Despite all of the promises for the Canadian cannabis space entering 2020, Aurora Cannabis (ACB) reported one of the worst quarters in the space and the lack of financial discipline has to question where the reorganization will work until new executive leadership joins the company.

EBITDA Loss Doubles

The most alarming number reported for the December quarter was the doubling of the adjusted EBITDA loss. Companies can’t always control revenues, especially in an emerging market with volatile regulations, but any particular company can control expenses.

Aurora Cannabis reported a C$80 million EBITDA loss in the quarter, up from $40 million in the prior quarter. The main culprit was operating expenses surging C$20 million sequentially to over C$106 million.

In no logical way should the company have ramped expenses knowing that Cannabis 2.0 products were set to disappoint. The vape health issue was a big concern in North America and the lack of retail stores in both Ontario and Quebec was logically going to restrict any major revenue boost from these products, yet Aurora Cannabis spent wildly.

Too Many Questions Remain

Investors really have to ponder how Aurora Cannabis is going to cut operating expenses to only C$40 million to C$45 million per quarter. The company is forecasting a cut of above C$60 million from the December quarter levels, but the discussion centered on only eliminating 500 corporate positions.

For FQ2, Aurora Cannabis spent C$71 million alone on general and administration expenses. The company has to eliminate over C$26 million from this category alone while completely wiping out sales and marketing and research and development.

The numbers don’t logically add up to how a company can cut 60% of operating expenses and still maintain the existing revenue levels. Aurora Cannabis still forecasts FQ3 revenues staying generally flat with the C$63 million net cannabis revenues in the last quarter.

So many moving parts aren’t supportive of the company maintaining the existing revenue base. Investors need to remember the existing interim CEO and CFO were executives in charge during the disastrous 2019 year. The company just announced a shift to higher THC products and the introduction of a value brand called Daily Specials. In both cases, investors have to question whether the company is skating towards the market or whether the market will again shift on this executive team.

The large cannabis company burned C$276 million in cash during the quarter. Both the C$135 million burned on operations and the C$131 million burned on investing activities during the quarter were appalling. The company has far too many questions on liquidity and a lack of financial discipline to warrant an investment here.

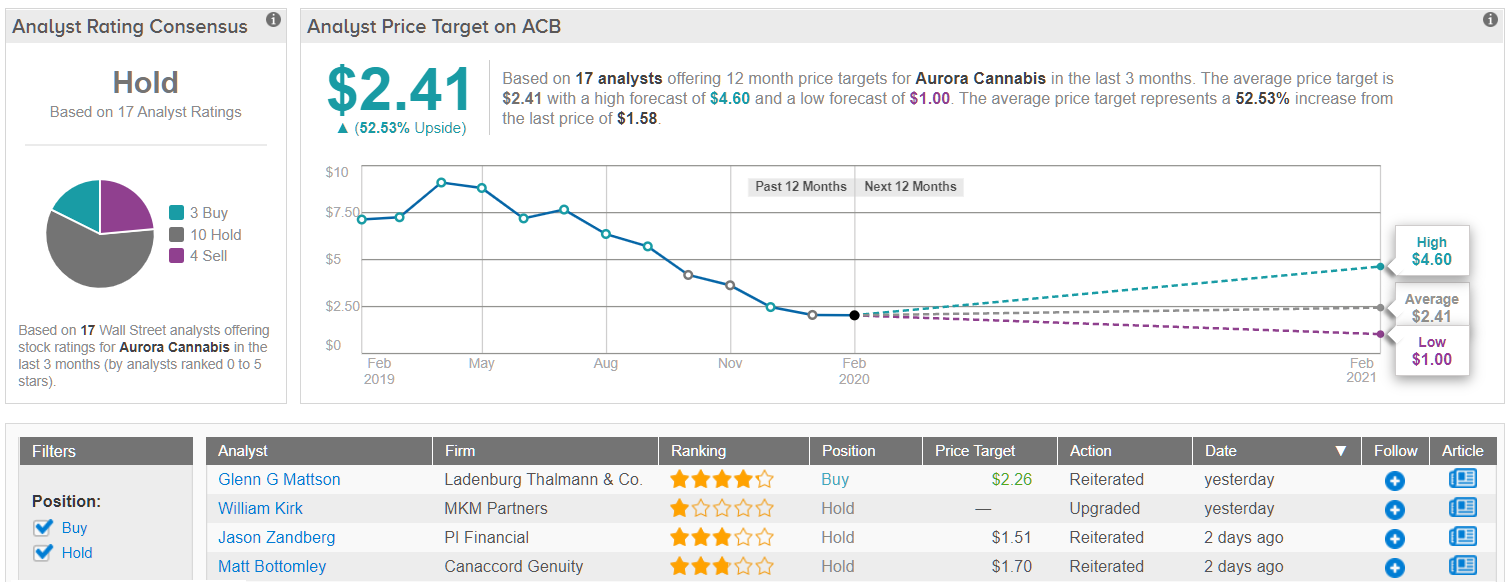

Consensus Verdict

The market’s current view on ACB is a mixed bag, indicating uncertainty as to its prospects. The stock has a Hold analyst consensus rating with only 3 recent “buy” ratings. This is versus 10 “hold” and 4 “sell” ratings. However, the $2.41 average price target suggests an upside potential of nearly 50% from the current share price. (See Aurora Cannabis stock analysis on TipRanks)

Takeaway

The key investor takeaway is that Aurora Cannabis has a Canadian market with a lot of positive catalysts to play out in 2020, but the company lacks the financial discipline for an investment. The stock trades at $1.50 for a reason and the lack of new executive leadership makes Aurora Cannabis too big of a gamble to buy on any weakness. Investors should prepare for the company to struggle with the massive cuts to the operations spilling over into weak revenues.

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclosure: No position.