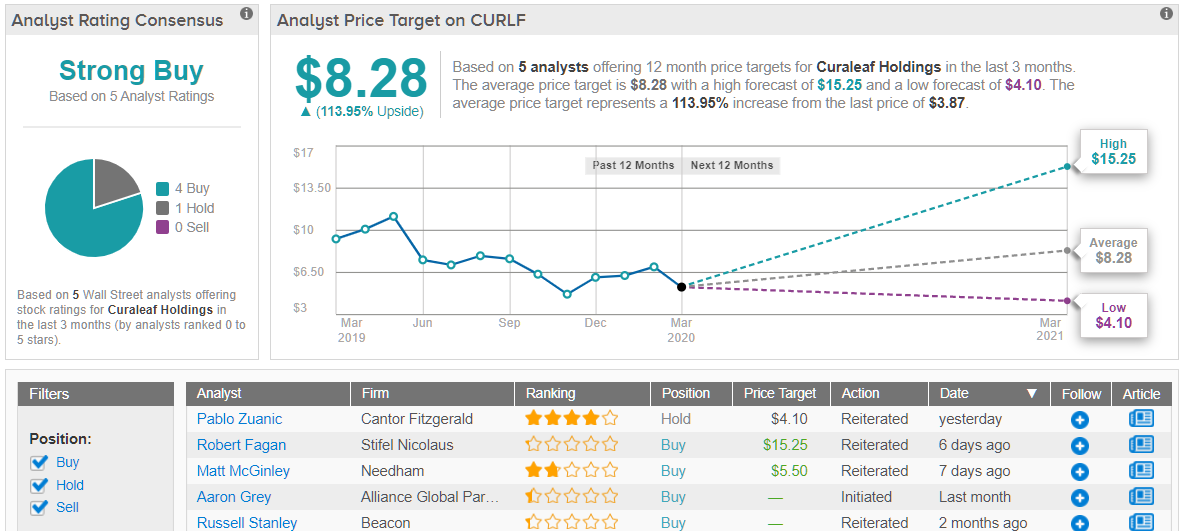

Curaleaf Holdings (CURLF)

First up, we have Curaleaf, which is slated to report earnings today. Based on several developments during the quarter, Canaccord’s Bottomley expects the company to “continue to see attractive growth in its standalone/managed revenue.” In Q4, CURLF expanded its standalone business with the opening of its first adult-use dispensary in Massachusetts and two additional retail openings in Florida. This puts its total exposure in Florida at 28 locations. Even though there’s some uncertainty related to its Grassroots and Select segments, the analyst thinks both will ultimately fuel growth for CURLF.

As a result, Bottomley is calling for standalone/managed revenue of $86.5 million, which would reflect a 15% quarter-over-quarter gain. While the growth is expected to be more modest for Select, due to vaping headwinds, Grassroots could post a 20% quarter-over-quarter rise. This would bring pro forma Q4 revenue to $152.9 million, up 19% from the prior quarter, and adjusted EBITDA to $9.6 million. A slight adjusted gross margin increase could also be in store.

Additionally, after the quarter concluded, the company announced two more recreational dispensaries in Massachusetts, term loan financing of $300 million, license wins in Utah and Pennsylvania and that its Select and Acres acquisitions had been finalized. This prompted Bottomley to state, “As a result, we expect the company to see a significant step-function increase in its standalone top line in the first quarter of 2020.”

With everything CURLF has going for it, it makes sense that Bottomley left his Buy rating and C$16 (US$11) price target as is. Should the target be met, a twelve-month gain of 184% could be in the cards. (To watch Bottomley’s track record, click here)

Turning now to the rest of the Street, other analysts are generally on the same page. 4 Buys and 1 Hold add up to a Strong Buy analyst consensus. At US$8.28, the average price target implies 114% upside potential. (See Curaleaf stock analysis at TipRanks)

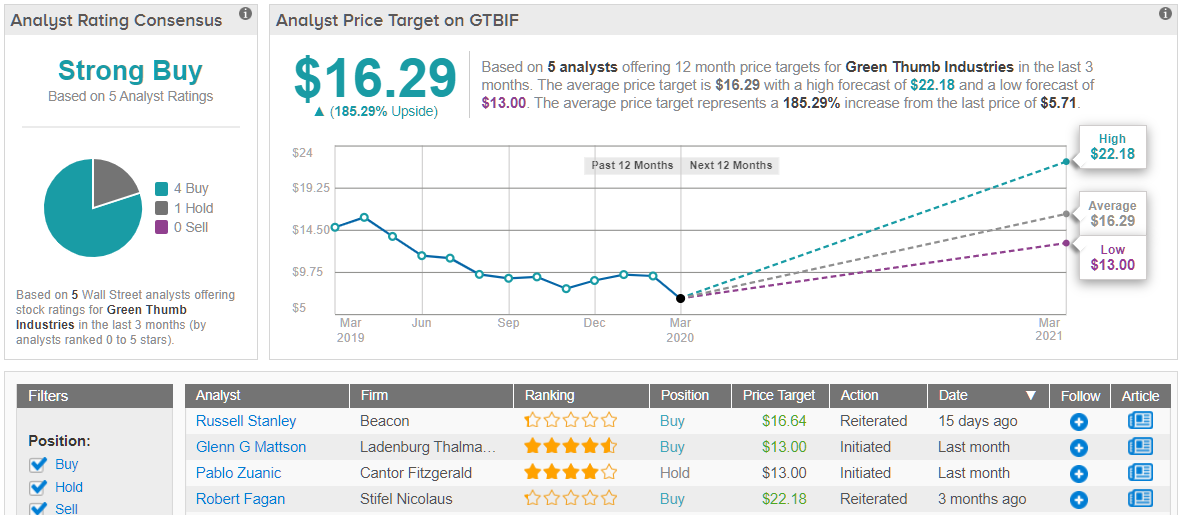

Green Thumb Industries (GTBIF)

Moving on to Green Thumb, Bottomley tells investors he has been impressed with this cannabis name, with it gearing up to announce its financial results on March 26.

