With the end of 2019 coming up, the climate is changing for the cannabis industry. Canada is getting ready to enact the second stage of its legalization drive, opening markets for CBD extracts, beverages, and edibles. The Canadian market is estimated to account for 12% of global marijuana sales by the end of this year. The scale of the US market compensates for the patchwork legalization landscape; US legal cannabis will account for 80% of global sales this year, according to Arcview Market Research.

Troy Dayton, CEO of Arcview, sees CBD as the driver for cannabis sales through 2024. He says, “CBD products on the shelves of grocery stores and mass merchants is just the first act in the “Cannabinoids Everywhere” phenomenon. Unlike with alcohol, coffee or other plant-sourced consumables, cannabis product marketers have more than taste and strength to work with; they also have the subtle effects of 100-plus cannabinoids other than THC. The popularity of CBD is the first inkling of things to come.”

In a report released earlier this summer, retail data analytics firm Nielsen points out that the initial legalization cannabis focused on dried flower products but that the upcoming wave of new derivative products, oils, edibles, and drinks have both higher gross margins and no supply chain bottlenecks. The Nielsen report predicts the US cannabis market reaching $41 billion by 2025.

So, with the market primed to expand, it’s clear that there is a lot of money to be made in marijuana stocks. The segment’s recent dip – at least three major players are at one-year lows as of yesterday – offers a savvy investor a chance to buy in at low prices and high upside potential. We’ve used TipRanks’ Stock Screener tool to find three small-cap marijuana companies with well over 100% upside potential. Let’s take a closer look:

Green Thumb Industries

Chicago-based Green Thumb (GTBIF – Get Report) owns the Rise and Essence brands of retail cannabis outlets, with more than 50 retail stores under the Rise name and additional outlets through third-party marketers. Green Thumb’s calendar Q2 earnings release showed $44.7 million in revenues, a 60% sequential gain and a 228% year-over-year gain. Organic consumer product growth and increased store traffic powered the revenue gains. Along with fast-growing revenue, the company also boasts a strong cash position, with $83 million in liabilities more than balanced by $117 million cash on hand. CEO Ben Kolver stated of the company’s forward prospects, “Continued execution of key priorities such as… accelerated store openings, and expanded distribution of our brand portfolio, sets us up well for the future.”

With operations in 12 US states, including its retail locations and 13 manufacturing facilities, Green Thumb is well positioned to take advantage of the expansion prospects in the US cannabis markets.

Starting coverage of Green Thumb for Cowen in mid-September, 5-star analyst Vivien Azer specifically cites the company’s high growth potential. She writes, “We believe the company’s focused operating model that favors geographic depth, and a balanced revenue approach between wholesale and retail, gives GTI the most revenue and margin potential among our MSO coverage. GTI is our favorite name among the MSOs.” Azer’s $18.50 price target suggests an upside to this stock of 122%. Ms. Azer adds that Green Thumb is a “compelling buy,” describing it as, “…currently trading at 4.2x FY20 revenue, which is a 22% discount to their MSO peers.” (To watch Azer’s track record, click here)

