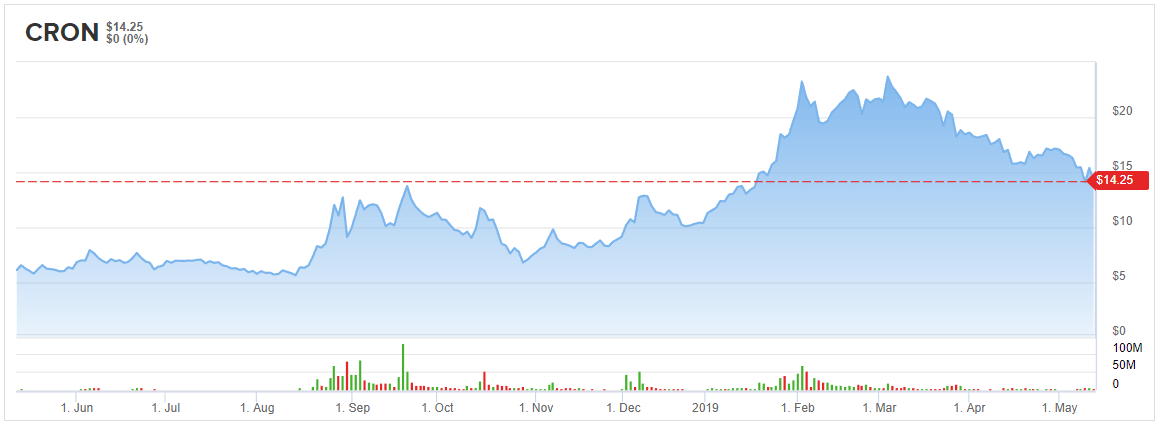

Last week, Cronos (CRON) reported earnings for Q1’19, which just like previous earnings, were not received well by the market. With CRON now down about 35% from highs in early March, investors might be asking if it is worth holding the bag on CRON. The answer is no.

Cronos’s Q1’19 net revenues of C$6.5M represented a mere C$0.9M increase from the quarter prior (C$5.6M for Q4’18). Neither the amount of revenues reported by CRON nor the quarter-over-quarter growth provide any justification for the current enterprise value of approximately C$4B. While CRON’s cash of C$2.4B brought in via the Altria investment provide the company with plenty of ability to expand, the management team at Cronos don’t appear to be taking advantage of that possibility.

Cronos Continues to Botch the Launch of Recreational Cannabis

Cronos’s MD&A from Q3’18 noted that it was selling its recreational cannabis products to cannabis control authorities in Ontario, British Columbia, Nova Scotia and Prince Edward Island. Heading into Q4’18 and the legalization of recreational cannabis this seemed pretty poor coverage of Canada relative to its peers like Canopy Growth Corporation (CGC), Aurora Cannabis (ACB), Tilray (TLRY) and Aphria (APHA).

Cronos had another quarter to get things right, however, it did miss out on the launch of recreational cannabis. Unfortunately, with regards to selling recreational cannabis products, the addition of sales to private retailers in Saskatchewan was the only update to the MD&A for Q4’18. Unsurprisingly, this corresponded to only minimal revenue growth (C$0.9M) for Q1’19.

With Q1’19 Cronos had yet another chance to get things right and ink supply agreements regarding its recreational cannabis products with new provinces. Alarmingly, Cronos doesn’t even appear to have a modest update on this front, the MD&A for Q1’19 doesn’t note any new territories or provinces where the company is selling its recreational cannabis products. What do investors think Q2’19 revenues will look like based on this? Cronos still does not appear to be in the two provinces where retail sales of recreational cannabis are now highest, Alberta and Quebec.

Revenues from Israel Aren’t Close Enough

A substantial amount of excitement surrounds Cronos’s operations in Israel. Cronos Israel is actually a joint venture, it isn’t wholly-owned. Cronos is however entitled to 90% of the net income from Cronos Israel, but it doesn’t appear that sizable revenues are set to come from that venture in Q2’19. The Q1’19 MD&A notes that construction of a 45,000 square foot greenhouse which represents the first phase in Cronos Israel’s expansion is only set to complete in the first half of 2019. Indeed, this construction did not appear to be complete at the time of Q1’19 earnings this May. It seems highly improbable that cultivation could commence in time to produce any meaningful amount of crop for processing and sale in the remainder of Q2’19. Further, Cronos notes that while it does plan to export medical cannabis products from Cronos Israel, this is subject to obtaining all the necessary licenses and permits, something that also does not yet appear to have occurred.

Bottom Line

With lackluster sales casting a shadow over the cannabis business, Cronos stock has struggled recently. While the company still has potential in the future, it seems Q2’19 will look a lot like Q1’19 and Q4’18 — two performances the market did not applaud. It seems unwise to hang around for a third performance.

To read more on the nitty gritty of what’s going on in the rising cannabis industry, click here.

Read more: Cronos Stock Still Looks Overvalued