Like Curaleaf, GTBIF has made strides in expanding its presence in several states throughout the U.S. At the end of the fourth quarter, the company revealed that it had opened six new locations, two in Pennsylvania and new stores in Florida, New Jersey, Connecticut and Ohio. With these new additions, its year-end store count comes in at 39. If that wasn’t enough, GTBIF received a $20.3 million sales and leaseback arrangement for its Pennsylvania cultivation/production facility.

The implication of these developments? Bottomley argues “For Q4/19, we expect GTI to realize moderate same-store-growth and incremental contribution from six additional stores opened during the period (albeit with less than a month of contribution on average).” This means that quarterly revenue could reach $76.5 million, up 13% quarter-over-quarter, and positive adjusted EBITDA of $11.5 million could be in the cards. Gross margins are expected to hold sturdy as well.

It should also be noted that following the end of the quarter, GTBIF announced additional sales and leasebacks of facilities in Ohio and Illinois and two more store openings in Illinois. “As a result, we believe Q1/20 will likely see significant growth over our Q4/19 forecasts,” Bottomley commented.

In line with his optimistic expectations, Bottomley reiterated his Buy rating. At C$20 (US$13.80), the analyst’s price target suggests 144% upside potential.

Looking at the consensus breakdown, other analysts take a similar approach. With 4 Buys and 1 Hold issued in the last three months, the word on the Street is that GTBIF is a Strong Buy. Not to mention the $16.29 average price target implies 185% upside potential. (See Green Thumb stock analysis at TipRanks)

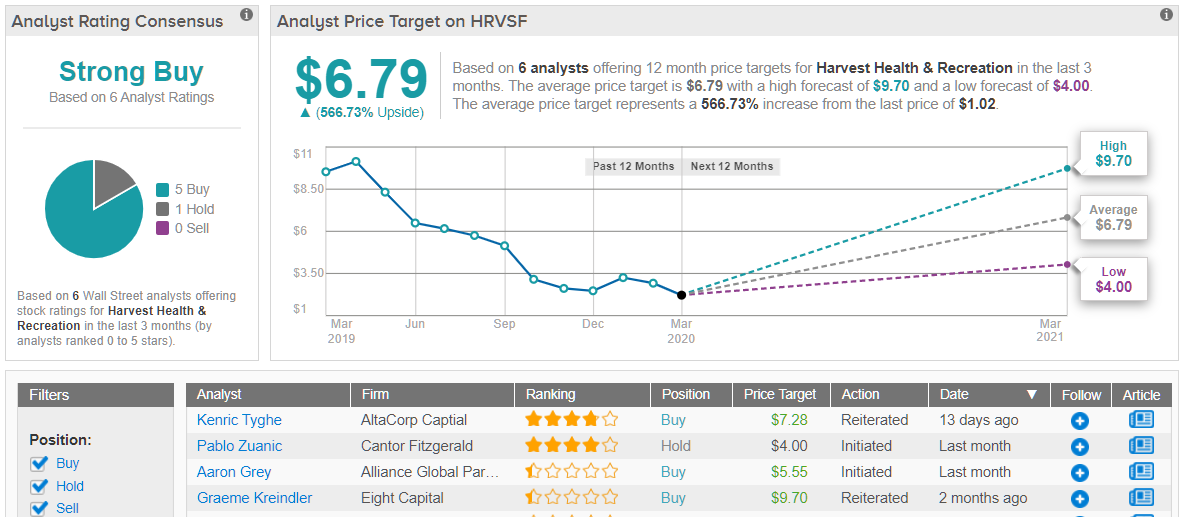

Harvest Health & Recreation (HRVSF)

With Harvest Health & Recreation preparing to report earnings the week of April 6, Bottomley has high hopes based on its recent retail openings.

During the quarter, HRVSF added its fourth dispensary in California, got a license for a fifth and reached a management service agreement for a store in Maryland. According to Bottomley, in order to compete with GTBIF in Pennsylvania, it opened three new stores in the state.

As Bottomley expects “continued progression it its core business, aided by contribution from an additional California recreational store and three new medical dispensaries in Pennsylvania”, he thinks standalone revenue will land at $40.7 million, representing 23% quarter-over-quarter growth. To top it all off, the analyst is predicting a gross margin expansion of 900 basis points to 40% and pro forma quarterly revenue of $109 million, up 14% quarter-over-quarter.

Despite the call for negative adjusted EBITDA, Bottomley points to several new developments reported after quarter-end as being capable of driving upside. “Subsequent to quarter end, the company (1) announced the purchase of an additional facility in Nevada; (2) announced and closed a deal for Have a Heart; (3) announced license wins/strategic arrangements in Arkansas and Michigan; (4) acquired four additional licenses (with three operating dispensaries) in its home state of Arizona (where it has a leading presence); and (5) announced significant corporate updates,” he noted.

Taking all of this into consideration, Bottomley decided to stay with the bulls, maintaining a Buy recommendation and C$7.00 (US$4.85) price target. This target implies that shares could soar 375% in the next year.

What do other analysts have to say? It turns out that a majority are also bullish. A Strong Buy consensus rating breaks down into 5 Buys and 1 Hold. Impressively, the $6.79 average price target leaves room for 567% upside potential. (See Harvest Health stock analysis on TipRanks)