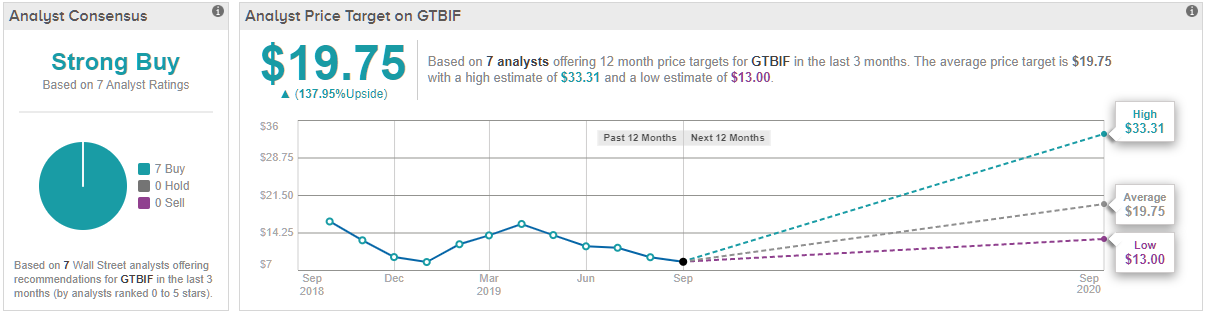

The company’s low share price and high upside are key benefits for new investors looking to get in on that expansion. GTBIF sells for just $8.30 cents per share, and the average price target, $19.75, indicates room for 138% growth. Green Thumb’s Strong Buy analyst consensus rating is based on a unanimous 7 buys assigned to the stock in the last three months. (See Green Thumb’s price targets and analyst ratings on TipRanks)

Supreme Cannabis Company

Formerly Supreme Pharmaceuticals, Supreme Cannabis (SPRWF – Get Report) in September reported its fiscal Q4 number, which included sales growth of 436%, to C$19 million, and the company’s first quarterly profit of C$3.2 million. Company statements credit the high-margin strategy of focusing on premium cannabis products, and the success of its 7ACRES brand of recreational marijuana. More importantly, however, the company held production-related overhead costs down to 49% of net revenue. With sales expected to rise, the company’s firm control of costs is boon for investors.

Supreme posted a C$41 million profit for fiscal 2019, and projects fiscal 2020 profits to come in between C$150 million and C$180 million. The company is positioning itself in partnership with PAX Labs, a leading provider of vaping products to the Canadian markets, giving it a foot in the door when the ‘Cannabis 2.0’ wave hits Canada later this year.

CIBC analyst John Zamparo is impressed by Supreme’s niche in the cannabis industry. Initiating coverage of the stock, he writes, “Supreme Cannabis’ focus on existing, premium-seeking consumers may be the most effective and yet somehow neglected strategy in the adult-use cannabis space.” Zamparo further notes that “…top-quality flower retains higher prices and is more defensive against margin compression, supporting Supreme’s strategy.”

With a marketing strategy based on premium product, and a compelling valuation, Zamparo gives SPRWF a buy rating and a C$2 price target. His target implies an upside of 79%. (To watch Zamparo’s track record, click here)

Zamparo is not along in seeing high potential in Supreme Cannabis. Canaccord 4-star analyst Matt Bottomley also initiated coverage of the stock after the earnings report, giving it a buy rating based on the solid numbers. His C$2.30 price target suggests a 107% upside for Supreme.

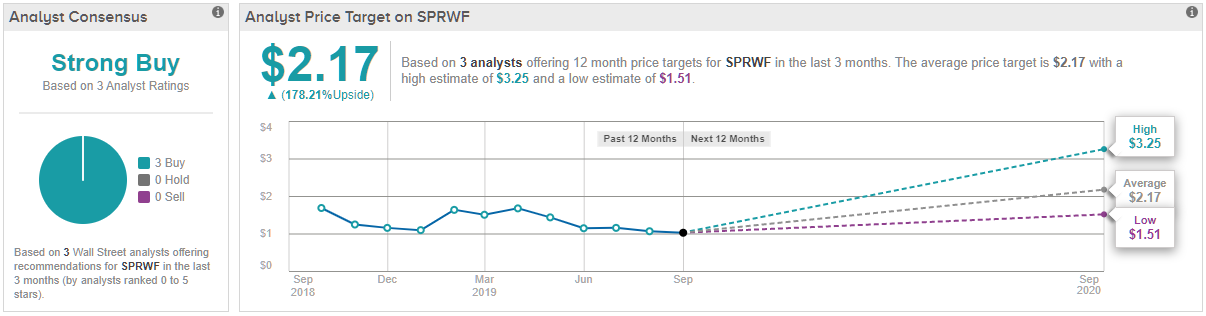

Overall, Supreme Cannabis has a Strong Buy from the analyst consensus, based on 3 recent buy ratings. The stock is prided at a bargain, only $0.84 US, and the $2.17 average price target suggests a robust upside of 178%. (See Supreme Cannabis’ price targets and analyst ratings on TipRanks)

