Despite better than expected quarterly results, Canopy Growth (CGC) hasn’t seen the stock sustain the rally. The coronavirus fears have overshadowed any positive from the quarterly report. While new CEO David Kline promised some restructuring, the company still hasn’t made any official moves to align cannabis production with demand or significant plans to reduce costs. Investors should expect another big move from the company.

Inventory Problems

For the December quarter, Canopy Growth surprised the market by reporting C$123.8 million in net revenue. The market expected far lower revenues after the big provisions and pricing adjustments of FQ2 and the warnings from competitors.

In reality, gross revenues were mostly up due to a surge in other revenues from strategic acquisitions. Cannabis gross revenues were only up C$7.5 million sequentially. The major revenue gains came from the growth in Storz & Bickel vapes and This Works.

For this reason, Canopy Growth has a major cannabis inventory issue. The company ended December with C$622.6 million in inventory, up from only C$262.1 million when the fiscal year started.

Not only is the inventory issue a problem, but the large cannabis company continues to produce far in excess of needs. MKM analyst Bill Kirk estimates Canopy Growth has produced 115,000 kg more than the company has sold. He even estimates the company has enough inventory for 2.5 years of sales.

For December, the company harvested 29,920 kg while only selling 13,237 kg. The amounts improved dramatically from the prior quarter where production was 40,570 kg while sales were only 10,913 kg. Regardless, Canopy Growth was still producing double the sales level last quarter with no signs of material improvements in the Canadian market.

Cost Cutting Next

While Canopy Growth needs to work on further reducing cultivation levels while inventory levels are far too high, the company needs to find additional ways to reduce operating expenses. Even the improved results in FQ3 due to 140 new cannabis retail stores in the Canadian market, the large cannabis company still produced an unsustainable C$91.7 million adjusted EBITDA loss.

For FQ3, Canopy Growth was able to reduce operating expenses by C$10.0 million sequentially to C$150.3 million. But the amount is still nearly 4x the new spending targets of Aurora Cannabis. The launch of Cannabis 2.0 products in Canada and CBD in the U.S. will make these costs difficult to cut substantially.

CFO Mike Lee promised the company will take further steps to reduce costs and right-size the business, but the company hasn’t made a move yet. Canopy Growth still has the cash balance of C$2.3 billion, but the cannabis giant can’t continue burning C$400 million per quarter and still have investors invest in the company based on a sizable balance sheet safety net.

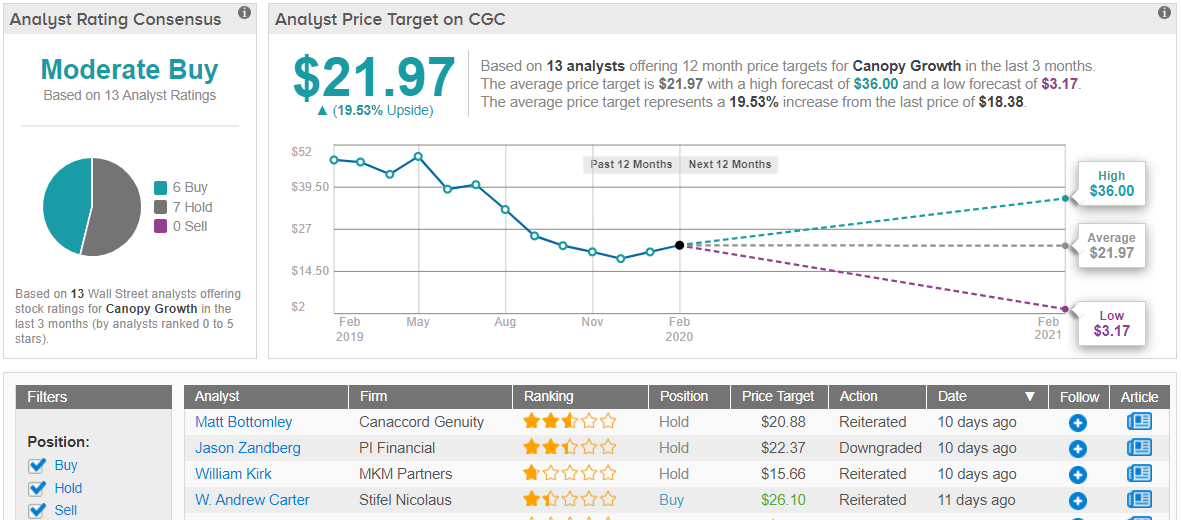

Consensus Verdict

Wall Street has mixed reviews on Canopy Growth. Of 13 analyst ratings tracked by TipRanks, 6 recommend Buy and 7 suggest Hold. The average price target is $21.97, which represents a 20% upside from current levels. (See Canopy stock analysis at TipRanks)

Takeaway

The key investor takeaway is that Canopy Growth still has more hurdles with the stock valuation. Even with the coronavirus market dip, the stock is expensive with a valuation of $7.5 billion while revenue estimates for FY21 ending March are still only up at $550 million after the strong December quarter revenues.

Investors have no valid reason to pay nearly 14x forward sales for a stock still needing to restructure the business. Once the new CEO dramatically cuts the operating expense base and reduces cultivation levels more in line with weak market demand, the stock will become a more appealing long term play.

To find better ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.