OrganiGram Holdings

Our third small-cap cannabis producer is unique. Unlike most of the Canadian marijuana producers, OrganiGram (OGI – Get Report) is based in New Brunswick, among the country’s Atlantic Maritime Provinces. And, in another departure from the cannabis norm, OrganiGram has operations in all 10 of Canada’s provinces, making it one of the few cannabis companies with a presence coast-to-coast. Most of the Canadian cannabis companies are focusing their operations on the populous regions of Ontario, Alberta, and British Columbia; OrganiGram’s foothold in the Atlantic Maritimes gives it a link to the Canadian region with the country’s highest adult-use rates. The Martimes give OrganiGram a low-competition base region, providing steady sales to support expansion in the rest of the country.

OrganiGram also differentiates itself from its peers in its production methods. Most growers measure their production facilities by square footage, expanding the footprint to increase production area. OrganiGram grows vertically; in the words of CEO Greg Engel, “Where the majority of companies went with large green house expansions, our facility is three levels. We actually do vertical cultivation.” Growing vertically allows OrganiGram to get the greatest efficiency out of its 14-acre facility in Moncton, New Brunswick. The company expects to reach a production capacity of 113,000 kilograms per year by December. At that capacity, OrganiGram will enter the top-10 of Canadian cannabis producers.

OrganiGram’s strong background and increasing production capacity has brought it high ratings from the Street’s analysts. Writing from Beacon Securities, Russell Stanley says the additions to the grow facility “…demonstrate continued execution against the company’s expansion plan, setting the stage for significant revenue/EBITDA growth in fiscal 2020.” He adds that the company reported C$3 million cash on the books in the last quarter, and looks forward to November’s fiscal Q4 report. Stanley’s C$15 price target suggests a one-year upside of 220% for OGI shares. (To watch Stanley’s track record, click here)

John Zamparo, quoted above on Supreme Cannabis, is also bullish on OGI. He writes, “The company offers one of the few opportunities to gain exposure to the cannabis space at a reasonable price. We believe Organigram has demonstrated track record of profitability, a rarity in the cannabis sector.” With profitability in mind, Zamparo initiated coverage of OGI at C$9, indicating confidence in a 92% upside.

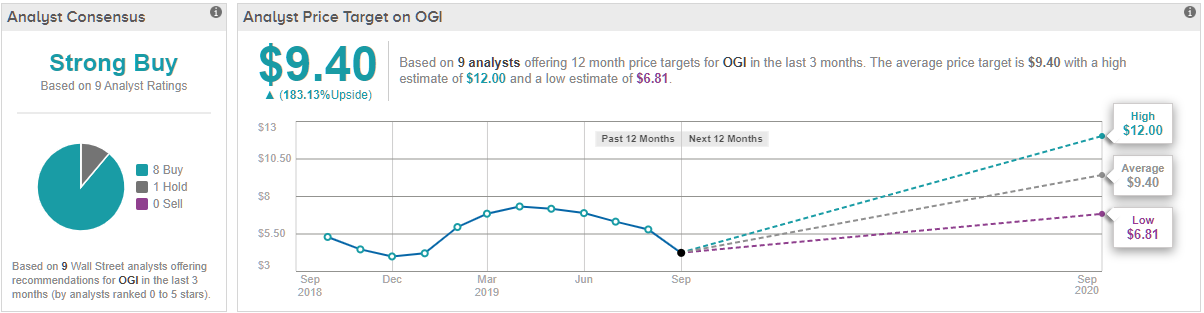

Like the stocks above, OrganiGram also has a Strong Buy from the analyst consensus. This rating is derived from 8 buys and 1 hold given in the past three months. The stock trades for $3.54, and the average price target of $9.40 suggests a hefty upside potential of 183%. (See OrganiGram’s price targets and analyst ratings on TipRanks)